1. The economic cycle refers to short-run fluctuations in national output (real GDP) around its long-term trend. It includes periods of boom, slowdown, recession, and recovery.

2. A recession is defined as at least six months of falling output across the economy. It can cause rising unemployment, falling business profits, and declining tax revenues.

3. Estimating the output gap, which is the difference between actual GDP and potential GDP, is difficult but important for understanding inflationary pressures and spare capacity in the economy. A negative output gap indicates unused resources while a positive gap risks inflation.

Introduction to the Trade Cycle, key stages: Boom, Slowdown, Recession, Recovery, Depression. Real GDP trends in the UK, with projections from IMF, highlighting growth potential and stages.

Explained concept of output gap, negative and positive gaps, and challenges in accurate measurement.

Examples of demand and supply shocks along with potential causes of recession in an economy.

Short-term impacts of recession on business, employment, government finances; long-term social effects.

Contrast between recession and depression, discussing economic consequences and historical context.

Summary of the Trade Cycle and its relation to output gap, reinforcing initial concepts.

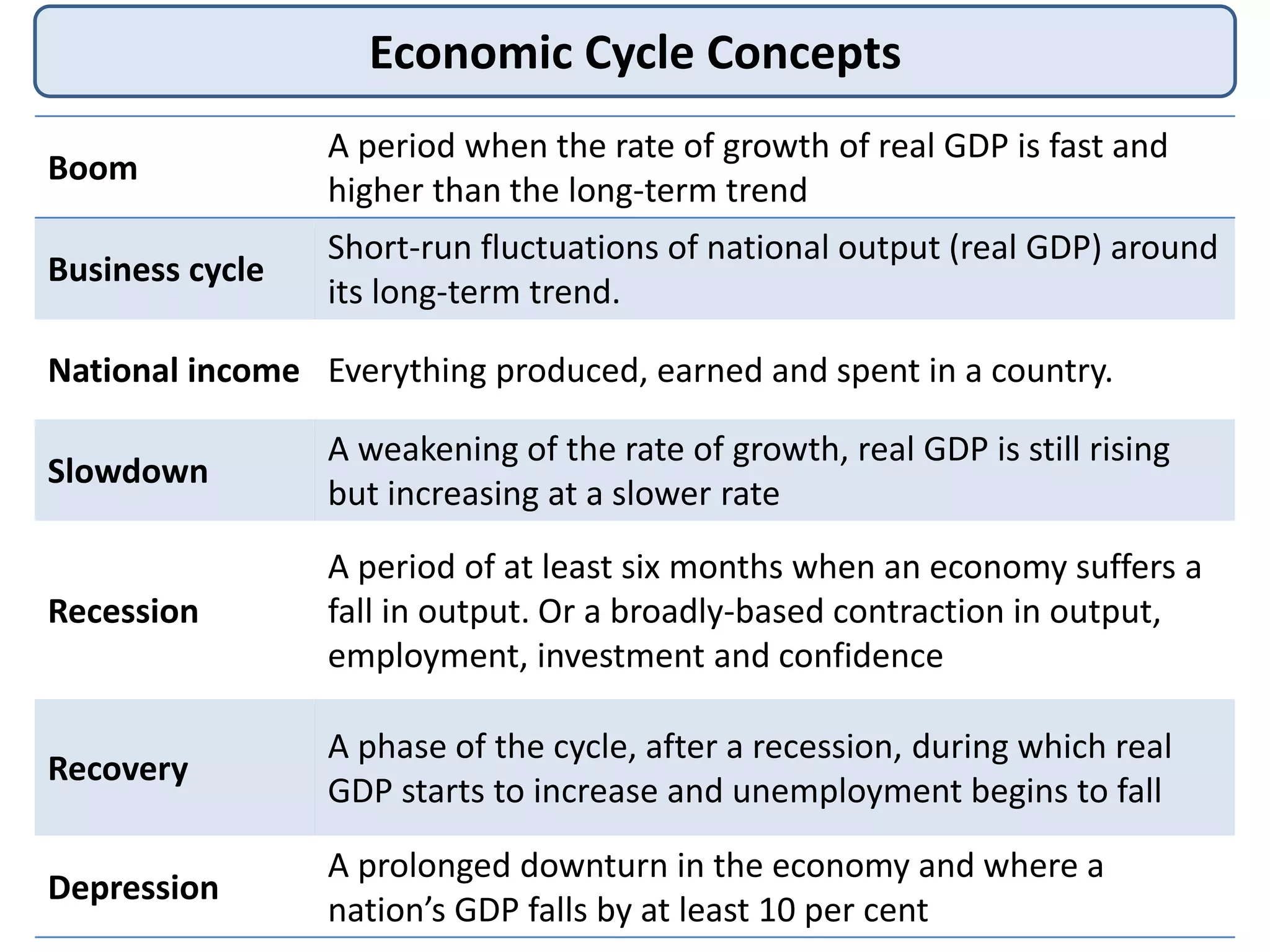

Economic Cycle Concepts

Boom

Aperiod when the rate of growth of real GDP is fast and

higher than the long-term trend

Business cycle

Short-run fluctuations of national output (real GDP) around

its long-term trend.

National income Everything produced, earned and spent in a country.

Slowdown

A weakening of the rate of growth, real GDP is still rising

but increasing at a slower rate

Recession

A period of at least six months when an economy suffers a

fall in output. Or a broadly-based contraction in output,

employment, investment and confidence

Recovery

A phase of the cycle, after a recession, during which real

GDP starts to increase and unemployment begins to fall

Depression

A prolonged downturn in the economy and where a

nation’s GDP falls by at least 10 per cent

3.

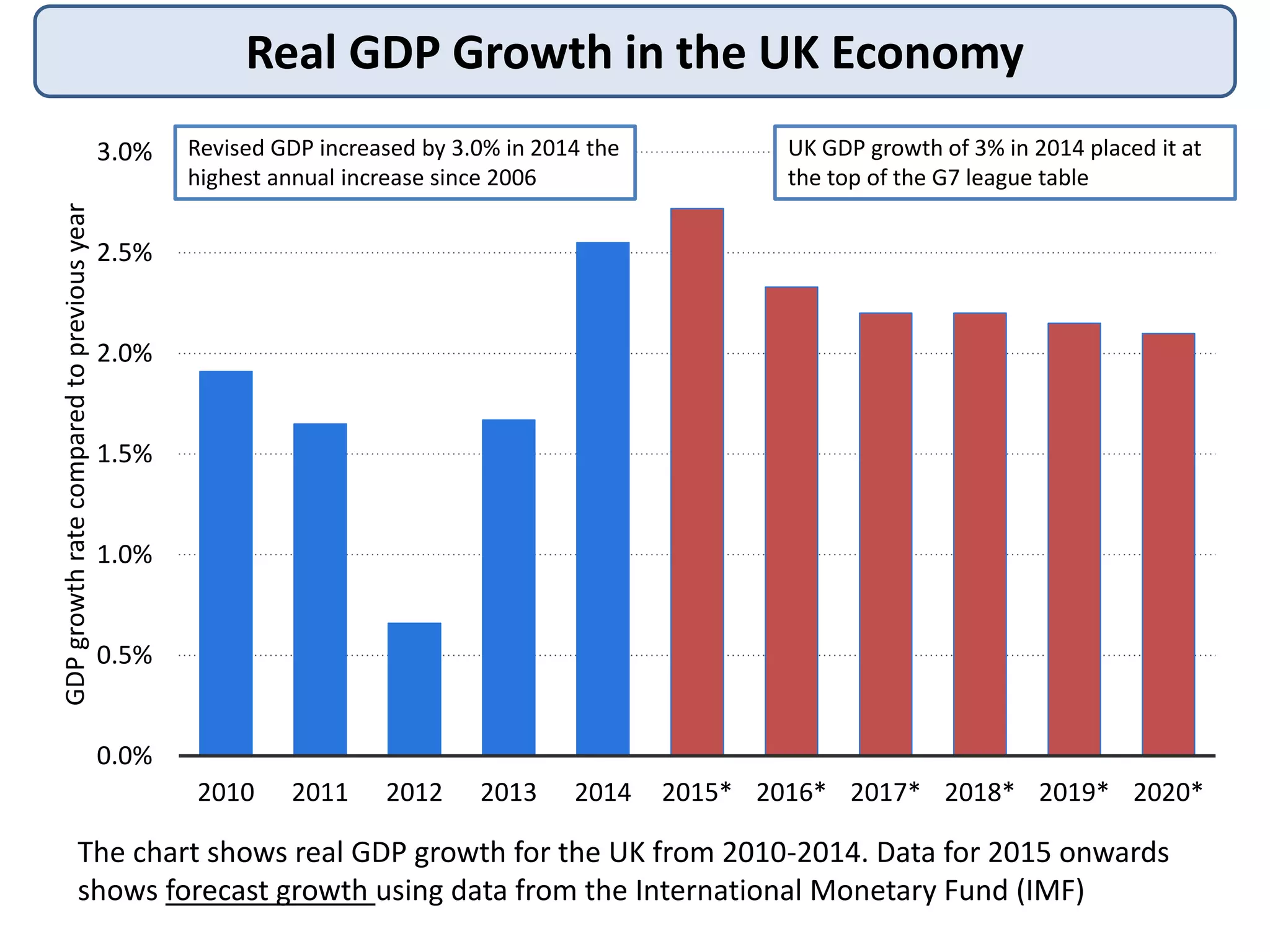

Real GDP Growthin the UK Economy

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2010 2011 2012 2013 2014 2015* 2016* 2017* 2018* 2019* 2020*

GDPgrowthratecomparedtopreviousyear

The chart shows real GDP growth for the UK from 2010-2014. Data for 2015 onwards

shows forecast growth using data from the International Monetary Fund (IMF)

UK GDP growth of 3% in 2014 placed it at

the top of the G7 league table

Revised GDP increased by 3.0% in 2014 the

highest annual increase since 2006

4.

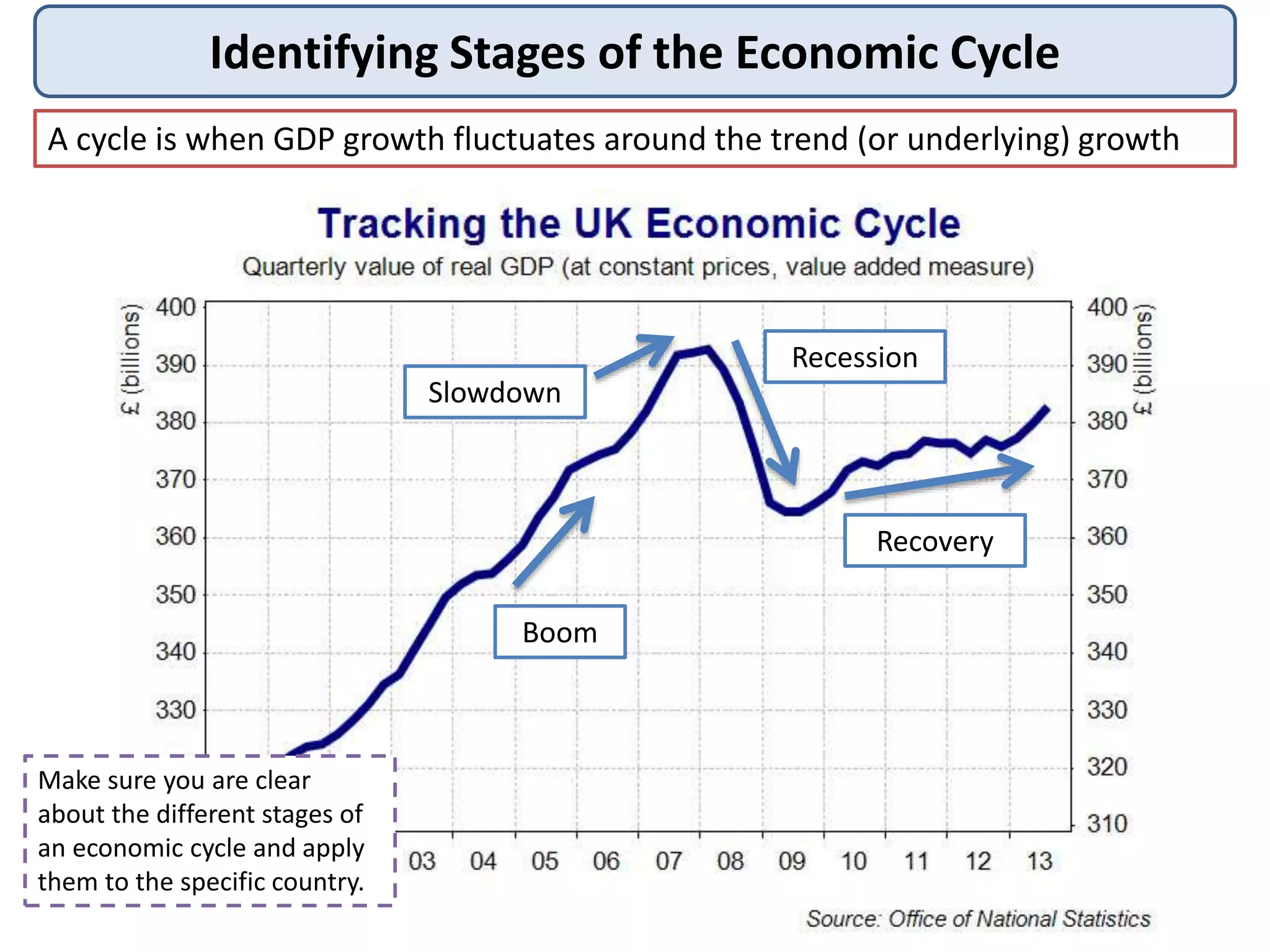

Identifying Stages ofthe Economic Cycle

Boom

Slowdown

Recession

Recovery

A cycle is when GDP growth fluctuates around the trend (or underlying) growth

Make sure you are clear

about the different stages of

an economic cycle and apply

them to the specific country.

5.

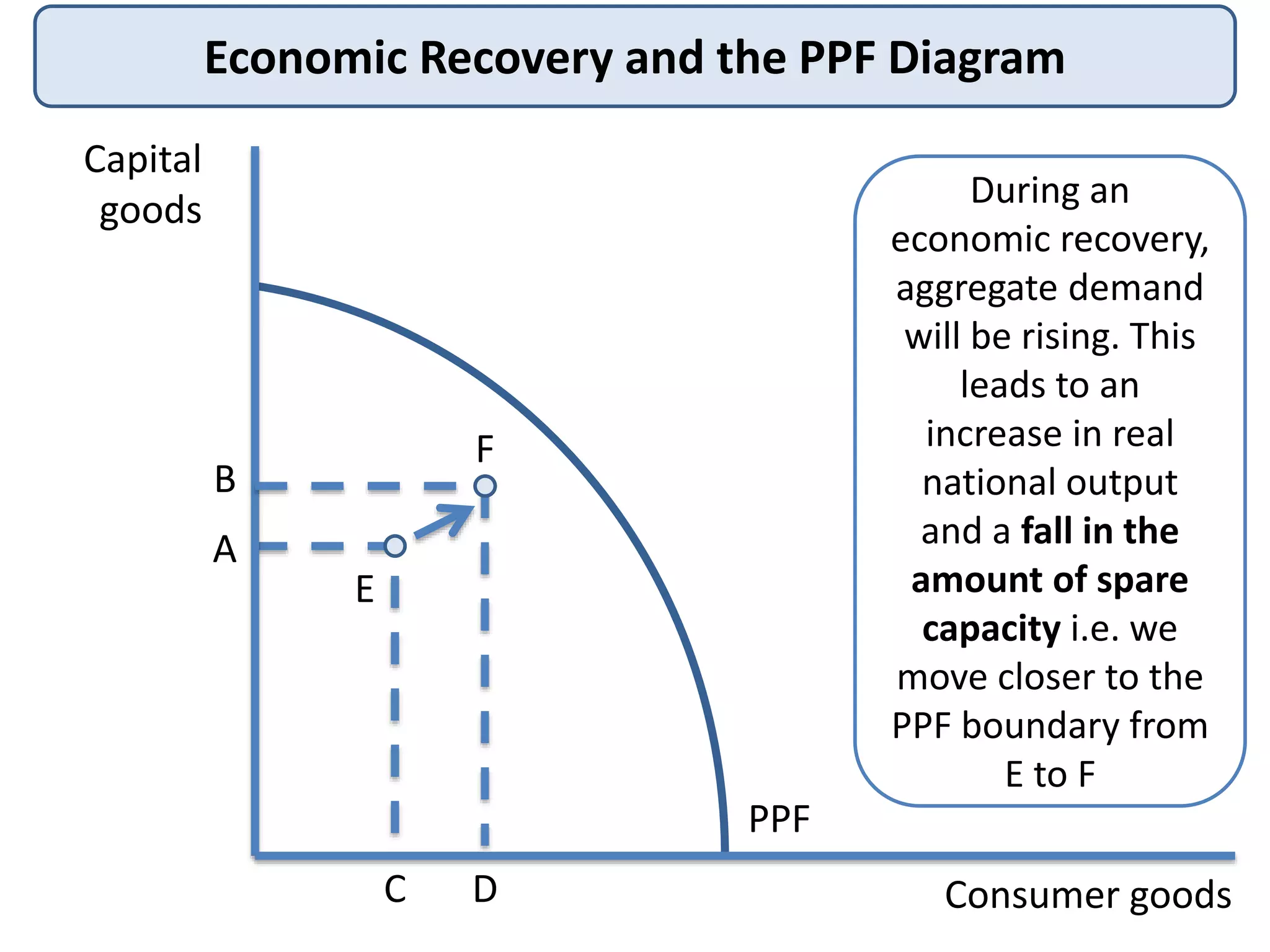

Economic Recovery andthe PPF Diagram

During an

economic recovery,

aggregate demand

will be rising. This

leads to an

increase in real

national output

and a fall in the

amount of spare

capacity i.e. we

move closer to the

PPF boundary from

E to F

Capital

goods

Consumer goods

PPF

A

B

C D

E

F

6.

-8% -6% -4%-2% 0% 2% 4% 6% 8%

Mining, oil, etc

Finance/insurance

Electricity & gas

Agriculture

Water & waste

Manufacturing

Other services

Construction

Hotels & restaurants

Property services

Transport & comms

Retail & wholesale

Prof & business services

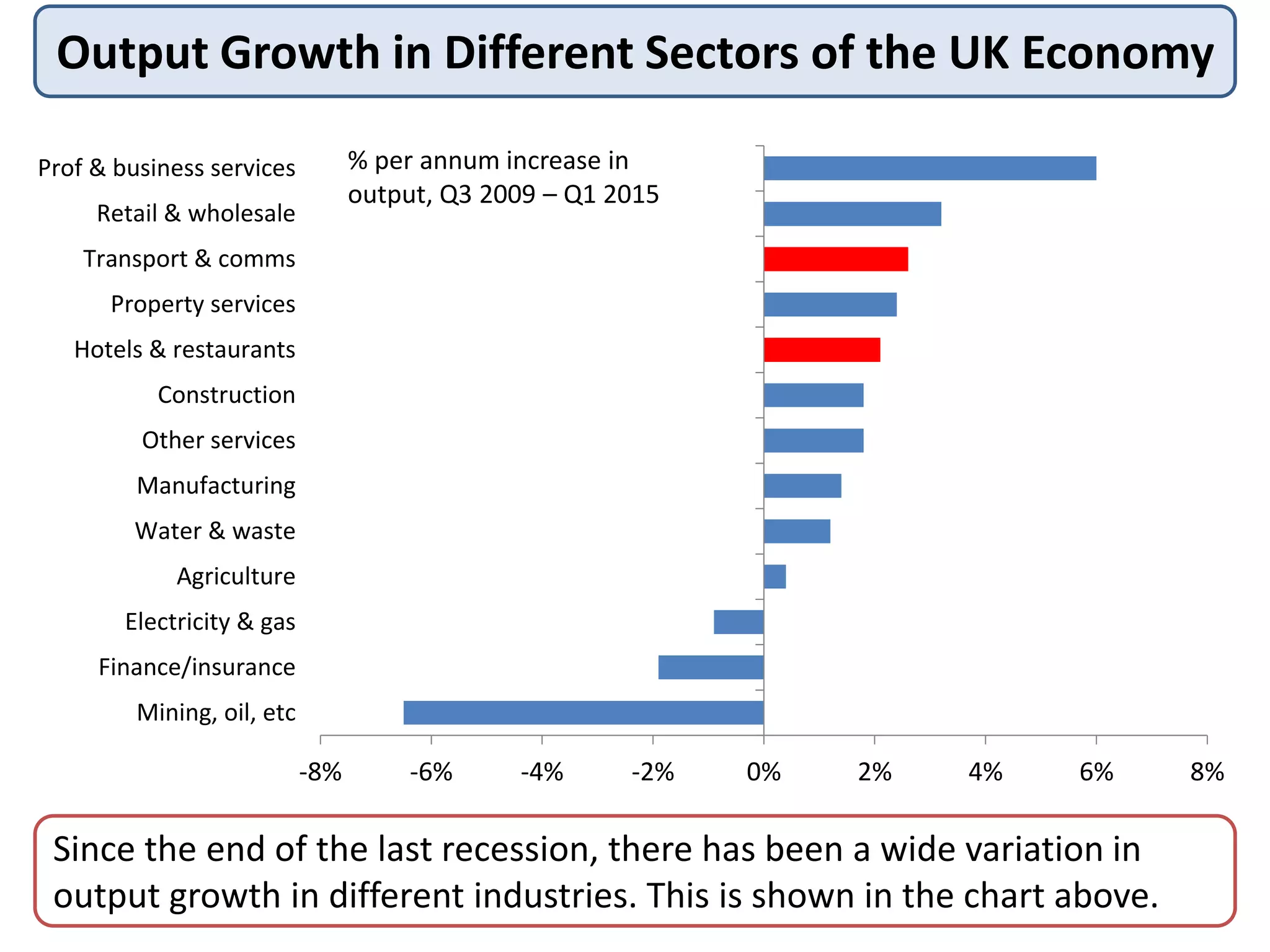

Output Growth in Different Sectors of the UK Economy

Since the end of the last recession, there has been a wide variation in

output growth in different industries. This is shown in the chart above.

% per annum increase in

output, Q3 2009 – Q1 2015

7.

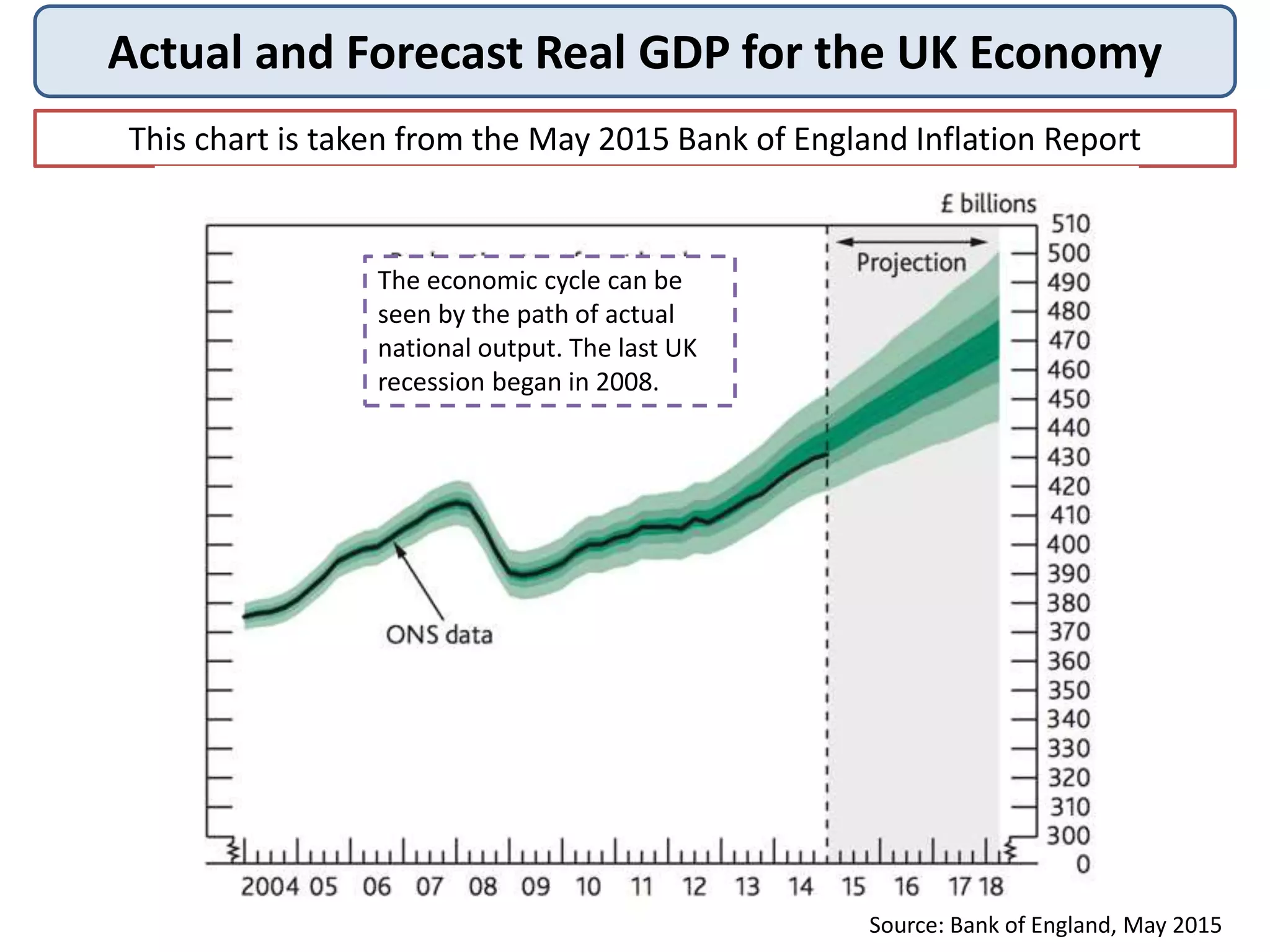

Actual and ForecastReal GDP for the UK Economy

This chart is taken from the May 2015 Bank of England Inflation Report

The economic cycle can be

seen by the path of actual

national output. The last UK

recession began in 2008.

Source: Bank of England, May 2015

8.

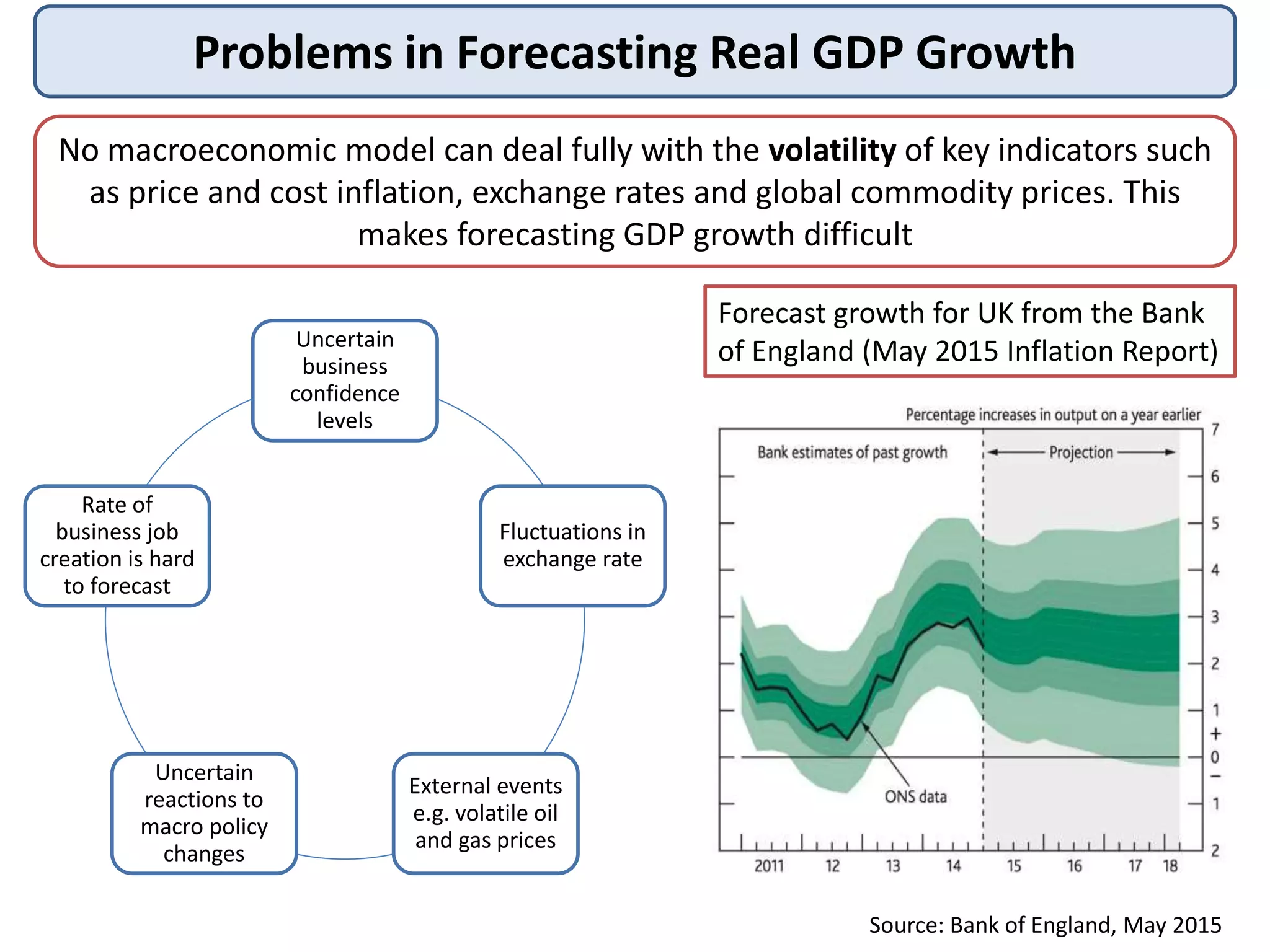

Problems in ForecastingReal GDP Growth

No macroeconomic model can deal fully with the volatility of key indicators such

as price and cost inflation, exchange rates and global commodity prices. This

makes forecasting GDP growth difficult

Uncertain

business

confidence

levels

Fluctuations in

exchange rate

External events

e.g. volatile oil

and gas prices

Uncertain

reactions to

macro policy

changes

Rate of

business job

creation is hard

to forecast

Forecast growth for UK from the Bank

of England (May 2015 Inflation Report)

Source: Bank of England, May 2015

9.

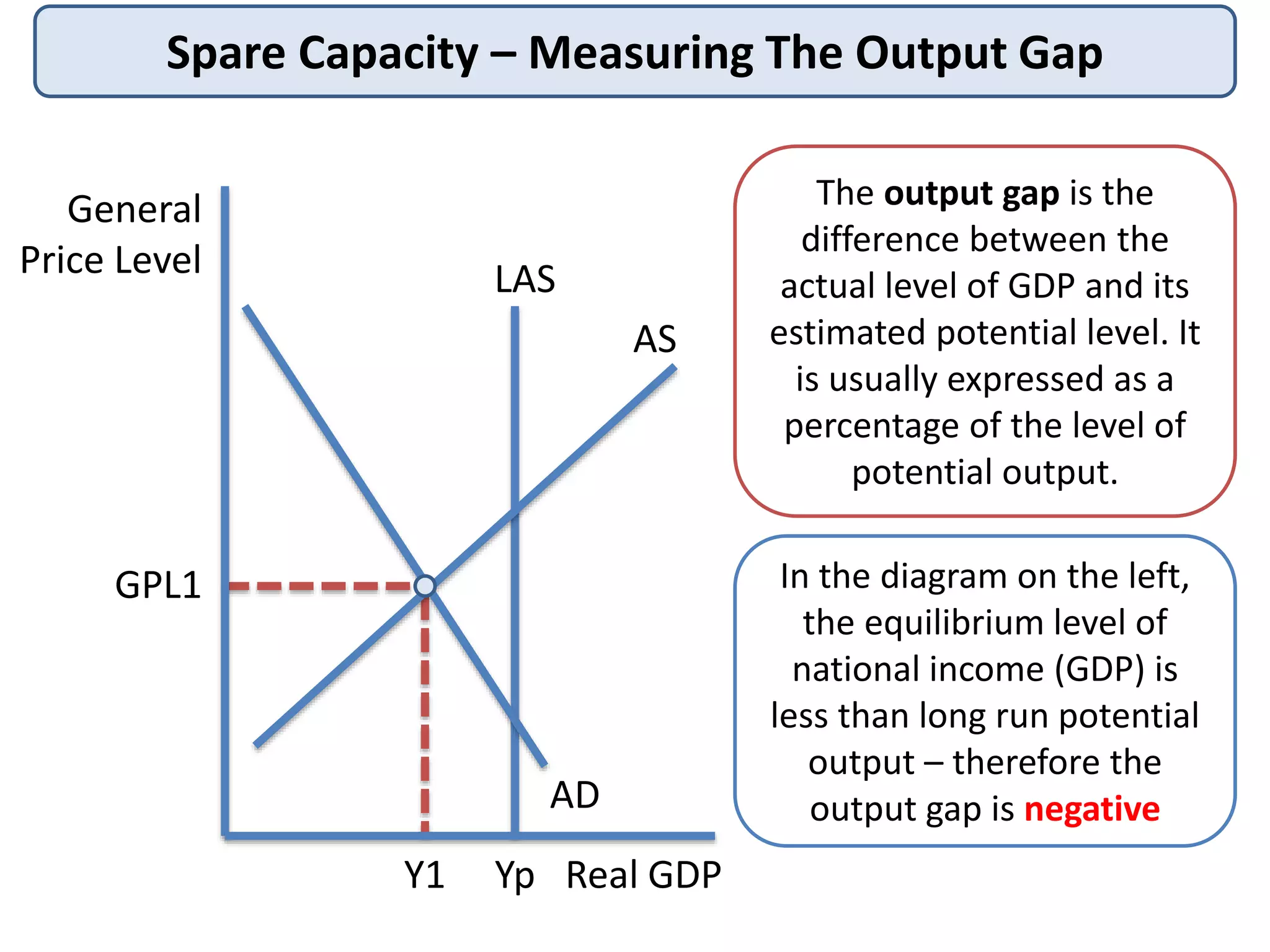

Spare Capacity –Measuring The Output Gap

The output gap is the

difference between the

actual level of GDP and its

estimated potential level. It

is usually expressed as a

percentage of the level of

potential output.

General

Price Level

Real GDP

GPL1

AS

Y1

AD

Yp

LAS

In the diagram on the left,

the equilibrium level of

national income (GDP) is

less than long run potential

output – therefore the

output gap is negative

10.

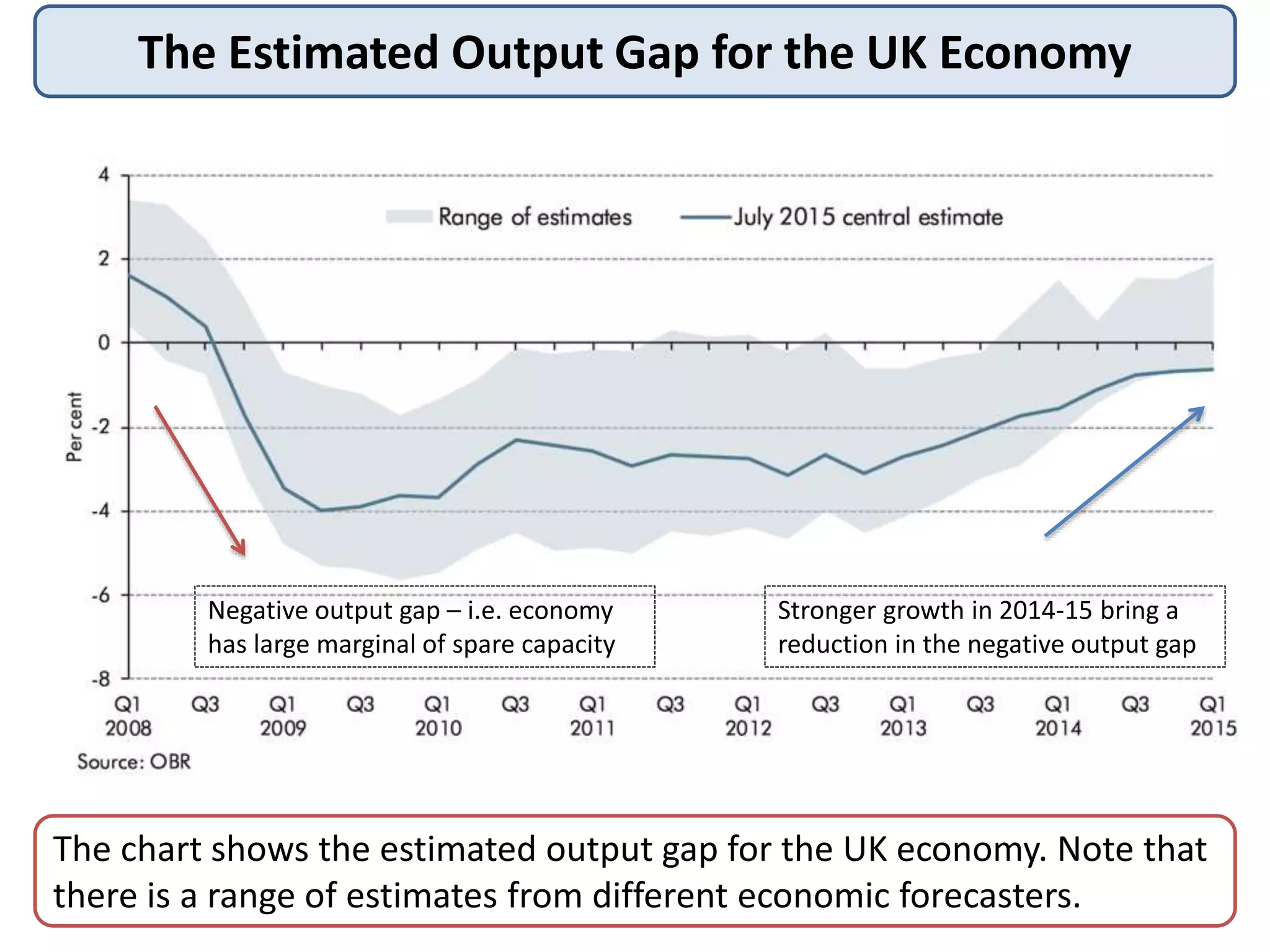

The Estimated OutputGap for the UK Economy

The chart shows the estimated output gap for the UK economy. Note that

there is a range of estimates from different economic forecasters.

Negative output gap – i.e. economy

has large marginal of spare capacity

Stronger growth in 2014-15 bring a

reduction in the negative output gap

11.

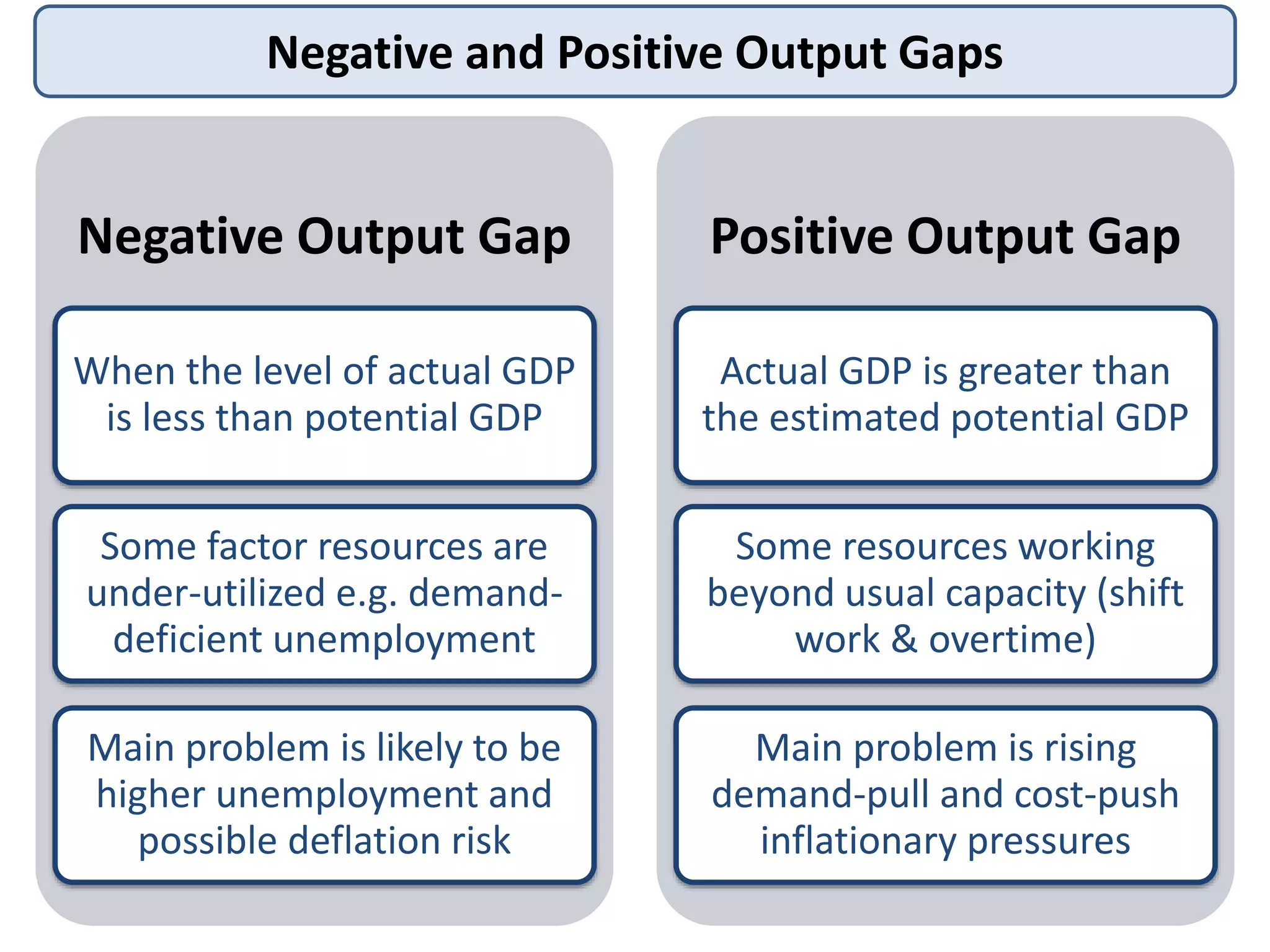

Negative and PositiveOutput Gaps

Negative Output Gap

When the level of actual GDP

is less than potential GDP

Some factor resources are

under-utilized e.g. demand-

deficient unemployment

Main problem is likely to be

higher unemployment and

possible deflation risk

Positive Output Gap

Actual GDP is greater than

the estimated potential GDP

Some resources working

beyond usual capacity (shift

work & overtime)

Main problem is rising

demand-pull and cost-push

inflationary pressures

12.

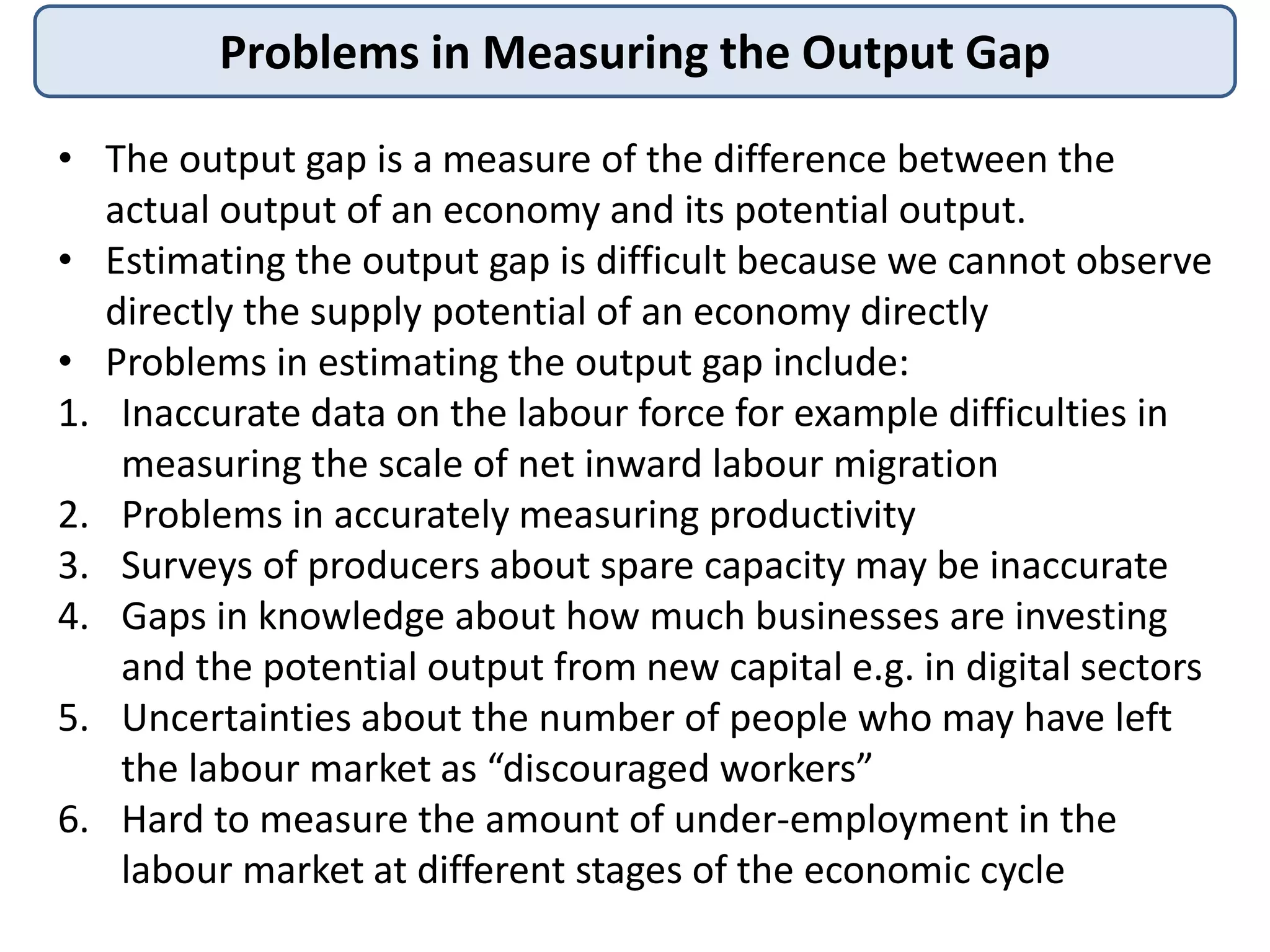

Problems in Measuringthe Output Gap

• The output gap is a measure of the difference between the

actual output of an economy and its potential output.

• Estimating the output gap is difficult because we cannot observe

directly the supply potential of an economy directly

• Problems in estimating the output gap include:

1. Inaccurate data on the labour force for example difficulties in

measuring the scale of net inward labour migration

2. Problems in accurately measuring productivity

3. Surveys of producers about spare capacity may be inaccurate

4. Gaps in knowledge about how much businesses are investing

and the potential output from new capital e.g. in digital sectors

5. Uncertainties about the number of people who may have left

the labour market as “discouraged workers”

6. Hard to measure the amount of under-employment in the

labour market at different stages of the economic cycle

13.

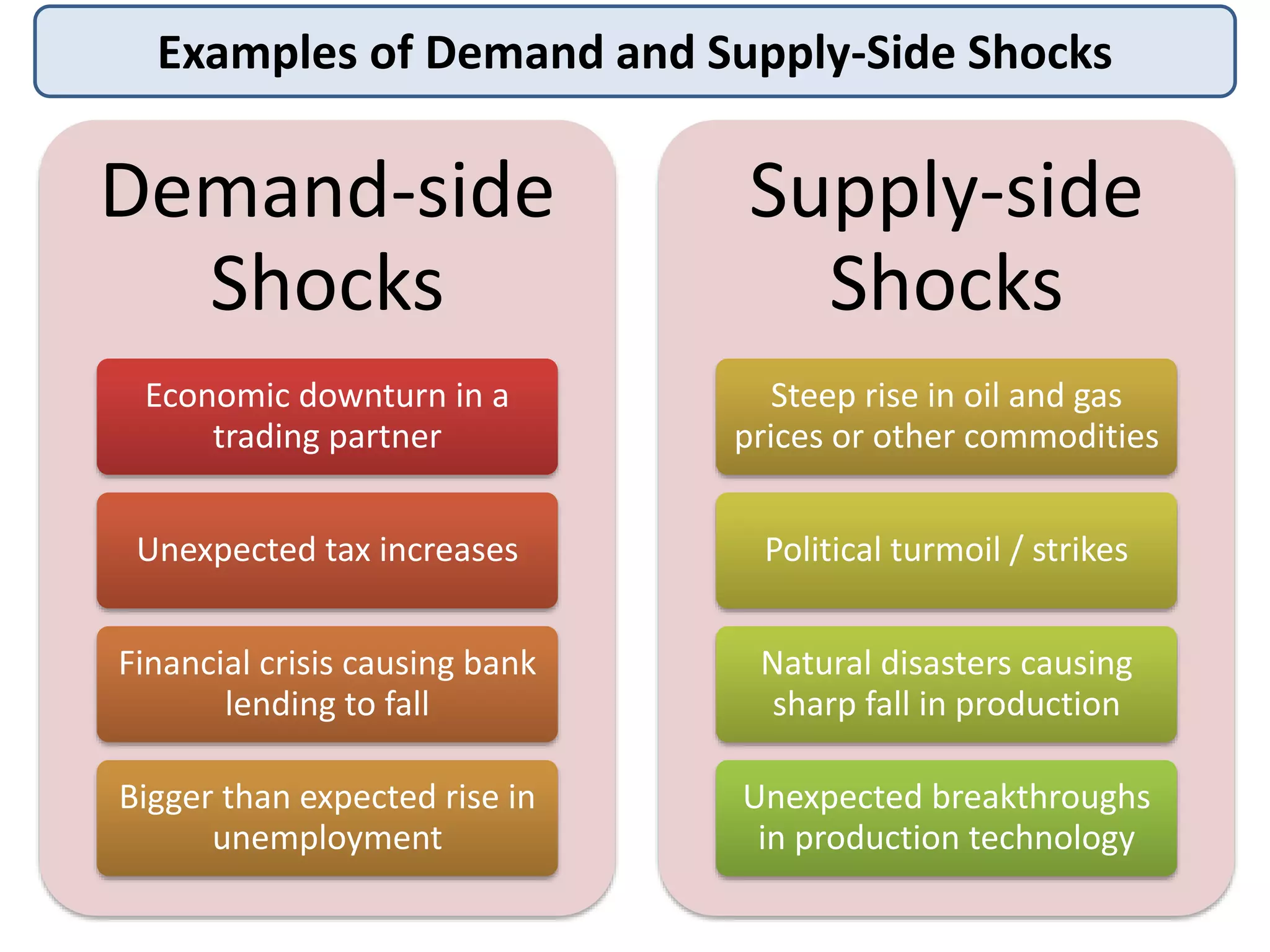

Examples of Demandand Supply-Side Shocks

Demand-side

Shocks

Economic downturn in a

trading partner

Unexpected tax increases

Financial crisis causing bank

lending to fall

Bigger than expected rise in

unemployment

Supply-side

Shocks

Steep rise in oil and gas

prices or other commodities

Political turmoil / strikes

Natural disasters causing

sharp fall in production

Unexpected breakthroughs

in production technology

14.

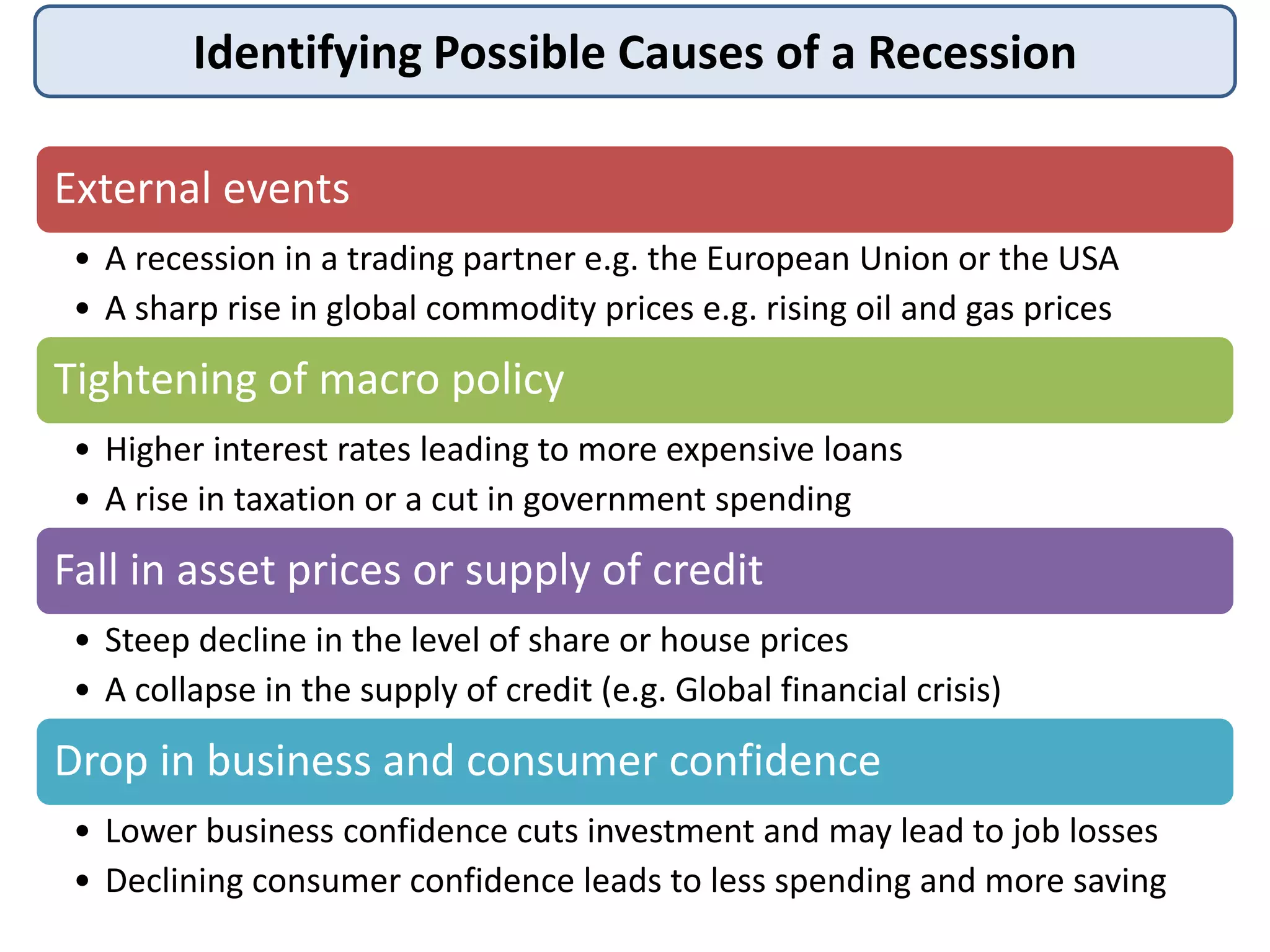

Identifying Possible Causesof a Recession

External events

• A recession in a trading partner e.g. the European Union or the USA

• A sharp rise in global commodity prices e.g. rising oil and gas prices

Tightening of macro policy

• Higher interest rates leading to more expensive loans

• A rise in taxation or a cut in government spending

Fall in asset prices or supply of credit

• Steep decline in the level of share or house prices

• A collapse in the supply of credit (e.g. Global financial crisis)

Drop in business and consumer confidence

• Lower business confidence cuts investment and may lead to job losses

• Declining consumer confidence leads to less spending and more saving

15.

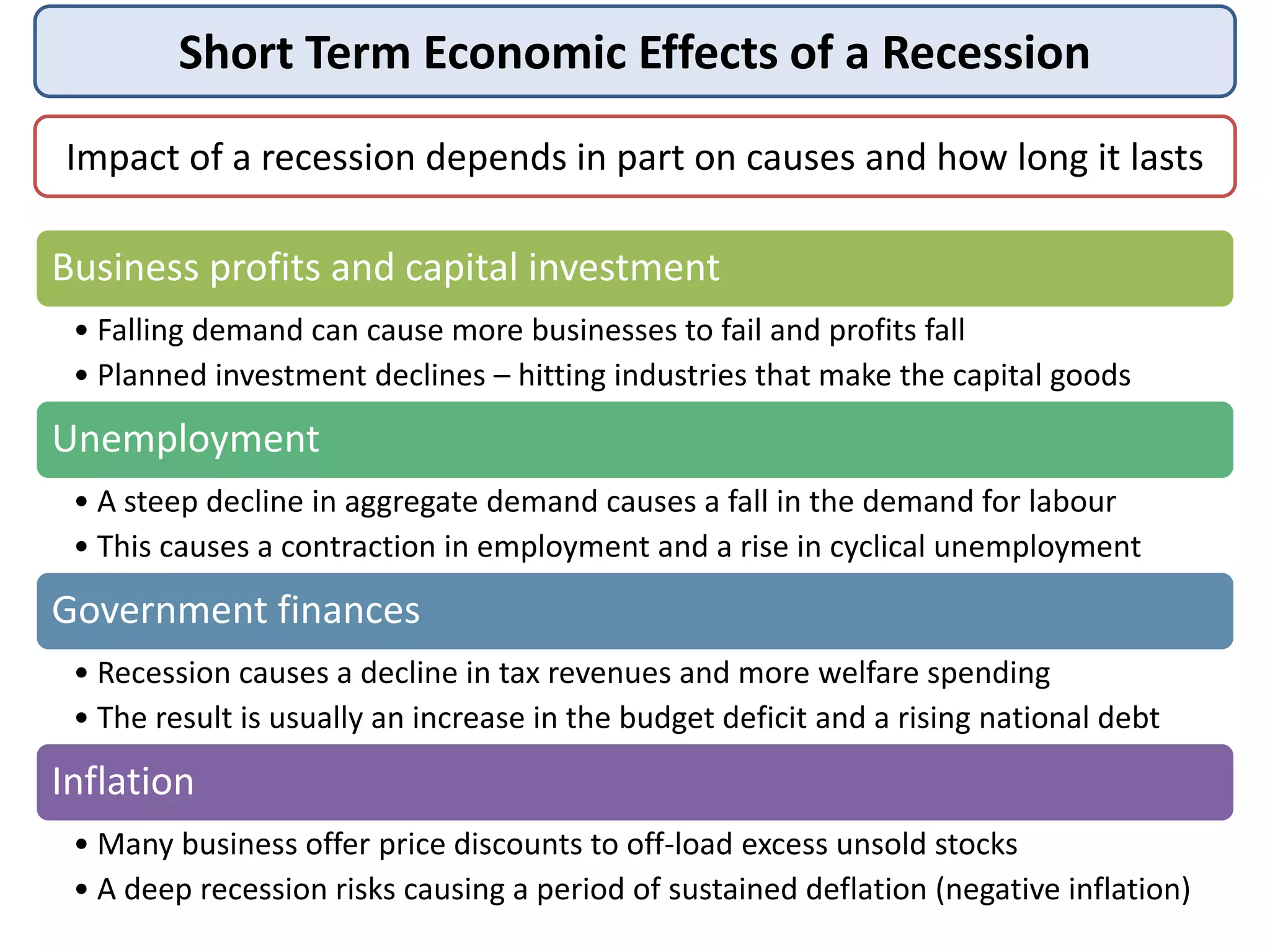

Short Term EconomicEffects of a Recession

Impact of a recession depends in part on causes and how long it lasts

Business profits and capital investment

• Falling demand can cause more businesses to fail and profits fall

• Planned investment declines – hitting industries that make the capital goods

Unemployment

• A steep decline in aggregate demand causes a fall in the demand for labour

• This causes a contraction in employment and a rise in cyclical unemployment

Government finances

• Recession causes a decline in tax revenues and more welfare spending

• The result is usually an increase in the budget deficit and a rising national debt

Inflation

• Many business offer price discounts to off-load excess unsold stocks

• A deep recession risks causing a period of sustained deflation (negative inflation)

16.

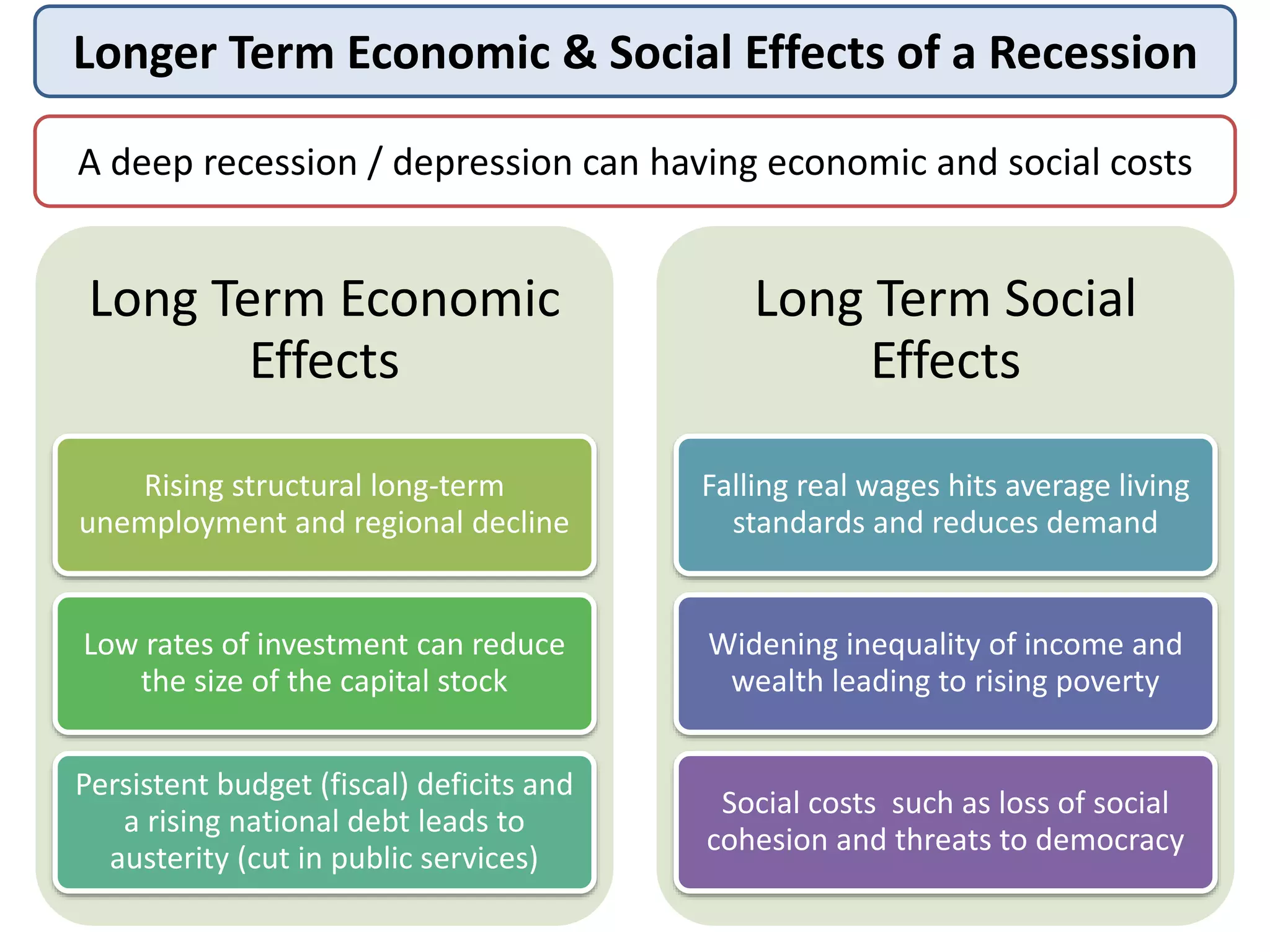

Longer Term Economic& Social Effects of a Recession

A deep recession / depression can having economic and social costs

Long Term Economic

Effects

Rising structural long-term

unemployment and regional decline

Low rates of investment can reduce

the size of the capital stock

Persistent budget (fiscal) deficits and

a rising national debt leads to

austerity (cut in public services)

Long Term Social

Effects

Falling real wages hits average living

standards and reduces demand

Widening inequality of income and

wealth leading to rising poverty

Social costs such as loss of social

cohesion and threats to democracy

17.

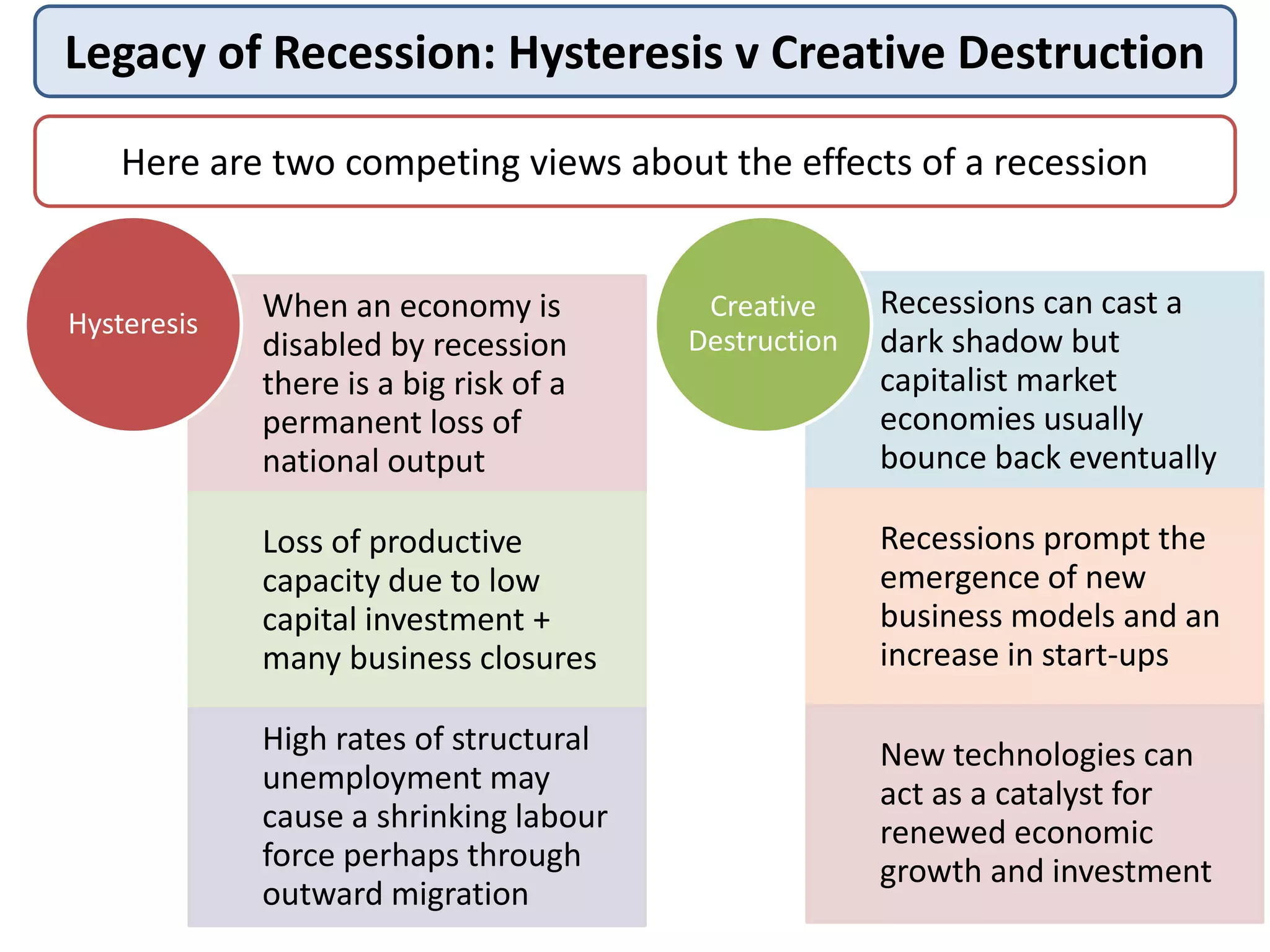

Legacy of Recession:Hysteresis v Creative Destruction

Here are two competing views about the effects of a recession

When an economy is

disabled by recession

there is a big risk of a

permanent loss of

national output

Loss of productive

capacity due to low

capital investment +

many business closures

High rates of structural

unemployment may

cause a shrinking labour

force perhaps through

outward migration

Hysteresis

Recessions can cast a

dark shadow but

capitalist market

economies usually

bounce back eventually

Recessions prompt the

emergence of new

business models and an

increase in start-ups

New technologies can

act as a catalyst for

renewed economic

growth and investment

Creative

Destruction

18.

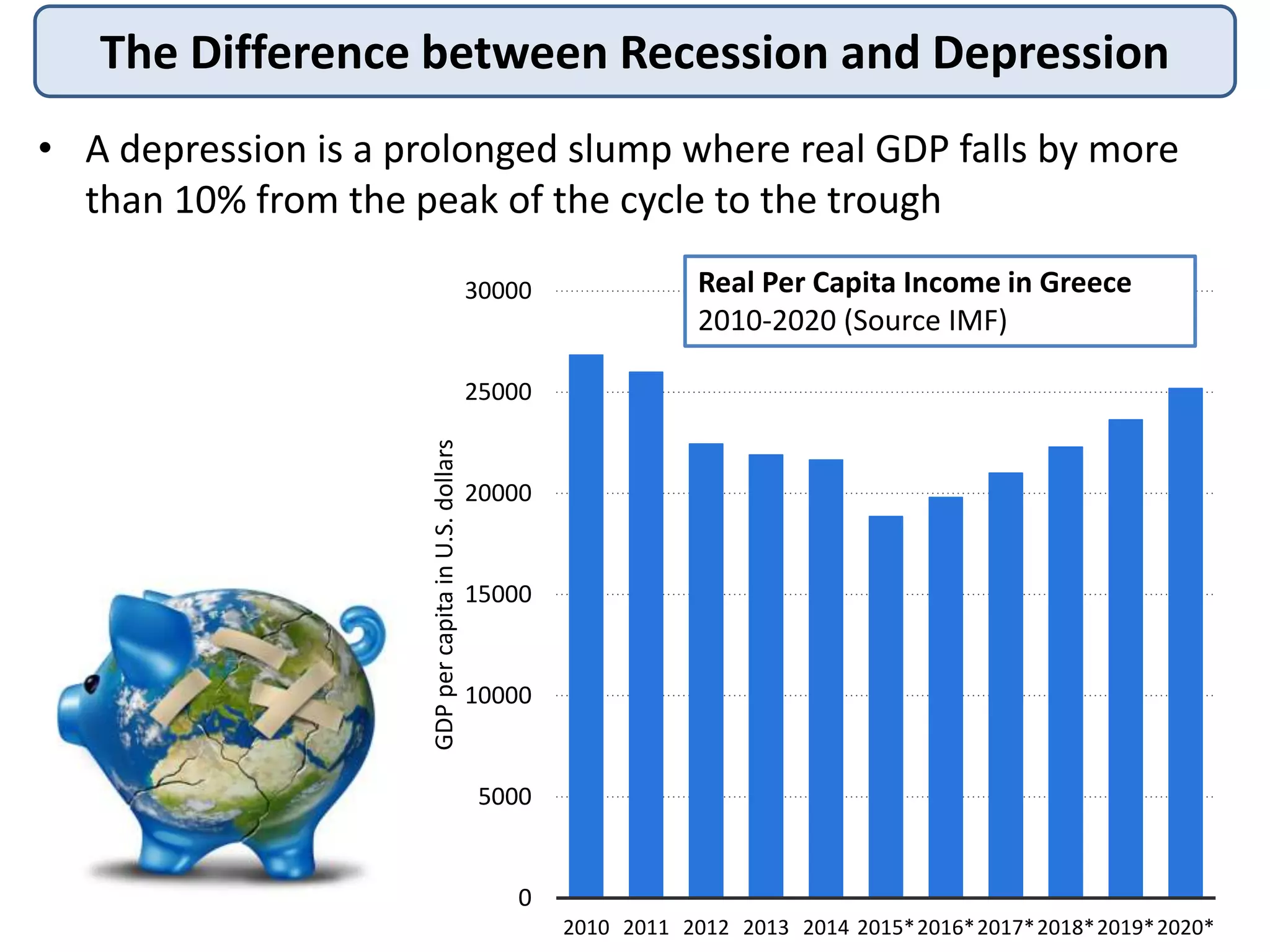

The Difference betweenRecession and Depression

• A depression is a prolonged slump where real GDP falls by more

than 10% from the peak of the cycle to the trough

0

5000

10000

15000

20000

25000

30000

2010 2011 2012 2013 2014 2015*2016*2017*2018*2019*2020*

GDPpercapitainU.S.dollars

Real Per Capita Income in Greece

2010-2020 (Source IMF)