Downloaded 79 times

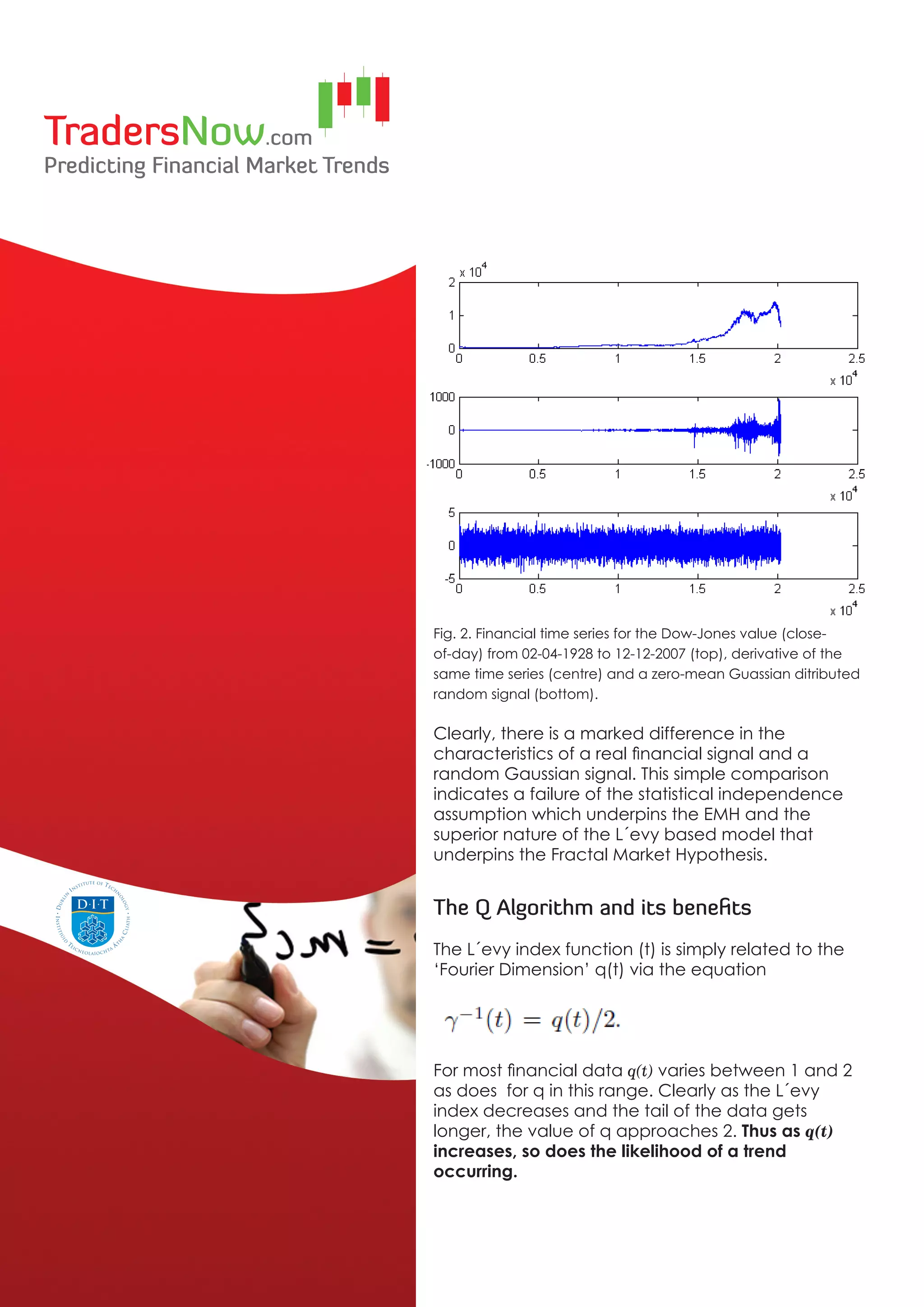

The document discusses the limitations of the Efficient Market Hypothesis (EMH) in explaining real financial market behavior, arguing for the Fractal Market Hypothesis (FMH) as a more accurate model. It highlights how actual market returns contradict the normal distribution predicted by EMH, exhibiting characteristics such as fat tails and leptokurtosis that suggest deeper underlying dynamics. The Q algorithm developed by TradersNow leverages the Levy index to forecast market trends by analyzing the behavior of financial time series data.

![[2 Session] TA controversis, Indicator, divergence, 9 rule for Divergence [29...](https://cdn.slidesharecdn.com/ss_thumbnails/4925acdd-c978-4683-b19c-f158d103b5f8-150325005159-conversion-gate01-thumbnail.jpg?width=640&height=640&fit=bounds)