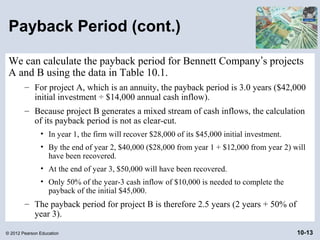

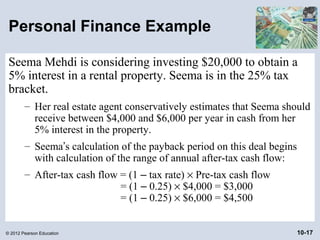

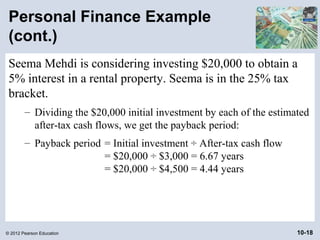

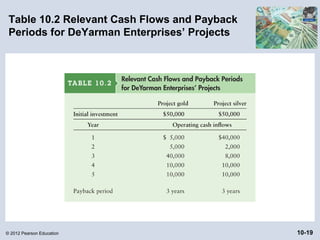

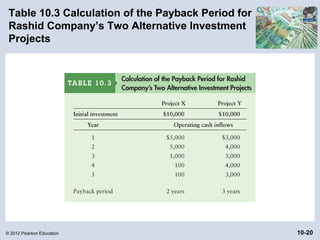

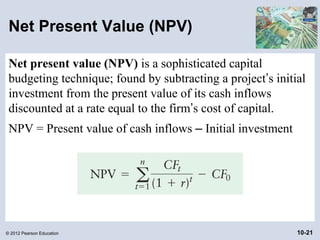

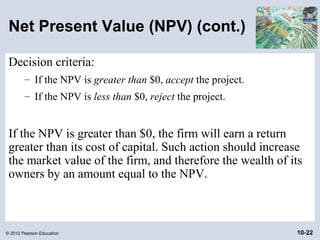

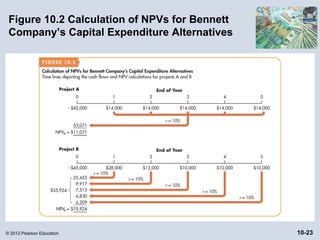

This chapter discusses capital budgeting techniques used to evaluate long-term investment projects. It covers the payback period method, which calculates the number of years to recover the initial investment of a project from its cash inflows. The chapter provides examples of calculating payback periods for projects and discusses the pros and cons of the payback method, noting it does not take the time value of money into account but is intuitive. It also introduces net present value and internal rate of return techniques.