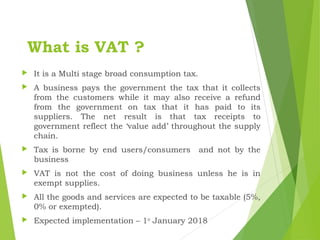

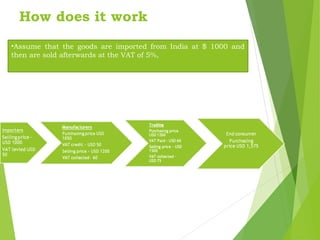

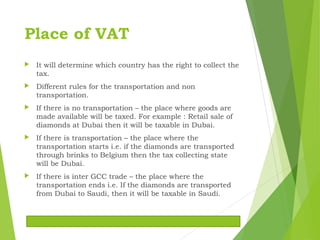

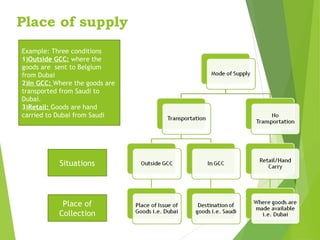

The UAE is implementing a VAT system beginning January 1, 2018, requiring companies with annual revenues over DH 3.75 million to register. VAT is a multi-stage consumption tax, where tax is paid by consumers, and businesses can reclaim tax on inputs, while exempt and zero-rated supplies exist. Registration, compliance, and reporting requirements are outlined, along with details on tax collection based on goods' transportation and supply locations.