Downloaded 448 times

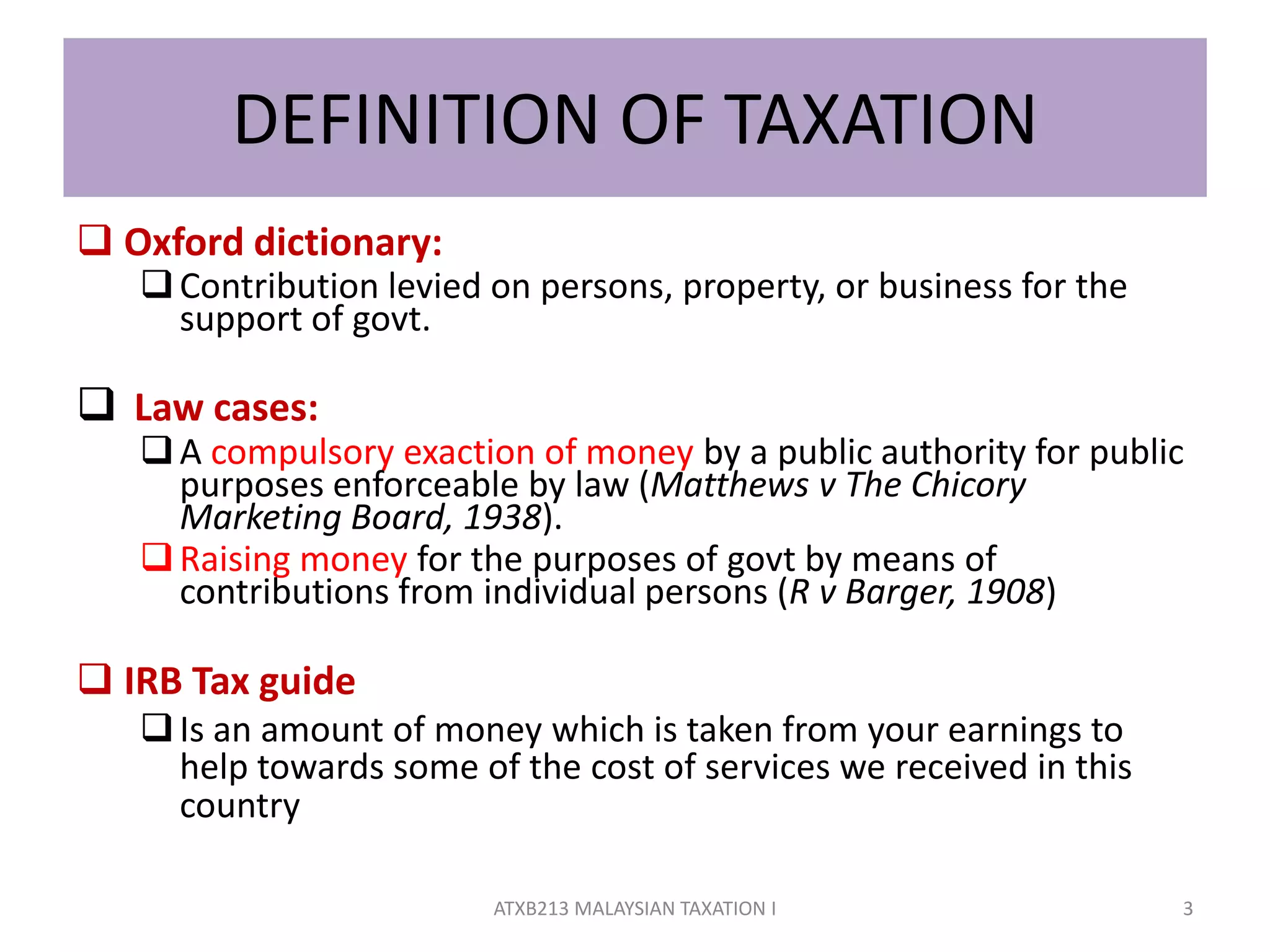

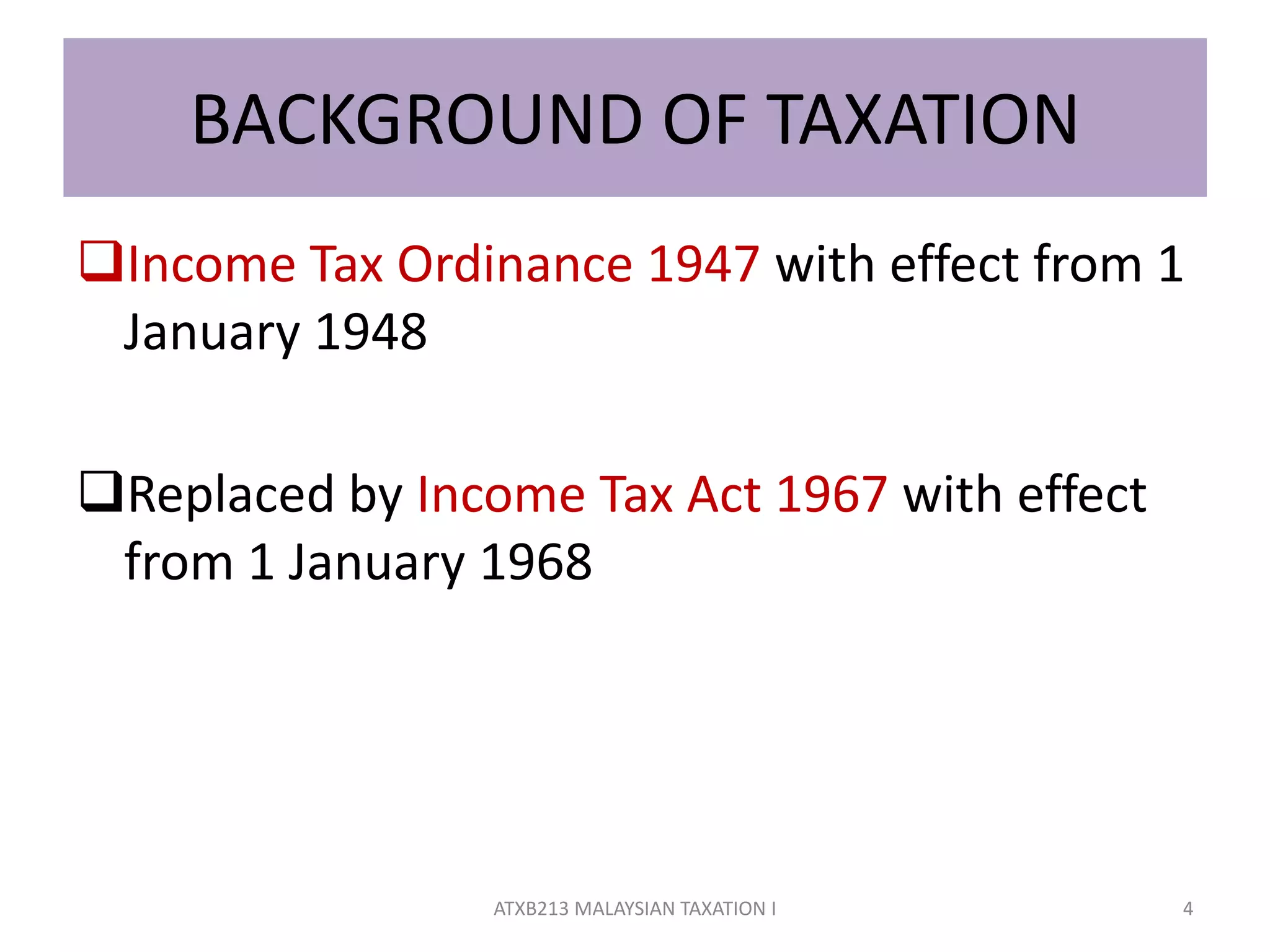

This document provides an introduction to Malaysian taxation. It defines taxation as a compulsory contribution levied by the government to support public services. The background of taxation in Malaysia began with the Income Tax Ordinance in 1947 and Income Tax Act in 1967. Taxation law comes from statutes, case law, and the Malaysian Inland Revenue Board. Taxes are either direct, paid directly by taxpayers, or indirect, collected by third parties. The document outlines the types and purposes of taxes in Malaysia and distinguishes between tax avoidance, which uses legal means to reduce taxes, versus tax evasion, which uses illegal means.