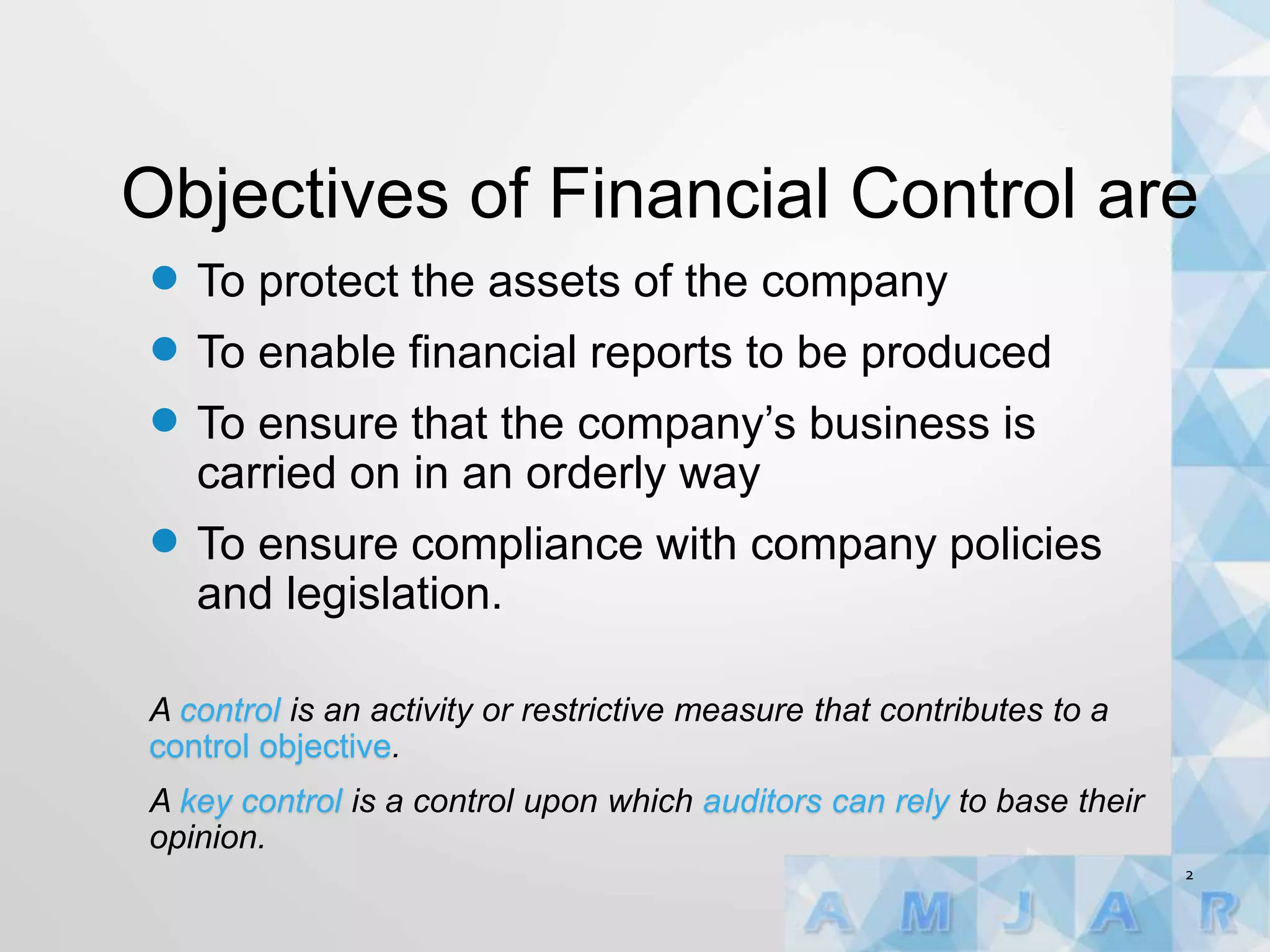

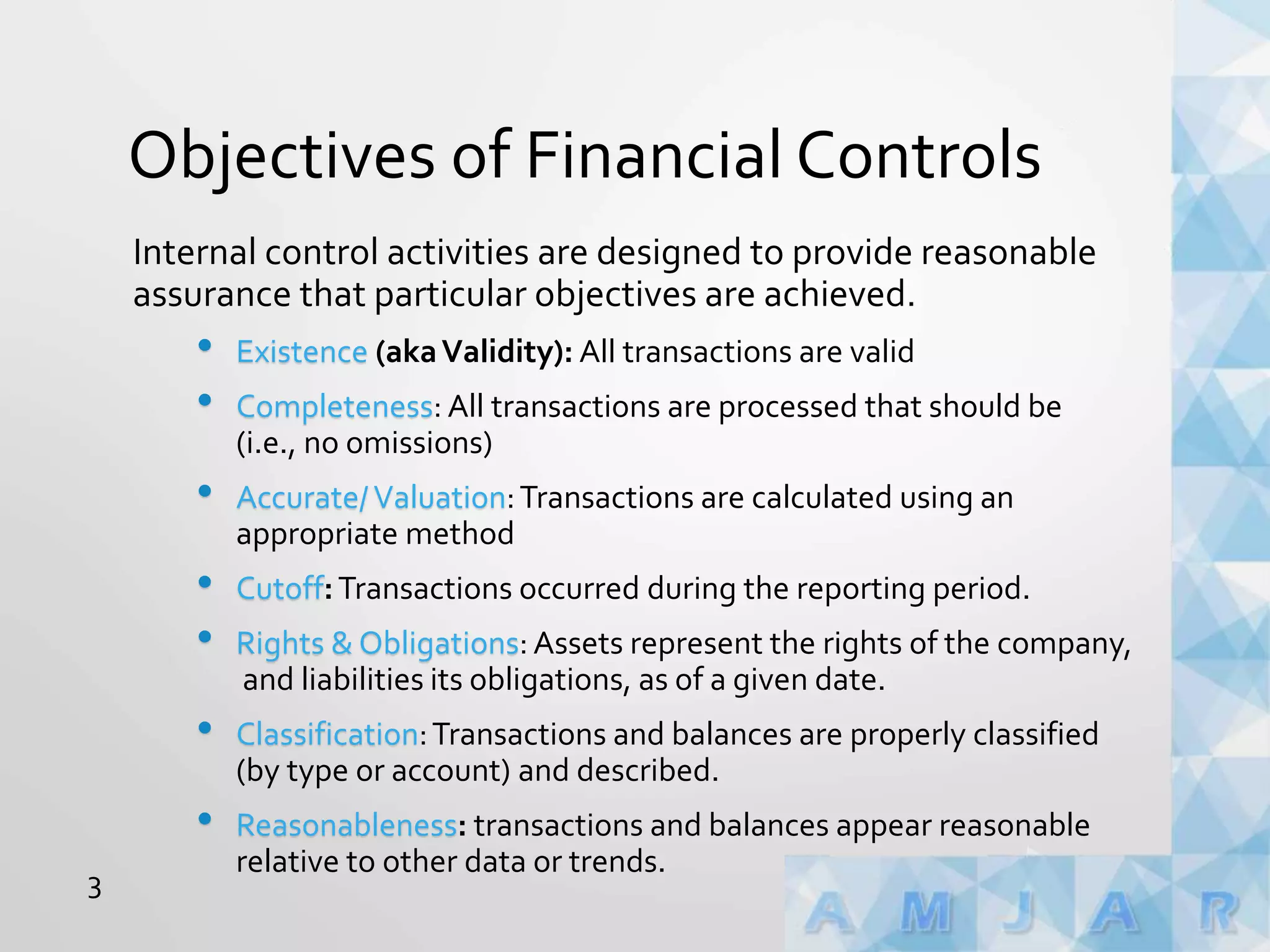

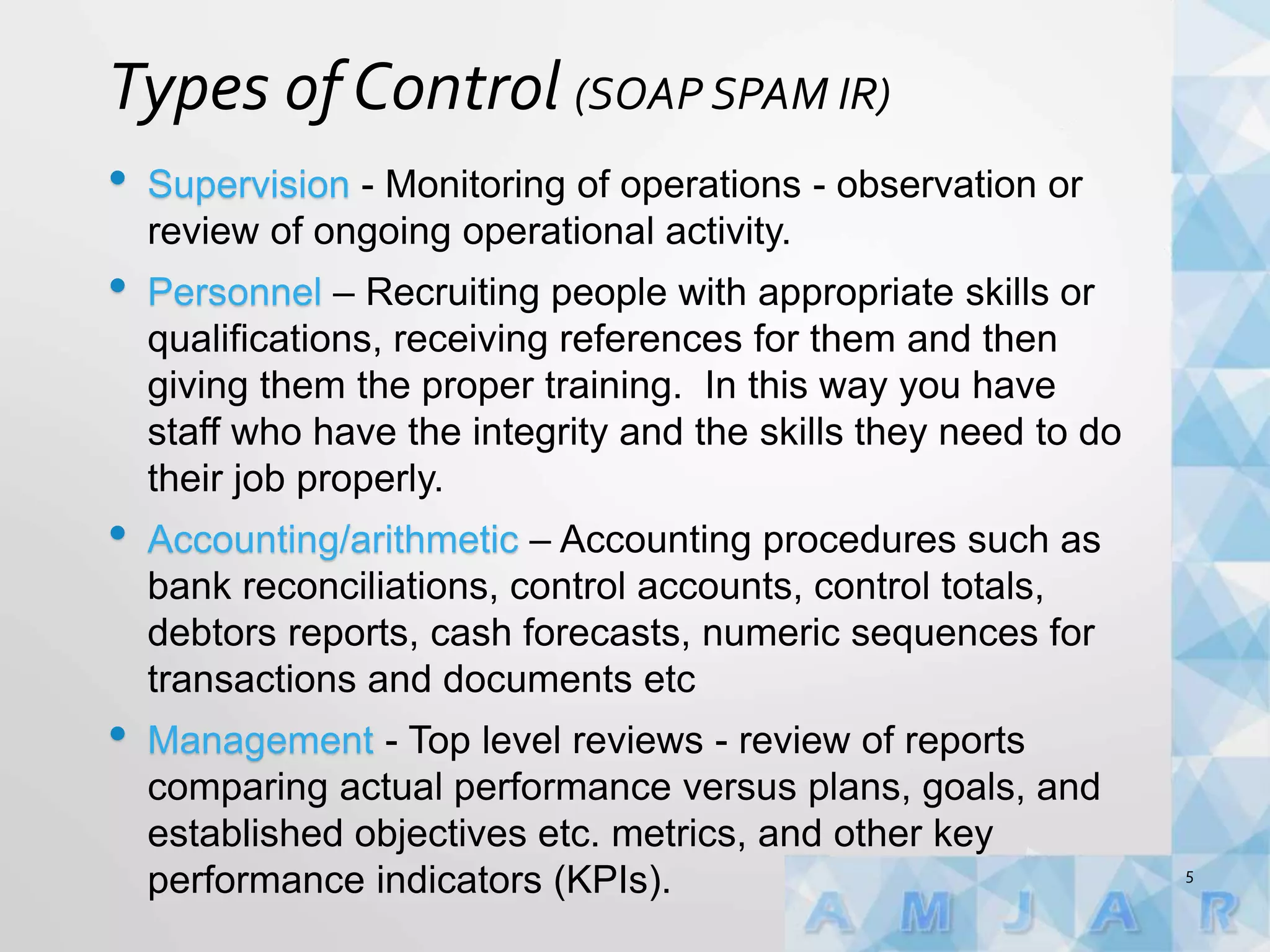

The document outlines the objectives of financial controls, which include protecting company assets, ensuring accurate financial reporting, and compliance with policies. It details various types of controls, such as segregation of duties, organisational controls, and authorisation, aimed at preventing fraud and ensuring the validity and completeness of transactions. Furthermore, it emphasizes internal control activities designed to provide reasonable assurance that financial reporting objectives are achieved.