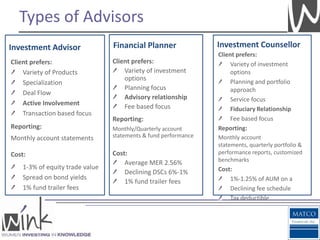

Assistant: Assistant: Paraplanner Paraplanner Portfolio Manager Regulation: Regulation: Regulation: IIROC FP Canada Portfolio Management Fee: Fee: Fee: Transaction based Hourly/Fixed/AUM AUM Focus: Focus: Focus: Products Planning Advisory Client: Client: Client: Mass Affluent Mass Affluent/HNW HNW Execution Strategies Lump Sum - All at once Dollar Cost Averaging - Regular intervals over time Value Averaging - Buys more shares