Enjoy Night⚡Call Girls Patel Nagar Delhi >༒8448380779 Escort Service

20 January Daily market report

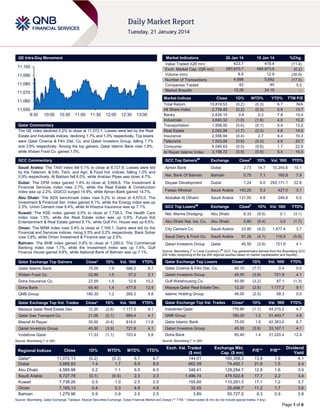

1. QE Intra-Day Movement

Market Indicators

11,100

11,090

11,080

11,070

Market Indices

11,060

11,050

9:30

20 Jan 14

423.7

583,970.7

8.9

4,698

42

12:28

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index declined 0.2% to close at 11,072.1. Losses were led by the Real

Estate and Industrials indices, declining 1.7% and 1.0% respectively. Top losers

were Qatar Cinema & Film Dist. Co. and Qatari Investors Group, falling 7.7%

and 3.9% respectively. Among the top gainers, Qatar Islamic Bank rose 1.9%,

while Widam Food Co. gained 1.5%.

19 Jan 14

478.4

584,973.5

12.9

5,692

40

24:15

%Chg.

(11.4)

(0.2)

(30.9)

(17.5)

5.0

–

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

15,819.53

2,739.40

2,634.15

3,640.32

1,958.00

2,042.98

2,556.94

1,523.08

6,049.63

3,198.72

(0.2)

(0.2)

0.6

(1.0)

(0.6)

(1.7)

(0.4)

(0.6)

(0.0)

(0.9)

(0.3)

(0.3)

0.3

(1.6)

(0.1)

(0.3)

2.7

(0.3)

(0.6)

(0.9)

6.7

5.9

7.8

4.0

5.4

4.6

9.4

4.8

1.7

5.4

N/A

13.7

13.4

13.2

13.2

14.0

10.3

20.7

22.9

16.5

GCC Commentary

GCC Top Gainers##

Exchange

Close#

Saudi Arabia: The TASI index fell 0.1% to close at 8,727.8. Losses were led

by the Telecom. & Info. Tech. and Agri. & Food Ind. indices, falling 1.0% and

0.9% respectively. Al Babtain fell 6.0%, while Arabian Pipes was down 4.7%.

Ajman Bank

1D%

Dubai

2.73

14.7

10,245.6

10.1

Nat. Bank Of Bahrain

Bahrain

0.75

7.1

160.8

7.9

Dubai: The DFM index gained 1.4% to close at 3,669.8. The Investment &

Financial Services index rose 2.7%, while the Real Estate & Construction

index was up 2.2%. GGICO surged 14.9%, while Ajman Bank gained 14.7%.

Deyaar Development

Dubai

1.24

6.0

293,171.1

22.8

Fawaz Alhokair

Saudi Arabia

143.25

5.3

427.0

3.1

Abu Dhabi: The ADX benchmark index rose 0.2% to close at 4,570.0. The

Investment & Financial Ser. index gained 6.1%, while the Energy index was up

2.3%. Union Cement rose 9.4%, while Al Khazna Insurance was up 7.1%.

Abdullah Al Othaim

Saudi Arabia

131.00

4.8

246.8

5.0

GCC Top Losers

Exchange

Kuwait: The KSE index gained 0.5% to close at 7,738.3. The Health Care

index rose 1.5%, while the Real Estate index was up 0.9%. Future Kid

Entertainment & Real Estate gained 9.1%, while Gulf Fin. House was up 8.6%.

Nat. Marine Dredging

Abu Dhabi

8.33

(9.5)

0.1

(3.1)

Abu Dhabi Nat. Ins. Co.

Abu Dhabi

5.80

(9.4)

3.0

(1.7)

Oman: The MSM index rose 0.4% to close at 7,165.1. Gains were led by the

Financial and Services indices, rising 0.5% and 0.2% respectively. Bank Sohar

rose 3.6%, while Oman Investment & Finance was up 2.5%.

City Cement Co.

Saudi Arabia

23.80

(4.2)

1,477.4

3.7

Saudi Dairy & Food Co.

Saudi Arabia

81.25

(4.1)

116.9

(5.8)

Qatari Investors Group

Qatar

45.50

(3.9)

721.9

4.1

Bahrain: The BHB index gained 0.9% to close at 1,280.0. The Commercial

Banking index rose 1.7%, while the Investment index was up 1.4%. Gulf

Finance House gained 9.8%, while National Bank of Bahrain was up 7.1%.

##

#

Close

Vol. ‘000

1D% Vol. ‘000

YTD%

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Islamic Bank

Close*

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Losers

Close*

1D%

Vol. ‘000

YTD%

75.00

Qatar Exchange Top Gainers

1.9

566.2

8.7

Qatar Cinema & Film Dist. Co.

40.10

(7.7)

0.4

0.0

37.2

2.1

Qatari Investors Group

45.50

(3.9)

721.9

4.1

Widam Food Co.

52.80

1.5

Doha Insurance Co.

27.55

1.5

12.9

10.2

Gulf Warehousing Co.

40.95

(3.2)

87.1

(1.3)

Doha Bank

65.40

1.4

477.8

12.4

Mazaya Qatar Real Estate Dev.

12.20

(2.6)

1,177.2

9.1

QNB Group

180.30

1.2

285.3

4.8

Islamic Holding Group

46.00

(2.5)

58.3

0.0

Qatar Exchange Top Vol. Trades

Close*

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

Mazaya Qatar Real Estate Dev.

12.20

(2.6)

1,177.2

9.1

Industries Qatar

176.90

(1.1)

54,215.2

4.7

Qatar Gas Transport Co.

21.09

(0.1)

989.4

4.1

QNB Group

180.30

1.2

51,443.7

4.8

Masraf Al Rayan

35.00

(0.4)

818.0

11.8

Qatar Islamic Bank

75.00

1.9

42,383.0

8.7

Qatari Investors Group

45.50

(3.9)

721.9

4.1

Qatari Investors Group

45.50

(3.9)

33,167.1

4.1

Vodafone Qatar

11.33

(1.1)

703.4

5.8

Doha Bank

65.40

1.4

31,220.4

12.4

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Close

1D%

WTD%

MTD%

YTD%

11,072.13

3,669.83

4,569.98

8,727.78

7,738.26

7,165.13

1,279.96

(0.2)

1.4

0.2

(0.1)

0.5

0.4

0.9

(0.3)

1.7

1.1

(0.4)

1.0

0.3

0.9

6.7

8.9

6.5

2.3

2.5

4.8

2.5

6.7

8.9

6.5

2.3

2.5

4.8

2.5

Exch. Val. Traded

($ mn)

144.01

662.39

348.41

1,496.74

155.60

32.45

3.89

Exchange Mkt.

Cap. ($ mn)

160,358.3

74,492.1

129,284.7

479,522.8

110,261.3

25,499.7

50,727.5

P/E**

P/B**

13.9

21.6

12.8

17.7

17.1

11.2

8.3

1.9

1.5

1.6

2.2

1.2

1.7

0.9

Dividend

Yield

4.1

2.4

3.9

3.4

3.7

3.6

3.8

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 6

2. Qatar Market Commentary

The QE index declined 0.2% to close at 11,072.1. The Real

Estate and Industrials indices led the losses. The index declined

on the back of selling pressure from Qatari shareholders despite

buying support from non-Qatari shareholders.

Qatar Cinema & Film Dist. Co. and Qatari Investors Group were

the top losers, falling 7.7% and 3.9% respectively. Among the

top gainers, Qatar Islamic Bank rose 1.9%, while Widam Food

Co. gained 1.5%.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

55.20%

71.87%

(70,614,235.17)

Non-Qatari

44.79%

28.13%

70,614,235.17

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Monday fell by 30.9% to 8.9mn from

12.9mn on Sunday. However, as compared to the 30-day

moving average of 11.5mn, volume for the day was 22.0% lower.

Mazaya Qatar Real Estate Dev. and Qatar Gas Transport Co.

were the most active stocks, contributing 13.2% and 11.1% to

the total volume respectively.

Earnings and Global Economic Data

Earnings Releases

Company

Basic Chemical Industries

Co.

Saudi Telecom Co. (STC)

United Cooperative

Assurance Co. (UCA)

Knowledge Economic City

(KEC)

Saudi Real Estate Co.

(Akaria)

Wataniya Insurance Co.

Al-Tayyar Travel Group

Holding Co.

Saudi Industrial Services Co.

Allied Cooperative Insurance

Group (ACIG)

Tabuk Agriculture

Development Co.

Takween Advanced

Industries

Middle East Specialized

Cables Co. (MESC)

Saudi Orix Leasing Co.

Saudia Dairy & Foodstuff

Co. (SADAFCO)

Arriyadh Development Co.

Anaam International Holding

Group Co.

Sanad Insurance &

Reinsurance Cooperative

Co. (SANAD)

Saudi Transport &

Investment Co.

Arabian Cement Co.

Mobile Telecommunications

Co. (ZAIN Saudi)

Saudi Pharmaceutical Ind. &

Med. Appliances Corp.

(SPIMACO)

Alahli Takaful Co. (ATC)

Aseer Trading, Tourism &

Manufacturing Co.

Dar Alarkan Real Estate

Development Co.

National Petrochemical Co.

(Petrochem)

Saudi Printing & Packaging

Co. (SPPC)

Savola Group

Alujain Corporation (ALCO)

Methanol Chemicals Co.

(CHEMANOL)

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

–

–

10.2

-63.2%

3.7

-75.2%

–

–

2,852.0

43.8%

3,623.0

821.9%

146.5

10.0%

–

–

1.8

-45.8%

–

–

-0.6

96.5%

15.0

NA

SR

–

–

42.1

5.0%

61.8

9.0%

Saudi Arabia

SR

31.0

-38.5%

–

–

0.6

7862.5%

Saudi Arabia

SR

–

–

214.0

26.6%

209.0

33.1%

Saudi Arabia

SR

–

–

32.3

0.2%

11.8

32.9%

Saudi Arabia

SR

61.7

-1.3%

–

–

1.8

NA

Saudi Arabia

SR

–

–

-1.7

29.4%

-1.8

36.2%

Saudi Arabia

SR

–

–

1.4

-93.7%

1.2

-94.4%

Saudi Arabia

SR

–

–

10.7

412.4%

1.9

NA

Saudi Arabia

SR

–

–

41.4

15.1%

27.6

32.3%

Saudi Arabia

SR

–

–

41.3

5.7%

38.6

8.5%

Saudi Arabia

SR

–

–

44.2

-42.1%

45.3

-36.3%

Saudi Arabia

SR

–

–

-21.4

-631.9%

-11.5

NA

Saudi Arabia

SR

49.3

23.6%

–

–

0.3

11.6%

Saudi Arabia

SR

–

–

-4.9

-1787.3%

81.4

NA

Saudi Arabia

SR

–

–

-80.8

NA

-108.7

NA

Saudi Arabia

SR

–

–

-271.0

-3.4%

-462.0

-4.3%

Saudi Arabia

SR

–

–

50.6

-19.8%

57.0

6.1%

Saudi Arabia

SR

7.5

7.7%

–

–

1.2

41.2%

Saudi Arabia

SR

–

–

75.6

25.4%

40.3

19.2%

Saudi Arabia

SR

–

–

220.8

-8.8%

156.8

8.9%

Saudi Arabia

SR

–

–

191.5

NA

74.6

NA

Saudi Arabia

SR

–

–

13.6

-15.5%

3.6

-95.8%

Saudi Arabia

SR

–

–

563.0

-29.4%

564.0

36.6%

Saudi Arabia

SR

–

–

85.2

31.3%

33.8

97.5%

Saudi Arabia

SR

–

–

45.5

76.3%

36.0

137.0%

Market

Currency

Saudi Arabia

SR

Saudi Arabia

SR

Saudi Arabia

SR

Saudi Arabia

SR

Saudi Arabia

Page 2 of 6

3. Basic Chemical Industries

Co.

Saudi Arabia

SR

–

–

10.2

-63.2%

3.7

-75.2%

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date

Market

Source

Indicator

Period

01/20

Germany

Destatis

PPI MoM

December

01/20

Germany

Destatis

PPI YoY

December

01/20

UK

Rightmove

Rightmove House Prices MoM

January

01/20

UK

Rightmove

Rightmove House Prices YoY

01/20

Italy

ISTAT

01/20

Italy

01/20

China

01/20

Actual

Consensus

Previous

0.10%

0.00%

-0.10%

-0.50%

-0.60%

-0.80%

1.00%

–

-1.90%

January

6.30%

–

5.40%

Industrial Sales MoM

November

0.90%

–

-0.70%

ISTAT

Industrial Orders MoM

November

2.30%

0.00%

-2.30%

National Bureau of Stat.

GDP YTD YoY

4Q2013

7.70%

7.70%

7.70%

China

National Bureau of Stat.

GDP YoY

4Q2013

7.70%

7.60%

7.80%

01/20

China

National Bureau of Stat.

Industrial Production YTD YoY

December

9.70%

9.70%

9.70%

01/20

China

National Bureau of Stat.

Industrial Production YoY

December

9.70%

9.80%

10.00%

01/20

China

National Bureau of Stat.

Retail Sales YTD YoY

December

13.10%

13.10%

13.00%

01/20

China

National Bureau of Stat.

Retail Sales YoY

December

13.60%

13.60%

13.70%

01/20

Japan

Ministry of Eco. Trade

Industrial Production MoM

November

-0.10%

–

1.00%

01/20

Japan

Ministry of Eco. Trade

Industrial Production YoY

November

4.80%

–

5.40%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

DHBK reports net profit of QR236.0mn vs. QR327.2mn (BBG

consensus estimate) in 4Q2013 – Doha Bank (DHBK)

reported a net profit of QR236.0mn in 4Q2013, dropping by

28.2% QoQ. Earnings per share for 2013 stood at QR5.29. Total

assets rose to QR67bn in 2013, representing a 21.3% YoY

growth. Loans & advances rose by 21.8% from QR33.8bn in

2012 to QR41.1bn in 2013, while customer deposits expanded

23.6% to QR42.5bn in 2013. Meanwhile, the bank has declared

a 45% (QR4.5/share) cash dividend (dividend yield of 6.9%),

which will have to be approved by the Qatar Central Bank and

its shareholders. DHBK’s Chairman Sheikh Fahad bin Mohamad

bin Jabor al-Thani said the bank is aiming for 15-20% asset

growth over the next four to five years. (QNBFS Research, GulfTimes.com, Qatar Tribune)

BRES selling its Barwa Bank stake for QR2.4bn – Barwa

Real Estate Group (BRES) is selling its 37.34% stake in Barwa

Bank for QR2.4bn. This deal is part of an existing agreement

between Qatari Diar and BRES, according to which Barwa sells

some of its assets to Qatari Diar and uses the profit of those

transactions to pay off some credit facilities. The deal is

expected to reflect on the company’s financial results in

4Q2013. BRES has sold all its shares in Barwa Bank after using

its rights to buy back 40.746.660 million shares, about 14% of

the bank’s shares in December 2013. The group is currently

obtaining the necessary regulatory approvals to complete the

transaction. (QE)

QP to spend $7bn to boost crude, gas condensate

production – According to sources, Qatar Petroleum (QP) is

planning to spend around $7bn over the next seven years to

boost crude oil & gas condensate production from its Bul Hanine

offshore field. The field off Qatar’s east coast produces around

40,000 bpd of crude oil and QP hopes to more than double its

output to 90,000 bpd by 2020. (Peninsula Qatar)

GDI takes possession of eighth jack-up rig for Oxy – Gulf

Drilling International (GDI) has taken possession of its eighth

jack-up drilling rig, which will be put into service for Occidental

Petroleum of Qatar (Oxy). The rig, which has been named

Msheireb after a district in the heart of Doha, is being towed to

Qatar where it will be prepared with upgrades to provide smooth

and seamless duty to its client, Oxy, at the NKOM (NakilatKeppel Offshore and Marine) shipyard. (Gulf-Times.com)

Doha Festival City appoints contractor for Qatar's largest

mall – Doha Festival City, Qatar's largest retail & entertainment

destination, has appointed a joint venture of the Gulf Contracting

Company and Alec Qatar as the contractor to work on the

construction for the mall of the QR6bn Doha Festival City

project. Scheduled to open in 3Q2016, the mall will be home to

over 550 brands of which many will be making their debut in

Qatar. (Qatar Tribune)

QA adds three weekly flights on Doha-Khartoum route –

Qatar Airways (QA) has added three additional flights per week

between Doha and Khartoum, bringing the total number of

services to Sudan to 17 weekly flights. QA’s CEO Akbar Al

Baker said that the extra capacity would be a great boost as it

would improve connections from Khartoum to over 130

destinations across the airline’s global network. (Bloomberg)

International

Global regulators plan to start work on new bank asset

valuation rule – According to sources, the global regulators are

planning the world’s first common rule within three years to

value hard-to-price assets held by banks after unexpected

revisions have unsettled investors. (Gulf-Times.com)

ILO warns of jobless recovery as global unemployment

climbs – The International Labour Organization (ILO) said

global unemployment climbed by 5mn people in 2013 to 202mn

despite green shoots in the world economy, signaling a jobless

recovery. Business activity is picking up but the misery of

unemployment continues to pile up. The ILO expects that about

215mn people worldwide to be unemployed by 2018. (ET)

Regional

GECF: Investments on conventional gas to remain robust –

The Gas Exporting Countries Forum (GECF) said the

investments on conventional gas would continue to be “robust”

in the foreseeable future – it further added that it would favor

“competing fuel-linked” pricing for gas. GECF also stated that

the present hydraulic fracturing (fracking) technology to extract

shale gas would prove to be an “impediment” for future

exploration because of environmental concerns, but it would

Page 3 of 6

4. enhance global gas supply. GECF’s Secretary General Seyed

Mohamed Hossein Adeli said the total reserves of shale gas are

2% and if one talks about production, it will be 6%. This is the

reason why investments on conventional gas will continue to

remain robust. (Gulf-Times.com)

MEED: Solar energy investment in MENA could cross $50bn

– The MENA region could see more than $50bn worth of

investment in the solar power sector by 2020 as regional

governments push for the adoption of clean energy and take

advantage of the region's high solar irradiation levels. According

to the MENA Solar Energy Report 2014, published by MEED

Insight in association with the Middle East Solar Industry

Association (MESIA), up to 37,000MW of new solar, wind and

hydroelectric projects are planned to be commissioned by the

end of the decade. Among these around 12,000-15,000MW will

be sourced from solar energy projects alone. (GulfBase.com)

Alkhabeer Capital, USAA Real Estate acquire real estate

assets – Alkhabeer Capital and its investment partner USAA

Real Estate Company announced that their real estate

investment team has completed the acquisition of Gateway

Distribution Portfolio in the city of St. Louis in the US. The

Gateway Distribution Centers I & II, are modern, Class A

warehouse buildings totaling 280,407 square meters that are

strategically located in the Gateway Commerce Center. This

premier bulk distribution park is located in the St. Louis area and

is close to a major US port, four cargo handling airports, and two

major highways. (GulfBase.com)

Kingdom’s two big hospitals plan stock market listings –

Saudi Arabia’s two private hospital operators are planning to list

their shares on the stock market as pressure mounts on the

government to pour huge sums into the underdeveloped sector.

Sulaiman Al-Habib Medical Group and Almana General

Hospitals are expected to list on the local bourse in late 2014 or

early 2015. (GulfBase.com)

Saudi Aramco cuts February supply due to maintenance –

According to sources, Saudi Aramco will supply less of its Arab

Extra Light crude in February 2014 due to maintenance at one

of its biggest oilfields. The company will carry out maintenance

at the Shaybah oilfield in February that could last up to two

months. Shaybah has a capacity of 750,000 bpd, which is

expected to rise to 1mn bpd by the end of 2016 or early 2017.

(Reuters)

Zain Saudi’s 4G use soars 1,400% in 2013 – The Mobile

Telecommunication Company (Zain Saudi) revealed that its 3G

network witnessed an unprecedented 100% increase in data

traffic, as compared to the same period in last year. Similarly,

Zain Saudi 4G network saw a 600% increase in data traffic and

1,400% increase in active user rates in 2013. (GulfBase.com)

New JV to target Saudi solar projects – A new JV has been

set up by Saudi Arabia's Abdul Latif Jameel Energy (ALJ

Energy) and Fotowatio Renewable Ventures (FRV) to develop

solar energy projects in the Kingdom. Both companies will jointly

develop and invest in photovoltaic (PV) solar power plants.

Through this venture, FRV and ALJ Energy will together on the

tender of the King Abdullah City for Atomic & Renewable Energy

program, which includes the construction of 41 GW of solar

power plants by 2032, of which 16 GW will be photovoltaic.

(GulfBase.com)

Savola Group declares SR266.99mn dividends for 4Q2013 –

Savola Group’s board of directors has approved the distribution

of dividends worth SR266.99mn (SR0.5 per share) for 4Q2013,

representing 5% of the share’s nominal value. Shareholders

who are registered in the company’s books by the end of the

trading date on the day of its AGM will be eligible for these

dividends. (Tadawul)

STC declares SR1,500mn dividends for 4Q2013 – The Saudi

Telecom Company’s (STC) board of directors has

recommended the distribution of dividends worth SR1,500mn

(SR0.75 per share), representing 7.5% of the face value for

4Q2013 to its shareholders. Those shareholders who are

registered in the Security Depository Center on the day of the

shareholder meeting will be eligible for these dividends.

(Tadawul)

ADC to increase its capital through bonus shares – Arriyadh

Development Company’s (ADC) board of directors has

recommended for 33.3% increase in the company’s capital

through bonus shares. The company’s capital is to be raised

from SR1,000mn to SR1,333.3mn, which will be done through

the capitalization of SR333.3mn from account. With this, the

number of shares would go up from 100mn to 133.3mn shares.

(Tadawul)

UAE's Shah Gas Project to be online early 2015 – The Abu

Dhabi National Oil Company’s (ADNOC) Chief Executive

Abdulla Nasser Al Suwaidi said that the UAE’s Shah Gas

Project will not be operational until early 2015, confirming the

multi-billion dollar development was behind schedule. ADNOC

officials had previously said the project, which would produce

usable gas from Shah's high-sulfur reserves, will be completed

in late 2014. (Reuters)

Arabtec wins AED5.7bn Jordan resort contract – Arabtec

Construction has been selected to execute an AED5.7bn

contract for the construction of the Red Sea Astrarium, a

themed-entertainment resort in Aqaba, Jordan. The Astrarium is

an integrated entertainment, hospitality, and leisure

development that is set to become a family destination,

attracting visitors from across the Middle East. (GulfBase.com)

Dubai starts work on huge resort on man-made islands –

The Kleindienst Group has started building a huge resort

complex on a man-made archipelago off Dubai's coast. The

group said the “Heart of Europe” project, a complex of luxury

hotels and villas stretching across six small islands is expected

to be completed by 2016-end. Lying about 5 kilometers off

mainland Dubai in the Gulf, the project will feature classic Italian,

Spanish and German architecture as well as landscaped

gardens & streets that in some cases will be lined with artificial

snow. (Peninsula Qatar)

Flydubai launches first direct air link between Dubai and

Hofuf – Flydubai has announced the launch of flights to Hofuf,

the largest city in the Al-Ahsa region of Saudi Arabia. The new

twice-weekly service to Al Ahsa Airport will commence on

February 6, 2014, bringing the total number of destinations

served by the carrier in the Kingdom to 11. (GulfBase.com)

DWTC expects 500,000 visitors in 1Q2014 – Dubai World

Trade Centre’s (DWTC) Senior Vice-President– Venues Ahmed

Alkhaja said more than 500,000 visitors are expected to visit the

center in 1Q2014, which is the region’s largest meetings,

incentives, conferences, exhibitions venue. He added that the

growth is driven by many of the region’s leading anchor shows,

including the Arab Health Exhibition & Congress, Gulfood, as

well as a robust calendar of trade events, conferences and

concerts. (GulfBase.com)

Emaar launches Boulevard Point in Downtown Dubai –

Emaar Properties set to launch “Boulevard Point”, in Downtown

Dubai on January 25, 2014. Featuring 297 residences, this 63storey building will encompass 1-3 bedroom residences.

Located above the Dubai Mall extension, “Boulevard Point” will

Page 4 of 6

5. offer direct access to the mall through a dedicated bridge link.

(GulfBase.com)

reported a net profit of OMR41.4mn for 2013, up from

OMR40.7mn in the previous year. (Gulf-Times.com)

TAQA to invest $1.2bn for developing Atrush oil & gas

block in Kurdistan region – Abu Dhabi National Energy

Company’s (TAQA) Iraq Operations Head said it is planning to

invest around $1.2bn for developing the Atrush oil & gas block in

the autonomous Kurdistan region. Earlier, TAQA has received

approval from the Kurdistan Regional Government (KRG) to

develop the block in late 2013. The company expects to invest

more than $300mn in the first phase of the project, with first oil

from the 30,000 bpd first phase expected in early 2015.

(Peninsula Qatar)

Renaissance divests from its NTI subsidiary – Renaissance

Services (RNSS) has entered into a binding agreement with

Babcock International Group (Babcock) to divest its whollyowned

subsidiary,

National

Training

Institute (NTI).

Renaissance’s CEO, Stephen Thomas said that this divestment

is part of the company’s strategy to focus on its core

businesses: the Topaz Offshore Support Vessel Fleet and the

Renaissance Contract Services & Facilities Management Group.

(MSM)

BIOjet Abu Dhabi to grow aviation biofuel industry in UAE –

Abu Dhabi-based Masdar Institute of Science & Technology and

its partners announced that they will collaborate on a new

initiative to support a sustainable aviation biofuel industry in the

UAE. The venture partners include Abu Dhabi’s oil refining

company Takreer, Total, Etihad Airways and Boeing Company.

The initiative named “BIOjet Abu Dhabi: Flight Path to

Sustainability”, will look at the possibilities to extract biofuels

from agriculture waste, date palm leaves, and plants tolerant to

salt water that can be grown on coastal areas of the UAE.

(GulfBase.com)

IRENA & ADFD announces $41mn for renewable energy

projects in developing countries – The International

Renewable Energy Agency (IRENA) and the Abu Dhabi Fund

for Development (ADFD) have announced funding for renewable

energy projects in the Republic of Ecuador, Sierra Leone, the

Maldives, Mauritania, Samoa, and Mali. IRENA and ADFD are

providing about $41mn in loans for these projects. These

selected projects bring power to isolated off-grid populations, in

turn will stimulate the local economic development and raise

living standards. The projects selected will provide energy to

over 300,000 people and numerous businesses. In total, 35

megawatts (MW) of energy capacity will come online, along with

4mn liters of biodiesel production per year. (GulfBase.com)

Mubadala, Shell swap Malaysian oilfield stakes – Mubadala

Petroleum and Royal Dutch Shell have swapped equity stakes

in two exploration blocks off Malaysia. Mubadala has taken a

20% interest in the Shell-operated deepwater Block 2B, while

Shell has taken a 20% interest in the Mubadala-operated Block

SK320 in return. Mubadala, owned by the Abu Dhabi

government, said that drilling in the Block SK320 yielded two

new gas discoveries, called Pegaga and Sintok. (GulfBase.com)

Shell sells stakes in Australian gas project to KUFPEC for

$1.14bn – Royal Dutch Shell said it had agreed to sell stakes in

a gas project in Western Australia for $1.14bn as part of its drive

to improve return on investment. Shell is selling an 8% stake in

the Wheatstone and nearby Iago gas fields as well as a 6.4%

stake in the related Wheatstone LNG project to the Kuwait

Foreign Petroleum Exploration Company (KUFPEC). The move

raises KUFPEC's holding in the Chevron-led LNG project, in

which the state company is already a partner owning 13.4%

stake. (Qatar Tribune)

Kuwait Projects hires banks for possible dollar bond sale –

According to sources, Kuwait Projects Company has hired BNP

Paribas, HSBC and JPMorgan for RegS dollar bonds under its

EMTN program. Kuwait Projects Company is set to hold

meetings starting January 23 in Asia, Middle East, Europe for

this bond sale. (Bloomberg)

OUIC appoints acting CEO – The Oman United Insurance

Company (OUIC) has appointed Muthukumar as the acting

Chief Executive Officer effective from January 20, 2014. (MSM)

Bank Sohar signs MoU with OHB – Bank Sohar has signed a

MoU with the Oman Housing Bank (OHB) to provide preferential

housing loans to Omani citizens. As part of Bank Sohar’s

commitment to the community, the provision of low-interest

home loans will provide financing for local citizens to own their

dream homes, which in turn will assist in the overall economic

development of the country. (Bloomberg)

Alizz Islamic Bank reports loss of OMR3.2mn for 13 month –

Alizz Islamic bank has reported a loss of OMR3.2mn for the

period November 2, 2012 to December 31, 2013. For the

preceding period, October 2011 to November 1, 2012, the bank

made a loss of OMR168,432. Total assets stood at

OMR99.72mn. The bank reported OMR487,468 in customers’

current accounts and OMR607,515 in equity of unrestricted

investment account holders. (GulfBase.com)

Omani CMA plans to launch Oman SME Exchange – The

Omani Capital Market Authority (Omani CMA) is planning to

develop a capital market and exchange for small & medium

enterprises (SME) in Oman. The model is being developed in

line with some of the most successful SME markets in the world,

and in coordination with the Ministry of Commerce & Industry

and the Public Authority for SME Development. (Bloomberg)

Bahrain Airshow surpasses $3bn mark – Deals worth around

$3bn were concluded during the three-day Bahrain International

Airshow event and its organizers confirmed that business deals

generated at the show were three times higher than the total in

2012. The announcement was made at the close of the third

edition of the event by show’s organizers, the Ministry of

Transportation and the Royal Bahrain Air Force in partnership

with Farnborough International Ltd. With over 100 international

and domestic companies present at the show, the increased

business was a reflection of the event’s importance in the Middle

Eastern aviation market. Over 130 delegations from 32 countries

participated in a series of meetings and events. (GulfBase.com)

GFH to sell 75% stake in LUFC – The Gulf Finance House

(GFH) has signed an agreement with a consortium of British

investors to sell 75% of its stake in Leeds United Football Club

(LUFC). The agreement is currently awaiting approval from the

English Football Association. Following the sale, GFH’s stake in

LUFC will remain at 10%. GFH stated that the sale should have

a positive financial impact for the company. (Bahrain Bourse)

NBO reports OMR10.2mn in 4Q2013 – National Bank of Oman

(NBO) posted a net profit of OMR10.2mn in 4Q2013. The bank

Page 5 of 6

6. Rebased Performance

Daily Index Performance

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

138.7

126.1

1.2%

0.9%

0.8%

0.5%

0.4%

0.4%

0.2%

0.0%

S&P Pan Arab

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu *

North American Spot LPG

Propane Price*

North American Spot LPG

Normal Butane Price*

Euro

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,254.66

0.0

0.0

4.1

DJ Industrial*

16,458.56

0.0

0.0

(0.7)

20.33

(0.0)

(0.0)

4.4

S&P 500*

1,838.70

0.0

0.0

(0.5)

106.35

(0.1)

(0.1)

(4.0)

NASDAQ 100*

4,197.58

0.0

0.0

0.5

4.39

0.0

0.0

1.1

STOXX 600

335.50

(0.1)

(0.1)

2.2

137.50

0.0

0.0

8.9

DAX

9,715.90

(0.3)

(0.3)

1.7

150.50

0.0

0.0

10.3

FTSE 100

6,836.73

0.1

0.1

1.3

1.36

0.1

0.1

(1.4)

CAC 40

104.18

(0.1)

(0.1)

(1.1)

Nikkei

GBP

1.64

0.0

0.0

(0.8)

MSCI EM

CHF*

1.10

0.0

0.0

(1.9)

SHANGHAI SE Composite

AUD

0.88

0.3

0.3

(1.2)

USD Index*

81.23

0.0

0.0

RUB

33.76

0.6

0.6

BRL

0.43

0.1

0.1

0.7

Yen

Dubai

May-13

Oman

Oct-12

Abu Dhabi

QE Index

Mar-12

Bahrain

Aug-11

Kuwait

Jan-11

(0.1%) (0.2%)

Qatar

(0.4%)

Saudi Arabia

Jun-10

1.4%

1.6%

159.1

4,322.86

(0.1)

(0.1)

0.6

15,641.68

(0.6)

(0.6)

(4.0)

970.82

(0.1)

(0.1)

(3.2)

1,991.25

(0.7)

(0.7)

(5.9)

HANG SENG

22,928.95

(0.9)

(0.9)

(1.6)

1.5

BSE SENSEX

21,205.05

0.7

0.7

0.2

2.7

Bovespa

48,708.41

(1.0)

(1.0)

(5.4)

1,394.49

(0.1)

(0.1)

(3.3)

Source: Bloomberg (*Market closed on January 20, 2013)

RTS

Source: Bloomberg (*Market closed on January 20, 2013)

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6