High Class Call Girls Nagpur Grishma Call 7001035870 Meet With Nagpur Escorts

2 August Daily market report

1. Page 1 of 6

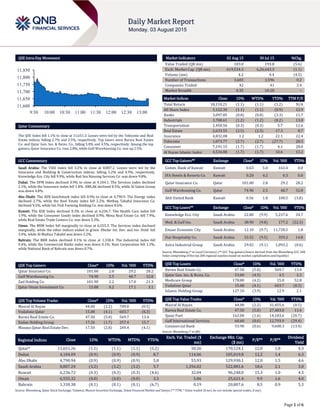

QSE Intra-Day Movement

Qatar Commentary

The QSE Index fell 1.1% to close at 11,651.3. Losses were led by the Telecoms and Real

Estate indices, falling 2.7% and 2.5%, respectively. Top losers were Barwa Real Estate

Co. and Qatar Gen. Ins. & Reins. Co., falling 5.0% and 4.5%, respectively. Among the top

gainers, Qatar Insurance Co. rose 2.8%, while Gulf Warehousing Co. was up 2.5%.

GCC Commentary

Saudi Arabia: The TASI Index fell 3.2% to close at 8,807.2. Losses were led by the

Insurance and Building & Construction indices, falling 5.2% and 4.9%, respectively.

Knowledge Eco. City fell 9.9%, while Red Sea Housing Services Co. was down 9.8%.

Dubai: The DFM Index declined 0.9% to close at 4,104.1. The Services index declined

2.1%, while the Insurance index fell 1.8%. AMLAK declined 8.5%, while Al Salam Group

was down 4.8%.

Abu Dhabi: The ADX benchmark index fell 0.9% to close at 4,790.9. The Energy index

declined 2.7%, while the Real Estate index fell 2.2%. Methaq Takaful Insurance Co.

declined 9.5%, while Int. Fish Farming Holding Co. was down 8.6%.

Kuwait: The KSE Index declined 0.3% to close at 6,236.7. The Health Care index fell

1.9%, while the Consumer Goods index declined 0.9%. Mena Real Estate Co. fell 7.9%,

while Real Estate Trade Centers Co. was down 5.3%.

Oman: The MSM Index fell marginally to close at 6,555.3. The Services index declined

marginally, while the other indices ended in green. Dhofar Int. Dev. and Inv. Hold. fell

3.4%, while Al Madina Takaful was down 2.2%.

Bahrain: The BHB Index declined 0.1% to close at 1,330.4. The Industrial index fell

0.4%, while the Commercial Banks index was down 0.1%. Nass Corporation fell 1.2%,

while National Bank of Bahrain was down 0.7%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Insurance Co. 101.00 2.8 29.2 28.2

Gulf Warehousing Co. 74.90 2.5 48.7 32.8

Zad Holding Co. 101.90 2.2 17.0 21.3

Qatar Oman Investment Co. 15.88 0.2 17.1 3.1

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Masraf Al Rayan 44.00 (2.2) 709.0 (0.5)

Vodafone Qatar 15.08 (4.1) 603.7 (8.3)

Barwa Real Estate Co. 47.50 (5.0) 569.7 13.4

Ezdan Holding Group 17.26 (1.7) 257.4 15.7

Mazaya Qatar Real Estate Dev. 17.50 (2.8) 249.4 (4.1)

Market Indicators 02 Aug 15 30 Jul 15 %Chg.

Value Traded (QR mn) 183.0 193.8 (5.6)

Exch. Market Cap. (QR mn) 619,534.3 6,26,443.3 (1.1)

Volume (mn) 4.2 4.4 (4.5)

Number of Transactions 3,603 3,596 0.2

Companies Traded 42 41 2.4

Market Breadth 4:35 10:28 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,110.21 (1.1) (1.1) (1.2) N/A

All Share Index 3,122.30 (1.1) (1.1) (0.9) 12.9

Banks 3,097.85 (0.8) (0.8) (3.3) 13.7

Industrials 3,708.61 (1.2) (1.2) (8.2) 13.0

Transportation 2,450.56 (0.3) (0.3) 5.7 12.6

Real Estate 2,633.55 (2.5) (2.5) 17.3 8.7

Insurance 4,832.08 1.2 1.2 22.1 22.4

Telecoms 1,073.77 (2.7) (2.7) (27.7) 28.3

Consumer 7,191.15 (1.7) (1.7) 4.1 28.0

Al Rayan Islamic Index 4,534.88 (1.7) (1.7) 10.6 13.2

GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD%

Comm. Bank of Kuwait Kuwait 0.63 5.0 163.4 0.0

IFA Hotels & Resorts Co. Kuwait 0.20 4.2 0.3 0.0

Qatar Insurance Co. Qatar 101.00 2.8 29.2 28.2

Gulf Warehousing Co. Qatar 74.90 2.5 48.7 32.8

Ahli United Bank Kuwait 0.56 1.8 100.5 (3.8)

GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD%

Knowledge Eco. City Saudi Arabia 22.80 (9.9) 5,237.6 34.7

Med. & Gulf Ins. Saudi Arabia 38.90 (9.8) 177.2 (22.3)

Emaar Economic City Saudi Arabia 12.10 (9.7) 11,720.5 1.8

Dur Hospitality Co. Saudi Arabia 33.52 (9.5) 359.2 14.8

Astra Industrial Group Saudi Arabia 29.02 (9.1) 1,093.2 (0.6)

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200

Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Barwa Real Estate Co. 47.50 (5.0) 569.7 13.4

Qatar Gen. Ins. & Reins. Co. 53.00 (4.5) 4.5 3.3

Medicare Group 178.80 (4.2) 15.0 52.8

Vodafone Qatar 15.08 (4.1) 603.7 (8.3)

Islamic Holding Group 127.10 (3.9) 12.9 2.1

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Masraf Al Rayan 44.00 (2.2) 31,455.6 (0.5)

Barwa Real Estate Co. 47.50 (5.0) 27,483.0 13.4

Qatar Fuel 162.00 (1.6) 14,183.6 (20.7)

Gulf International Services 68.60 (0.6) 12,793.9 (29.4)

Commercial Bank 53.90 (0.6) 9,608.3 (13.4)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded ($

mn)

Exchange Mkt. Cap.

($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 11,651.26 (1.1) (1.1) (1.1) (5.2) 50.26 170,124.1 12.0 1.8 4.3

Dubai 4,104.09 (0.9) (0.9) (0.9) 8.7 114.06 105,019.8 12.2 1.4 6.3

Abu Dhabi 4,790.94 (0.9) (0.9) (0.9) 5.8 55.93 129,930.1 12.0 1.5 4.6

Saudi Arabia 8,807.24 (3.2) (3.2) (3.2) 5.7 1,356.02 522,881.6 18.6 2.1 3.0

Kuwait 6,236.72 (0.3) (0.3) (0.3) (4.6) 32.04 96,248.0 15.3 1.0 4.3

Oman 6,555.32 (0.0) (0.0) (0.0) 3.3 5.86 25,621.4 9.9 1.6 4.0

Bahrain 1,330.38 (0.1) (0.1) (0.1) (6.7) 0.19 20,807.6 8.5 0.9 5.3

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,600

11,650

11,700

11,750

11,800

11,850

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QSE Index fell 1.1% to close at 11,651.3. The Telecoms and Real Estate

indices led the losses. The index fell on the back of selling pressure from

GCC shareholders despite buying support from Qatari and non-Qatari

shareholders.

Barwa Real Estate Co. and Qatar Gen. Ins. & Reins. Co. were the top losers,

falling 5.0% and 4.5%, respectively. Among the top gainers, Qatar Insurance

Co. rose 2.8%, while Gulf Warehousing Co. was up 2.5%.

Volume of shares traded on Sunday fell by 4.5% to 4.2mn from 4.4mn on

Thursday. Further, as compared to the 30-day moving average of 4.8mn,

volume for the day was 12.1% lower. Masraf Al Rayan and Vodafone Qatar

were the most active stocks, contributing 16.7% and 14.2% to the total

volume, respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue (mn)

2Q2015

% Change

YoY

Operating Profit

(mn) 2Q2015

% Change

YoY

Net Profit (mn)

2Q2015

% Change

YoY

Sanad Insurance &

Reinsurance Cooperative Co.

Saudi Arabia SAR -0.8 NA – – 3.7 NA

Amana Cooperative Insurance

Co.

Saudi Arabia SAR 125.4 15.4% – – 1.8 NA

Tihama Advertising & Public

Relations Co.

Saudi Arabia SAR – – -12.5 NA -11.5 NA

National Agriculture Marketing

Co. (Thimar)

Saudi Arabia SAR – – 0.9 -64.4% 2.5 -18.0%

Middle East Specialized Cables

Co.

Saudi Arabia SAR – – -7.7 NA -10.4 NA

Saudi Paper Manufacturing Co.

(SPMC)

Saudi Arabia SAR – – 5.8 -72.6% -3.4 NA

Saudi Cable Co. (SCC) Saudi Arabia SAR – – -17.4 NA 0.9 NA

Arabian Aramco Total Services

Co.

Saudi Arabia SAR – – 945.5 NA 748.7 NA

Solidarity Saudi Takaful Co.

(SSTC)

Saudi Arabia SAR 53.3 233.7% – – 7.3 NA

Etihad Etisalat Co. (Mobily) Saudi Arabia SAR – – -817.0 NA -900.9 NA

Wafrah for Industry and

Development Co.

Saudi Arabia SAR – – 0.8 -66.1% 0.5 -76.4%

Mohammad Al Mojil Group

(MMG)

Saudi Arabia SAR – – -78.2 NA -82.0 NA

Kingdom Holding Co. (KHC) Saudi Arabia SAR – – 353.7 -3.4% 238.3 12.6%

National Gas and

Industrialization Co.

Saudi Arabia SAR – – 39.1 19.1% 27.4 -28.2%

Emaar Properties Dubai AED 3,484.0 NA – – 1,179.0 NA

Unikai Foods Dubai AED 88.0 -7.2% 6.5 NA 6.7 NA

Agthia Group* Abu Dhabi AED 911.0 NA – – 125.0 NA

Bahrain Kuwait Insurance

Company (BKIC)*

Bahrain BHD – – – – 1.8 -30.8%

Mezzan Holding Co. Kuwait KD 51.6 NA – – 7.3 NA

Source: Company data, DFM, ADX, MSM (*1H2015 results)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 65.99% 59.83% 11,258,796.07

GCC 5.91% 13.10% (13,158,403.91)

Non-Qatari 28.10% 27.06% 1,899,607.84

3. Page 3 of 6

News

Qatar

AKHI’s bottom-line slumps in 2Q2015 on lower investment gains –

Al Khaleej Takaful Group’s (AKHI) net profit slumped 76.7% QoQ

(down 75.5% YoY) to QR5.7mn. The bottom-line contracted as

AKHI’s total investment & other income dropped 52.5% QoQ

(down 42.8% YoY) to QR16.7mn, which in-turn was primarily

impacted by a decline in net realized gain on sale of available-for-

sale investments from QR23.3mn in 1Q2015 to QR3.4mn in

2Q2015. The EPS amounted to QR0.22 in 2Q2015 versus QR0.96 in

1Q2015. (QSE, QNBFS Research)

MDPS: Qatar PPI falls 36.2% YoY in May on lower crude & gas prices

– According to statistics released by the Ministry of Development

Planning and Statistics (MDPS), Qatar’s producer price index (PPI)

plunged 36.2% YoY in May 2015 led by a double-digit decline in

the prices for crude and natural gas as well as refined petroleum

products, basic metals and basic chemicals. However, the PPI for

the industrial sector – a measure of the average selling prices

received by domestic producers for their output – rose 3.2% MoM

on higher prices of crude, basic chemicals, refined petroleum

products and man-made fibers. The PPI for mining, which carries

the maximum weight of 77%, reported a 40.3% YoY plunge in May

2015 due to a 40.3% decline in the prices of crude petroleum and

natural gas, while stone, sand and clay prices firmed up 2.2%. On

the other hand, the mining sector PPI saw a 3.4% MoM surge in

May owing to a 3.4% rise in the price of crude petroleum and

natural gas even as stone, sand and clay prices fell 0.7%. The

manufacturing sector, which has a weight of 21% in the PPI

basket, reported a 25.5% YoY decline in May 2015, driven by a

31% plunge in the price of refined petroleum goods, 19.7% in

basic chemicals, 14.9% in basic metals and 0.1% in paper and

paper products. However, there was a 6.9% increase in the price of

dairy products, 5.9% in beverages, 5.3% in cement and other non-

metallic products, 3.1% in juices, 1% in other chemical products,

man-made fibers, 0.6% in rubber and plastic products and 0.5% in

grain mill and other products. The manufacturing sector PPI

witnessed a 2.9% MoM expansion on account of a 5.4% increase in

the price of basic chemicals, 2.9% in refined petroleum products,

1.3% in other chemical products, man-made fibers, 0.4% in

cement and other non-metallic products and 0.1% in grain mill

and other products. However, there was a 0.4% fall in the price of

rubber and plastic products, 0.3% in basic metals, 0.2% in dairy

products and 0.1% each in juices and beverages. The electricity

and water group PPI (2% weight) gained 2.3% YoY (-0.7% MoM)

in May. (Gulf-Times.com)

Ashghal issues 11 tenders – A local Arabic daily Arrayah has

reported that the Public Works Authority (Ashghal) has recently

issued 11 tenders to implement a number of infrastructure

projects, most of which pertain to roads and drainage networks.

Most of these projects are open to Qatari companies only. One of

the tenders, valued at QR3.5mn, pertains to the development of

roads in the northern parts of Qatar. Another tender (QR2.5mn) is

for a project that involves designing and creating key elements of a

drainage system. There is also a tender for a service contract to

check and clean sewage networks (QR2.45mn) as well as a

contract to design and create a system for treated sewage water

(QR2.5mn). Meanwhile, Ashghal has announced that four north-

bound lanes on a section of Al Shamal Road will be closed for four

months from August 5, 2015 to facilitate infrastructure works.

Traffic will be diverted to the opposite side of the road, which will

be divided into two lanes in each direction. (Gulf-Times.com)

Al Daayen Municipality areas witness rapid urban expansion –

According to local Arabic daily Arrayah, areas falling under Al

Daayen Municipality have seen significant urban expansion in

recent times, with around 6% of Qataris living there. Director of

the Municipal Affairs Department at Al Daayen Municipality,

Mohamed Hassan al-Nuaimi stressed that the area is rapidly

becoming a major destination for inhabitants and municipal

services are being developed at a swift pace. Areas where new

plots of land have been given to Qataris have seen significant

construction works. According to the latest statistics, 1,017

requests for building permits were received in 2014 by the

development and building permits section. The section issued 703

building permits, 787 building completion certificates, 61

maintenance permits, 21 demolition permits, 49 temporary

licenses to manage projects and 20 permits for fencing works over

the same period. (Gulf-Times.com)

QA in new code share pact with RJ – Royal Jordanian (RJ) has

further enhanced ties with oneworld partner Qatar Airways (QA)

by signing a new code share agreement that is set to further

expand travelling opportunities for the customers of both airlines.

The new agreement, which will be activated on August 6, 2015,

will benefit RJ passengers travelling between Amman and Doha on

both RJ and QA. (Gulf-Times.com)

Qatar’s beIN signs three-year deal with Bundesliga – After securing

the Middle East and North Africa broadcast rights for Olympic

games between 2018 and 2024 from the International Olympic

Committee (IOC), Qatar’s beIN Media Group reached another

milestone by striking a deal with Bundesliga. The German League

and beIN Media Group have reached a global media rights

agreement beginning in the 2016-2017 season that will make the

Bundesliga available to “hundreds of millions” of fans across

MENA region, Europe, and Asia. The length of the contract is three

years. (Peninsula Qatar)

International

Greek financial markets reopen after five weeks – Greek financial

markets reopened on Monday after a five-week suspension as

talks continue with creditors on austerity measures and reforms

required for a third bailout. According to the Finance Ministry,

local traders will be able to buy stocks, bonds, derivatives and

warrants under certain conditions. International investors would

not face any restrictions, as long as they were active in the markets

before they were shuttered in June. The resumption of trading

comes as Prime Minister Alexis Tsipras negotiates conditions that

will be attached to an €86bn lifeline to see the country through the

next three years. An agreement is needed before a payment which

is due on bonds held by the European Central Bank on August 20,

2015. (Bloomberg)

China car sales drop flashes yellow light for economy – Car sales in

China is falling, a symbol of steady deceleration in the economy. In

contrast, when the economy was booming, motorists became a

symbol of China’s new spending power. Voracious demand saw

China overtake the US as the world’s biggest car market in 2009,

spurring auto giants including Ford Motor and Volkswagen to

supercharge their production in the country. However, Ford now

sees a potential decline in auto sales in China for the first time in

17 years. Volkswagen suffered its first sales drop in a decade

during 1H2015. New car sales fell in June for the first time in more

than two years. Ford projects the market at as small as 23mn units

in 2015, as compared to 23.5mn vehicles sold in 2014. Hyundai

Motor has also said its deliveries have fallen. Since car demand is

often a timely indicator of consumer and business confidence, it

can capture economic trends before official data. The deterioration

comes at a time when President Xi Jinping and Premier Li Keqiang

want consumers and services to play a bigger role in driving the

economy as part of a shift away from debt-fueled investment and

exports. (Bloomberg)

4. Page 4 of 6

Australia new home sales rebound in June – Sales of new homes in

Australia bounced in June after a dip in the previous month to hold

at near their highest level in at least five years. The Housing

Industry Association (HIA) said its survey of large volume builders

showed sales of new homes rose a seasonally adjusted 0.5% MoM

in June. Sales of detached homes rebounded by 1.7% in June to

offset a 2.9% decline in multi-units. Meanwhile, figures released by

property consultant CoreLogic showed dwelling prices across all

of Australia’s major cities surged 2.8% in July, on top of a 2.1%

jump in June. Annual growth in home values picked up to 11.1%,

from 9.8% in June. Australia is in the midst of a boom in home

building thanks to relatively rapid population growth and

historically low mortgage rates, after the Reserve Bank of Australia

(RBA) cut its rates to a record low of 2.0% in May. (Reuters)

Regional

GCC’s $86bn infrastructure investments augur well for materials

handling – Multi-billion dollar investments in GCC commercial and

civil infrastructure projects are having a positive impact on the

materials handling sector, as the region's dedicated logistics and

warehousing trade show reaches full capacity ahead of its

September opening in Dubai. According to industry reports, the

Gulf region awarded infrastructure projects worth $86bn in 2014,

78% over 2013, with the increased investments fueling demand

for providers of logistics, transportation, materials handling, and

supply chain solutions. The upbeat sentiment is underlined by the

industry's biggest names exhibiting at Materials Handling Middle

East 2015, which has sold out all exhibition space, and will take

place during September 14-16, 2015 at the Dubai International

Convention & Exhibition Center. (Gulf-Base.com)

Saudi electricity sector needs SR700bn investments over next 10

years – Deputy Minister For Water & Electricity and Chairman of

the Saudi Electricity Company (SEC), Saleh bin Hussein Al-Awaji

said the Saudi electricity sector needs an estimated SR700bn

investment in the next 10 years, with a large percentage expected

from the private sector. He said that new plans were launched for

the establishment of companies provided with specialized staff to

design and implement projects in the electricity sector throughout

the Kingdom, adding that this national trend encouraged the SEC

to establish the SEC for Projects Development, an engineering

company wholly-owned by SEC. Al-Awaji added that projects in

the electricity sector and the labor market indicate that this new

company will only meet about 25% of SEC's needs, which gives an

indication of the magnitude of the Saudi market and the available

opportunities to other competitors. He said that other companies

are planned to be established, such as the independent electricity

production companies, in cooperation with the private sector,

confirming that there are other companies producing electricity,

such as Saudi Aramco and the General Establishment for Water

Desalination (GEWD), along with a number of private companies.

(Gulf-Base.com)

HERFY opens 7 new stores during July 2015 – HERFY Food Services

Company has opened 7 new stores in various regions across the

Kingdom during July 2015, taking the total number of new HERFY

stores to 28, opened during January 1, 2015 to July 31, 2015. This

is part of the company’s expansion plan in the fast food sector with

its 283 units. (Gulf-Base.com)

Tadawul publishes July 2015 trading statistics – According to the

Saudi Stock Exchange’s (Tadawul) trading statistics report

(Nationality & Investor Type), the total value of shares traded

reached SR84.14bn during July 2015, reflecting a decrease of

25.17% MoM. The value of shares traded by Saudi Arabia stood at

SR80.02bn (94.80%) for buying and SR80.19bn (95.00%) for

selling. The value of shares traded by GCC amounted to SR1.94bn

(2.30%) for buying and SR1.53bn (1.81%) for selling. The value of

shares traded by Foreigners (Resident, SWAP & QFI) reached

SR2.44bn (2.89%) for buying and SR2.69bn (3.19%) for selling.

(Tadawul)

Saudi CMA lifts trading suspension of Mobily shares from August 3 –

The Saudi Capital Market Authority (CMA) has lifted the trading

suspension of Etihad Etisalat Company’s (Mobily) shares starting

from August 3, 2015. (Tadawul)

IMF: UAE economy to grow 3.2% in 2015 – According to the

International Monitory Fund (IMF), the average estimated

economic growth of the UAE was 3.6% in 2014, and is expected to

be 3.2% in 2015, among the highest in the area. Financially, the

IMF expects a retreat in the surplus of current account from 12.1%

of the GDP in 2014 to around 5.3% in 2015, due to the decline in

international oil prices. Further, the IMF expects inflation in the

UAE to average 2.1% in 2015 as compared to 2.3% in 2014. (Gulf-

Base.com)

GFH signs restructuring agreement for Villamar project – GFH

Financial Group has informed its shareholders and markets that it

has recently signed a restructuring agreement toward the

remobilization of the Villamar Project, which is based in the

Bahrain Financial Harbour. Gulf Holding Company, the developer

of the Villamar Project, has inked the restructuring agreement

with Al Rajhi Bank as the original financiers of the project, GFH

Financial Group as the project's new financiers, and Al Hamad

Construction as the project's contractor. (DFM)

Abu Dhabi GDP expands 5.8% in 1Q2015 – Chairman of the

Department of Economic Development (DED) Abu Dhabi, Ali Majid

Al-Mansouri said that the local economy of Abu Dhabi has

recorded new overall economic growth levels, by the end of 2014,

given the noticeable improvement in the non-oil sectors

performance, as figures show a real GDP growth of 5.8% in

1Q2015. Al-Mansouri clarified that the results of the development

indicators during 1Q2015 showed improvements in the levels of

trust among consumers and business establishments in reference

to the economic situation at the Emirate. He was speaking on the

occasion of release of the “Economic Performance of the Emirate of

Abu Dhabi Follow-Up Report” by the Economic Development

Department of Abu Dhabi. (GulfBase.com)

CBRE: Residential rents rise 1% in Abu Dhabi – According to real

estate consultancy firm CBRE, average residential rents in Abu

Dhabi continued to remain stable with just over 1% increase in

2Q2015. It was the lowest quarterly rise in two years. However, in

annual terms, the rental growth still looks substantial at around

10%, reflecting the relative strength of the market during 2014.

According to the report, luxury apartment residences within

master planned communities remained in strong demand amid

relatively limited new supply. This equated to a 14% increase in

rent levels during the past year alone. (Gulf-Base.com)

ENOC raises offer to acquire Dragon Oil – Emirates National Oil

Company (ENOC) increased its offer to buy Dragon Oil to 800

pence a share winning support from minority owners including

billionaire Paul Singer’s Elliott Advisors UK Ltd. that rejected

ENOC’s offer in June. ENOC said that Elliott and Baillie Gifford &

Company, which hold a combined 13.1% stake in Dragon Oil, have

accepted the new price. ENOC’s new offer is unconditional and

final. ENOC had offered to buy the 46% of Dragon Oil it did not

own for 750 pence a share, or £1.7bn on June 15, 2015.

(Bloomberg)

CI affirms Oman ratings – International credit rating agency,

Capital Intelligence (CI) has affirmed Oman’s long-term foreign

currency and local currency ratings of ‘A’ and its short-term

foreign and local currency rating at ‘A1’. The outlook for Oman’s

ratings remains at stable. The rating agency in February 2015 had

said that the economy is expected to continue its steady growth

5. Page 5 of 6

averaging 3.5% during 2015-16, driven by growth in the non-

hydrocarbon sectors and supported by Gulf Cooperation Council

(GCC) funded infrastructure projects. (Gulf-Base.com)

ONEIC awards OMR4mn meter reading & billing collection contract

– Oman National Engineering & Investment Company (ONEIC) has

been awarded a contract of meter reading & billing collection in all

provinces except Muscat. The contract, worth OMR4mn, is for a

period of eleven months. (MSM)

Tamkeen signs agreement with Ithmaar Bank for finance scheme

portfolio – Tamkeen and Ithmaar Bank have signed an agreement

to add BHD10mn to their joint enterprise finance scheme

portfolio. Tamkeen Chairman and Acting Chief Executive Shaikh

Mohammed bin Essa Al Khalifa said that the company seeks to

help enterprises achieve their developmental goals and provide

them with expansion and growth opportunities through its various

programs. This includes financing solutions that make it easier for

these enterprises to succeed in their ventures and projects. With

the signing of this agreement, the total financing offered through

Tamkeen’s finance scheme in cooperation with partner banks

reached BHD372.5mn. More than 6,000 enterprises have benefited

from the program. (Gulf-Base.com)

Batelco launches online portal for enterprise customers – Bahrain

Telecommunication Company (Batelco) has launched an online

portal for the enterprise sector. This functionality is the latest

addition to the already established Batelco eServices, which allows

corporate customers to log in to the portal by inputting their

Commercial Registration (CR) number. (Bahrain Bourse)

6. Contacts

Saugata Sarkar Sahbi Kasraoui QNB Financial Services SPC

Head of Research Head of HNI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 PO Box 24025

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the Qatar Financial

Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or

recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect

losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore

strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS

believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and

completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or

contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the

views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions

included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

Jul-11 Jul-12 Jul-13 Jul-14 Jul-15

QSE Index S&P Pan Arab S&P GCC

(3.2%)

(1.1%)

(0.3%) (0.1%) (0.0%)

(0.9%) (0.9%)

(4.0%)

(3.0%)

(2.0%)

(1.0%)

0.0%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,095.82 0.7 (0.3) (7.5) MSCI World Index 1,765.60 0.3 1.2 3.3

Silver/Ounce 14.78 0.2 0.6 (5.9) DJ Industrial 17,689.86 (0.3) 0.7 (0.7)

Crude Oil (Brent)/Barrel (FM

Future)

52.21 (2.1) (4.4) (8.9) S&P 500 2,103.84 (0.2) 1.2 2.2

Crude Oil (WTI)/Barrel (FM

Future)

47.12 (2.9) (2.1) (11.5) NASDAQ 100 5,128.28 (0.0) 0.8 8.3

Natural Gas (Henry

Hub)/MMBtu

2.77 (2.8) (1.7) (7.6) STOXX 600 396.37 0.9 0.7 5.2

LPG Propane (Arab Gulf)/Ton 37.75 (2.6) (9.3) (23.0) DAX 11,308.99 1.3 (0.1) 4.4

LPG Butane (Arab Gulf)/Ton 50.38 (1.9) (5.4) (23.1) FTSE 100 6,696.28 0.7 2.5 2.3

Euro 1.10 0.5 0.0 (9.2) CAC 40 5,082.61 1.5 0.7 8.2

Yen 123.89 (0.2) 0.1 3.4 Nikkei 20,585.24 0.6 0.0 13.7

GBP 1.56 0.1 0.7 0.3 MSCI EM 901.68 0.9 (1.0) (5.7)

CHF 1.03 0.3 (0.3) 2.9 SHANGHAI SE Composite 3,663.73 (1.1) (10.0) 13.2

AUD 0.73 0.2 0.4 (10.6) HANG SENG 24,636.28 0.6 (2.0) 4.4

USD Index 97.34 (0.2) 0.1 7.8 BSE SENSEX 28,114.56 1.7 0.2 1.0

RUB 61.71 3.3 5.3 1.6 Bovespa 50,864.77 0.4 0.9 (21.3)

BRL 0.29 (1.4) (2.0) (22.5) RTS 858.82 (1.0) (0.0) 8.6

139.4

121.4

116.7