Activity Based Costing: 5. Differenze tra Activity Based Costing e i tradizionali costi di prodotto

•

1 like•2,443 views

Miglioramenti dei processi https://www.manager.it/default.asp?page=A_contabilita.html

Recommended

Recommended

More Related Content

What's hot

What's hot (18)

Viewers also liked

Viewers also liked (6)

Similar to Activity Based Costing: 5. Differenze tra Activity Based Costing e i tradizionali costi di prodotto

Similar to Activity Based Costing: 5. Differenze tra Activity Based Costing e i tradizionali costi di prodotto (20)

More from Manager.it

More from Manager.it (20)

Recently uploaded

Recently uploaded (20)

Activity Based Costing: 5. Differenze tra Activity Based Costing e i tradizionali costi di prodotto

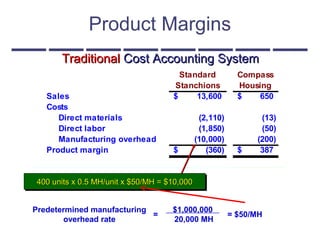

- 1. Product Margins Standard Stanchions Compass Housing Sales 13,600$ 650$ Costs Direct materials (2,110) (13) Direct labor (1,850) (50) Manufacturing overhead (10,000) (200) Product margin (360)$ 387$ TraditionalTraditional Cost Accounting SystemCost Accounting System Predetermined manufacturing overhead rate $1,000,000 20,000 MH = $50/MH= 400 units x 0.5 MH/unit x $50/MH = $10,000400 units x 0.5 MH/unit x $50/MH = $10,000400 units x 0.5 MH/unit x $50/MH = $10,000400 units x 0.5 MH/unit x $50/MH = $10,000

- 2. Difference Between ABC and Traditional Product Costs Batch-level or product-Batch-level or product- level costs willlevel costs will ordinarily shiftordinarily shift overhead costs fromoverhead costs from high-volumehigh-volume products producedproducts produced in large batches toin large batches to low-volume productslow-volume products produced in smallproduced in small batches.batches. Batch-level or product-Batch-level or product- level costs willlevel costs will ordinarily shiftordinarily shift overhead costs fromoverhead costs from high-volumehigh-volume products producedproducts produced in large batches toin large batches to low-volume productslow-volume products produced in smallproduced in small batches.batches. Under ABC bothUnder ABC both manufacturing andmanufacturing and nonmanufacturingnonmanufacturing costs may becosts may be assigned to products.assigned to products. Organization-Organization- sustaining costs andsustaining costs and the costs of idlethe costs of idle capacity are notcapacity are not assigned to products.assigned to products. Under ABC bothUnder ABC both manufacturing andmanufacturing and nonmanufacturingnonmanufacturing costs may becosts may be assigned to products.assigned to products. Organization-Organization- sustaining costs andsustaining costs and the costs of idlethe costs of idle capacity are notcapacity are not assigned to products.assigned to products.

- 3. Targeting Process Improvement Activity-based costing can be used to identify areas that would benefit from process improvements. Activity-based costing can be used to identify areas that would benefit from process improvements. The theory of constraints approach is a powerful tool for targeting the area in an organization whose improvement will yield the greatest benefits. The theory of constraints approach is a powerful tool for targeting the area in an organization whose improvement will yield the greatest benefits.

- 4. Activity-Based Costing and External Reporting Most companies do not use ABC for external reporting because . . .Most companies do not use ABC for external reporting because . . . 1.1. External reports are less detailed than internalExternal reports are less detailed than internal reports.reports. 2.2. It may be difficult to make changes to the company’sIt may be difficult to make changes to the company’s accounting system.accounting system. 3.3. ABC does not conform to GAAP.ABC does not conform to GAAP. 4.4. Auditors may be suspect of the subjective allocationAuditors may be suspect of the subjective allocation process based on interviews with employees.process based on interviews with employees.

- 5. Limitations of ABC ABC systems are aABC systems are a major project requiringmajor project requiring substantial resources.substantial resources. The benefits ofThe benefits of increased accuracyincreased accuracy must outweigh thesemust outweigh these additional costs.additional costs. ABC systems are aABC systems are a major project requiringmajor project requiring substantial resources.substantial resources. The benefits ofThe benefits of increased accuracyincreased accuracy must outweigh thesemust outweigh these additional costs.additional costs. ABC producesABC produces numbers, like productnumbers, like product margins, that are atmargins, that are at odds with numbersodds with numbers produced by traditionalproduced by traditional costing system. Somecosting system. Some managers find itmanagers find it difficult to adjust to thisdifficult to adjust to this change.change. ABC producesABC produces numbers, like productnumbers, like product margins, that are atmargins, that are at odds with numbersodds with numbers produced by traditionalproduced by traditional costing system. Somecosting system. Some managers find itmanagers find it difficult to adjust to thisdifficult to adjust to this change.change. ABC data can be misinterpreted and mustABC data can be misinterpreted and must be used with care when making decisions.be used with care when making decisions. ABC data can be misinterpreted and mustABC data can be misinterpreted and must be used with care when making decisions.be used with care when making decisions.

- 6. Limitations of ABC ABC systems are aABC systems are a major project requiringmajor project requiring substantial resources.substantial resources. The benefits ofThe benefits of increased accuracyincreased accuracy must outweigh thesemust outweigh these additional costs.additional costs. ABC systems are aABC systems are a major project requiringmajor project requiring substantial resources.substantial resources. The benefits ofThe benefits of increased accuracyincreased accuracy must outweigh thesemust outweigh these additional costs.additional costs. ABC producesABC produces numbers, like productnumbers, like product margins, that are atmargins, that are at odds with numbersodds with numbers produced by traditionalproduced by traditional costing system. Somecosting system. Some managers find itmanagers find it difficult to adjust to thisdifficult to adjust to this change.change. ABC producesABC produces numbers, like productnumbers, like product margins, that are atmargins, that are at odds with numbersodds with numbers produced by traditionalproduced by traditional costing system. Somecosting system. Some managers find itmanagers find it difficult to adjust to thisdifficult to adjust to this change.change. ABC data can be misinterpreted and mustABC data can be misinterpreted and must be used with care when making decisions.be used with care when making decisions. ABC data can be misinterpreted and mustABC data can be misinterpreted and must be used with care when making decisions.be used with care when making decisions.