BAIT 3

TMU 08212:ADVANCED BUSINESS

TAXATION

TOPIC ONE: VALUE ADDED TAX (VAT)

LECTURE II: IMPOSITION OF VAT IN TANZANIA AND ITS

REGISTRATION

Year 2023/2024

1

VALUE ADDED TAX (VAT) BY: NYANTAMBA

2.

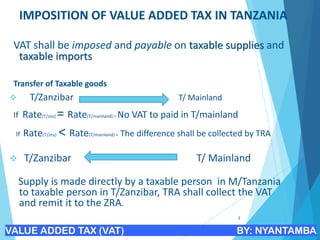

IMPOSITION OF VALUEADDED TAX IN TANZANIA

VAT shall be imposed and payable on taxable supplies and

taxable imports

Transfer of Taxable goods

❖ T/Zanzibar T/ Mainland

If Rate(T/znz) = Rate(T/mainland) = No VAT to paid in T/mainland

If Rate(T/znz) < Rate(T/mainland) = The difference shall be collected by TRA

❖ T/Zanzibar T/ Mainland

Supply is made directly by a taxable person in M/Tanzania

to taxable person in T/Zanzibar, TRA shall collect the VAT

and remit it to the ZRA.

2

VALUE ADDED TAX (VAT) BY: NYANTAMBA

3.

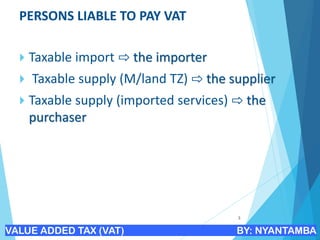

PERSONS LIABLE TOPAY VAT

Taxable import ⇨ the importer

Taxable supply (M/land TZ) ⇨ the supplier

Taxable supply (imported services) ⇨ the

purchaser

3

VALUE ADDED TAX (VAT) BY: NYANTAMBA

4.

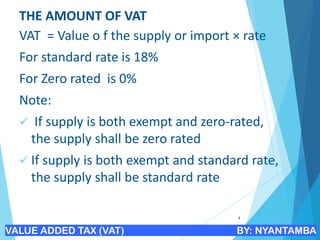

THE AMOUNT OFVAT

VAT = Value o f the supply or import × rate

For standard rate is 18%

For Zero rated is 0%

Note:

✓ If supply is both exempt and zero-rated,

the supply shall be zero rated

✓ If supply is both exempt and standard rate,

the supply shall be standard rate

4

VALUE ADDED TAX (VAT) BY: NYANTAMBA

5.

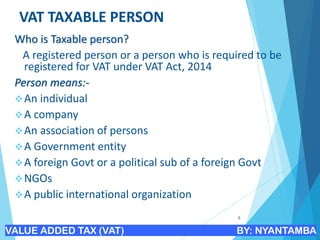

VAT TAXABLE PERSON

Whois Taxable person?

A registered person or a person who is required to be

registered for VAT under VAT Act, 2014

Person means:-

❖An individual

❖A company

❖An association of persons

❖A Government entity

❖A foreign Govt or a political sub of a foreign Govt

❖NGOs

❖A public international organization

5

VALUE ADDED TAX (VAT) BY: NYANTAMBA

6.

VAT -REGISTRATION

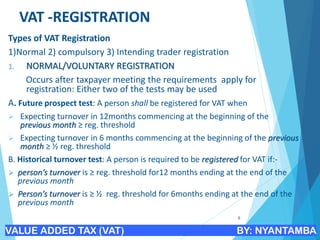

Types ofVAT Registration

1)Normal 2) compulsory 3) Intending trader registration

1. NORMAL/VOLUNTARY REGISTRATION

Occurs after taxpayer meeting the requirements apply for

registration: Either two of the tests may be used

A. Future prospect test: A person shall be registered for VAT when

➢ Expecting turnover in 12months commencing at the beginning of the

previous month ≥ reg. threshold

➢ Expecting turnover in 6 months commencing at the beginning of the previous

month ≥ ½ reg. threshold

B. Historical turnover test: A person is required to be registered for VAT if:-

➢ person’s turnover is ≥ reg. threshold for12 months ending at the end of the

previous month

➢ Person’s turnover is ≥ ½ reg. threshold for 6months ending at the end of the

previous month

6

VALUE ADDED TAX (VAT) BY: NYANTAMBA

7.

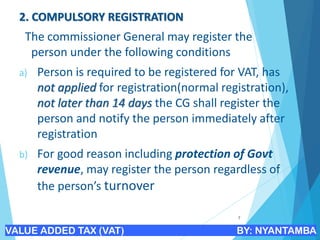

2. COMPULSORY REGISTRATION

Thecommissioner General may register the

person under the following conditions

a) Person is required to be registered for VAT, has

not applied for registration(normal registration),

not later than 14 days the CG shall register the

person and notify the person immediately after

registration

b) For good reason including protection of Govt

revenue, may register the person regardless of

the person’s turnover

7

VALUE ADDED TAX (VAT) BY: NYANTAMBA

8.

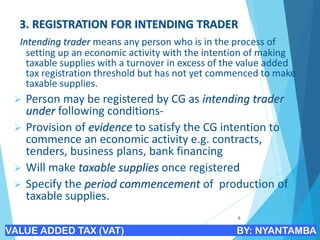

3. REGISTRATION FORINTENDING TRADER

Intending trader means any person who is in the process of

setting up an economic activity with the intention of making

taxable supplies with a turnover in excess of the value added

tax registration threshold but has not yet commenced to make

taxable supplies.

➢ Person may be registered by CG as intending trader

under following conditions-

➢ Provision of evidence to satisfy the CG intention to

commence an economic activity e.g. contracts,

tenders, business plans, bank financing

➢ Will make taxable supplies once registered

➢ Specify the period commencement of production of

taxable supplies.

8

VALUE ADDED TAX (VAT) BY: NYANTAMBA

9.

Registrations Of BranchesAnd Divisions

➢ Businesses with more than one set of premises

(branches) or autonomous units within same

legal entity shall be a single registration,

➢ Shall cover all economic activities undertaken

by that person’s branches divisions.

➢ All returns are amalgamated for completion of

a single VAT return

9

VALUE ADDED TAX (VAT) BY: NYANTAMBA

10.

Person’s Turnover

A person’sturnover is sum of :

➢ Total value of supplies made, or to be made, by the

person and

➢ Total value of supplies of imported services made, or to

be made, to the person during the period that would be

taxable supplies if the person was a taxable person

during that period.

Note

A person’s turnover in respect of supplies of imported

services shall be considered for registration where that

person has a turnover resulting from taxable supplies

other than supplies of imported services (Regu. 10(2))

10

VALUE ADDED TAX (VAT) BY: NYANTAMBA

11.

Example

Nchimunya started runninga retail business making standard

rated taxable supplies on 1 June 2022. She made sales of Tshs

6,000,000 in the month of June. Her sales increased by Tshs

21,000,000 each month from July 2022 to November 2022. From

December 2022, she expects sales to be Tshs 17,000,000 per

month. Her standard rated expenses were Tshs 35,000,000 per

month and are expected to remain at this level in future.

Nchimunya is not sure whether she is required to register her

business for Value Added Tax.

a) Explain the Value Added Tax registration requirements to

Nchimunya

b) State, giving reasons, when Nchimunya will be required to

register for VAT

c) Explain three (3) obligations Nchimunya will have once she

registers her business for VAT

11

12.

Exclusion on Person’sTurnover

➢The value that would not be a taxable

if the person were a taxable person

➢The value of a sale of a capital asset

➢The value as a consequence of selling

an economic activity or part of it.

➢The value as a consequence of

permanently ceasing to carry on an

economic activity

12

VALUE ADDED TAX (VAT) BY: NYANTAMBA

13.

Exception on RegistrationThreshold

A person shall be required to be registered for VAT

if

➢The person supplying of professional services in

Mainland TZ and supplies of professional

services in M/TZ made by a person who is

permitted, approved, licensed, or belongs to a

professional association

➢A Govt entity or institution which carries on

economic activity

13

VALUE ADDED TAX (VAT) BY: NYANTAMBA

14.

TIME OF APPLICATIONSFOR REGISTRATION

➢Apply to CG within 30 days from the date of

such requirement

➢Once satisfied that an applicant qualifies,CG

shall register such person

➢Notify the applicant within 14 days of the

application

14

VALUE ADDED TAX (VAT) BY: NYANTAMBA

15.

NOTE

➢CG shall issuea registration certificate

to the registered person

➢A registered person shall use Taxpayer

Identification Number(TIN) and a Value

Added Tax Registration Number(VRN)

on all documents required to be issued

under VAT Act.

15

VALUE ADDED TAX (VAT) BY: NYANTAMBA

16.

VAT REGISTRATION THRESHOLD

➢Thelevel at which registration for the VAT becomes

compulsory is called VAT registration threshold.

➢now TSHS 200,000,000.

Important?

Yes! determines the efficiency operation of the VAT.

⇨Low threshold level includes many firms as taxable

persons which may exceeds tax authority

administration capacity

⇨ High threshold eliminates many small firms from

being included in the VAT population but it is

manageable

16

VALUE ADDED TAX (VAT) BY: NYANTAMBA

17.

CONSEQUENCES/EFFECTS OF VATREGISTRATION

➢ Person becomes a taxable person

➢ Enjoying benefits but with

responsibilities

⇨Ability of deducting input taxes incurred

when buying taxable goods and services

⇨ Becomes agent of TRA on collecting

taxes on all taxable goods and services

made by him.

17

VALUE ADDED TAX (VAT) BY: NYANTAMBA

18.

Issuing electronic fiscalreceipts(Tax invoice)

➢ Taxable person are supposed to issue

electronic fiscal receipts(EFR).

➢ EFR acknowledge both VAT received or

payable and the debts or cash received

from taxable transactions WHILE normal

receipts acknowledge receipt of cash or

debts

➢ Price advertised or quoted shall be VAT

inclusive

18

VALUE ADDED TAX (VAT) BY: NYANTAMBA

19.

TAX INVOICE

➢ Aregistered person who makes a

taxable supply shall, no later than the

day on which VAT becomes payable on

the supply

➢ Issue a serially numbered true and

correct tax invoice generated by EFD for

the supply.

19

VALUE ADDED TAX (VAT) BY: NYANTAMBA

20.

CONTENTS OF TAXINVOICE

➢ Date on which it is issued

➢ The name, TIN and VRN of the supplier

➢ The description & quantity

➢ The total consideration and the amount of VAT

➢ If the value of the supply exceeds the minimum amount

prescribed in the regulations, the name, address, TIN

and VRN of the customer

➢ Any other additional information as may be prescribed

in the regulations

➢ Original tax invoice shall be issued for each taxable

supply 20

VALUE ADDED TAX (VAT) BY: NYANTAMBA

21.

CREDIT NOTE

➢ Itis a commercial document issued by a seller to

a buyer

➢ Taxable person who had issued EFR in respect of

taxable supply must issue a credit note when:-

a) The supply is cancelled

b) The goods are returned to the registered taxable

person

c) The value of the supply is reduced

Credit note must include all features of EFR, the

amount of credit and a statement of the reason for

credit

21

VALUE ADDED TAX (VAT) BY: NYANTAMBA

22.

KEEPING RECORDS

Registered personshould keep the following records:

Value of each supply excluding VAT and the VAT

charged

Total VAT recorded for each accounting period

Payment made or received showing the date,

amount and the person making or receiving the

payment.

All goods appropriate or taken into person use or into

the use of other, the date of appropriation or taking

into use, the description of the goods, the value of

goods excluding VAT calculated on the goods.

22

VALUE ADDED TAX (VAT) BY: NYANTAMBA

23.

RECORDS…

➢ Copies ofall VAT electronic fiscal receipts

issued.

➢ A record of all outputs that is sales day

book

➢ Evidence supporting claims for the

recovery of input VAT that electronic fiscal

receipts.

➢ A record of all input, eg purchase day book

➢ VAT account

23

VALUE ADDED TAX (VAT) BY: NYANTAMBA

24.

A CANCELLATION OFREGISTRATION

A registered person may apply for cancellation if:-

a) Permanently ceased to make taxable supplies

b) Fails to maintain the registration threshold

Application shall be made within 14 days

CG may cancel registration of the person if:-

a) Registered by providing false or misleading

information

b) Not carrying on an economic activity

c) Ceases to produce taxable supplies

d) Taxable turnover falls below registration threshhod

24

VALUE ADDED TAX (VAT) BY: NYANTAMBA

25.

EFFECTS OF CANCELLATION

Aperson whose registration is cancelled shall

a) Shall cease to be registered person

b) Shall cease to use and issue Tax invoice

c) Shall surrender VAT registration certificate

d) Within 30 days file the final VAT return

and pay all taxes under this Act

NOTE: CG shall maintain list of all registered

including their history and make available

when required

25

VALUE ADDED TAX (VAT) BY: NYANTAMBA

26.

Example One

Tinashana Ltdis the owner of a new company dealing

with selling of mixed supplies in Arusha town. The

business started two years ago. She needs to know some

issues on tax compliance especially on Value Added Tax

(VAT).

Required:

Assist her on the following areas of issues:

(i) How does one become VAT taxable traders? (ii) Briefly

explain how one can stop to be taxable trader. (CPA (T))

VALUE ADDED TAX (VAT) BY: NYANTAMBA

27.

Example Two

The traderin some circumstances or conditions is

required to be registered for VAT and again may apply

for cancellation. The Commissioner in some

circumstance has powers to deregister a trader.

Required:

Explain at least four (4) reasons where Commissioner

may be required to do so. CPA (T)

27

VALUE ADDED TAX (VAT) BY: NYANTAMBA

28.

Review questions

Question 1

a)Explain the types of registration for the purposes of Value

Added Tax (VAT)

b) List any Six (6) contents which must appear on the tax

invoice

c) Describe three (4) circumstances which may result in a

business being de-registered for VAT

d) It has sometimes been suggested that the current TZS 100

million turnover thresholds for VAT registration and the

18% VAT single rate should be reduced to TZS 50 million

and 15% respectively. What is the basis or justification for

the above suggestion?

28

VALUE ADDED TAX (VAT) BY: NYANTAMBA