AGENDA FOR TODAY’SSESSION

Definition of Tax

Meaning of Tax

Objective of Tax

Difference between Tax and Duty

Charge and Fee

Classification Of Tax

Differences between Direct Tax and Indirect Tax

3.

AGENDA FOR TODAY’SSESSION

Tax on Income

Tax on Capital (Tax on land, land transfer, motor vehicle

Value Added Tax ( VAT )

Custom Duty, Excise Duty

Impact of Direct Tax and Indirect Tax on Economy

Canons of Taxation.

4.

DEFINITION OF TAX

Derived from Latin word “Taxare” meaning to estimate.

Prof. Seligman : “A compulsory contribution from person to the government to

defray the expenses incurred in the common interest of all without reference to

special benefit conferred”.

It is a type of levy or financial charge or fee imposed by government on legal

entities or individuals.

It is not voluntary payment or donation but and enforced contribution imposed

by the government.

5.

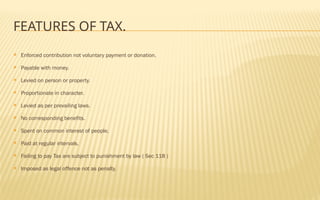

FEATURES OF TAX.

Enforced contribution not voluntary payment or donation.

Payable with money.

Levied on person or property.

Proportionate in character.

Levied as per prevailing laws.

No corresponding benefits.

Spent on common interest of people.

Paid at regular intervals.

Failing to pay Tax are subject to punishment by law ( Sec 118 )

Imposed as legal offence not as penalty.

6.

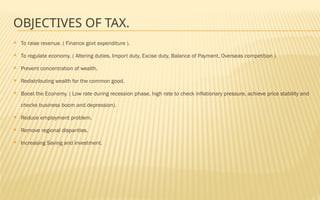

OBJECTIVES OF TAX.

To raise revenue. ( Finance govt expenditure ).

To regulate economy. ( Altering duties, Import duty, Excise duty, Balance of Payment, Overseas competition )

Prevent concentration of wealth.

Redistributing wealth for the common good.

Boost the Economy. ( Low rate during recession phase, high rate to check inflationary pressure, achieve price stability and

checks business boom and depression).

Reduce employment problem.

Remove regional disparities.

Increasing Saving and investment.

7.

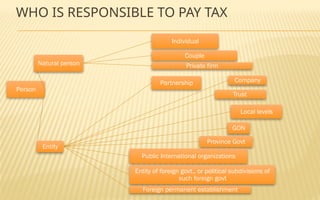

WHO IS RESPONSIBLETO PAY TAX

Person

Natural person

Individual

Couple

Private firm

Entity

Partnership

Trust

Company

Local levels

GON

Province Govt

Public International organizations

Entity of foreign govt., or political subdivisions of

such foreign govt

Foreign permanent establishment

8.

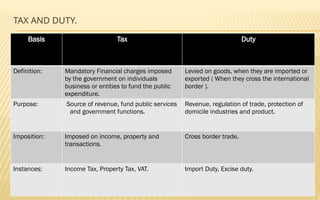

TAX AND DUTY.

BasisTax Duty

Definition: Mandatory Financial charges imposed

by the government on individuals

business or entities to fund the public

expenditure.

Levied on goods, when they are imported or

exported ( When they cross the international

border ).

Purpose: Source of revenue, fund public services

and government functions.

Revenue, regulation of trade, protection of

domicile industries and product.

Imposition: Imposed on income, property and

transactions.

Cross border trade.

Instances: Income Tax, Property Tax, VAT. Import Duty, Excise duty.

9.

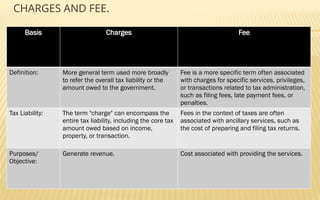

CHARGES AND FEE.

BasisCharges Fee

Definition: More general term used more broadly

to refer the overall tax liability or the

amount owed to the government.

Fee is a more specific term often associated

with charges for specific services, privileges,

or transactions related to tax administration,

such as filing fees, late payment fees, or

penalties.

Tax Liability: The term "charge" can encompass the

entire tax liability, including the core tax

amount owed based on income,

property, or transaction.

Fees in the context of taxes are often

associated with ancillary services, such as

the cost of preparing and filing tax returns.

Purposes/

Objective:

Generate revenue. Cost associated with providing the services.

10.

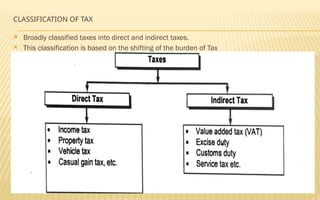

CLASSIFICATION OF TAX

Broadly classified taxes into direct and indirect taxes.

This classification is based on the shifting of the burden of Tax

11.

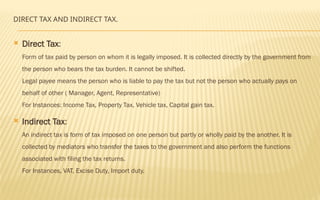

DIRECT TAX ANDINDIRECT TAX.

Direct Tax:

Form of tax paid by person on whom it is legally imposed. It is collected directly by the government from

the person who bears the tax burden. It cannot be shifted.

Legal payee means the person who is liable to pay the tax but not the person who actually pays on

behalf of other ( Manager, Agent, Representative)

For Instances: Income Tax, Property Tax, Vehicle tax, Capital gain tax.

Indirect Tax:

An indirect tax is form of tax imposed on one person but partly or wholly paid by the another. It is

collected by mediators who transfer the taxes to the government and also perform the functions

associated with filing the tax returns.

For Instances, VAT, Excise Duty, Import duty.

12.

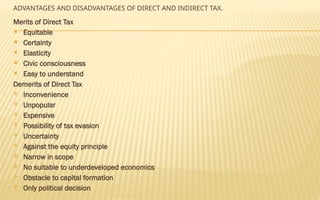

ADVANTAGES AND DISADVANTAGESOF DIRECT AND INDIRECT TAX.

Merits of Direct Tax

Equitable

Certainty

Elasticity

Civic consciousness

Easy to understand

Demerits of Direct Tax

Inconvenience

Unpopular

Expensive

Possibility of tax evasion

Uncertainty

Against the equity principle

Narrow in scope

No suitable to underdeveloped economics

Obstacle to capital formation

Only political decision

13.

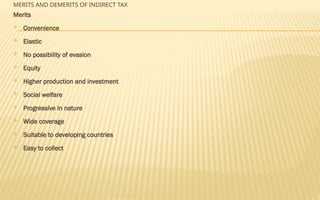

MERITS AND DEMERITSOF INDIRECT TAX

Merits

Convenience

Elastic

No possibility of evasion

Equity

Higher production and investment

Social welfare

Progressive in nature

Wide coverage

Suitable to developing countries

Easy to collect

14.

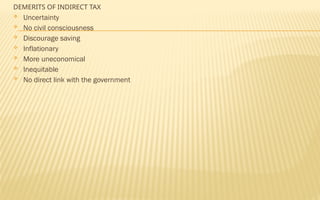

DEMERITS OF INDIRECTTAX

Uncertainty

No civil consciousness

Discourage saving

Inflationary

More uneconomical

Inequitable

No direct link with the government

15.

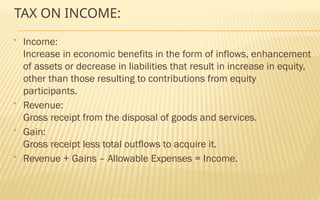

TAX ON INCOME:

Income:

Increase in economic benefits in the form of inflows, enhancement

of assets or decrease in liabilities that result in increase in equity,

other than those resulting to contributions from equity

participants.

Revenue:

Gross receipt from the disposal of goods and services.

Gain:

Gross receipt less total outflows to acquire it.

Revenue + Gains – Allowable Expenses = Income.

16.

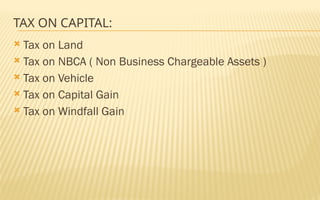

TAX ON CAPITAL:

Tax on Land

Tax on NBCA ( Non Business Chargeable Assets )

Tax on Vehicle

Tax on Capital Gain

Tax on Windfall Gain

17.

VALUE ADDED TAX( VAT )

It is Indirect Tax, improved and modified form of sales tax.

It is levied on value added of goods and services at each

stage in the process of production and distribution chain.

Although VAT is eventually borne by the final consumer, it

is collected at each stage of production and distribution

chain.

Types of VAT:

i. Consumption type

ii. Income Type

iii. Gross National Product type ( GNP ).

18.

CUSTOM DUTY, EXCISEDUTY.

Import duty/Custom duty is a tariff levied on goods

when they are brought into a country. It is a financial

charge imposed by the government on imported

products.

Import duties serve various purposes, including revenue

generation, protection of domestic industries, trade

regulation, and correction of trade imbalances.

Excise duty, also known as excise tax, is a type of indirect

tax imposed by the government on the production, sale,

or consumption of certain goods within the country.

Excise duties are often considered "sin taxes" because

they are frequently applied to goods that are deemed

19.

CANONS OF TAXATION.

Basic principles of taxation upon which a good tax system

is built.

Canon of Equality.

Canon of Certainty. ( Time , Method, Amount, Place )

Canon of Convenience.

Canon of Economy.

Canon of Productivity.

Canon of Elasticity.

Canon of Diversity

RELATION OF INCOMETAX WITH OTHER LAWS

A. Income tax Act and constitution ( Article 15 )

B. Income tax act and Finance Act

C. Income Tax Act and Income Tax rules

D. Income Tax Act and provisional Tax realization Act

E. Income Tax Act and Legal Precedents established by court