Downloaded 123 times

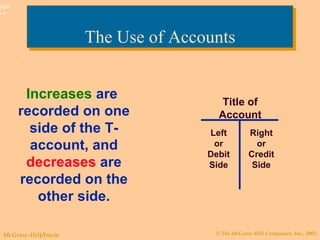

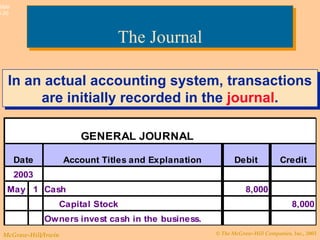

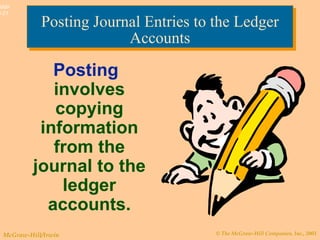

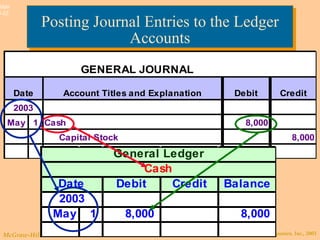

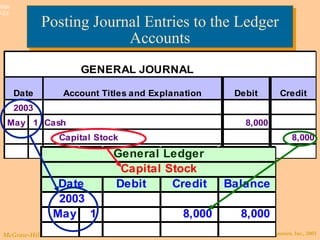

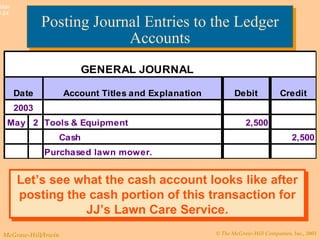

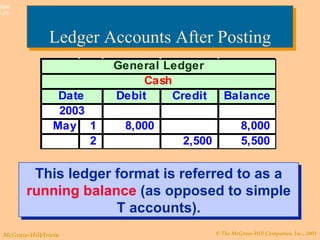

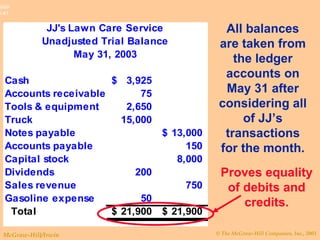

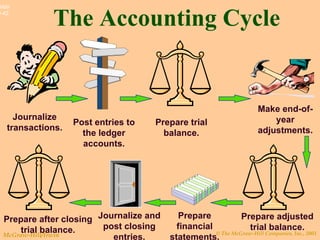

The document summarizes key aspects of the accounting cycle, including establishing and maintaining accounting records, using T-accounts and ledgers to track transactions, and applying debit and credit rules. It provides examples of journalizing and posting transactions for a sample business, including investments, expenses, revenues, and dividends. It explains the purpose of the trial balance in proving the equality of debits and credits.