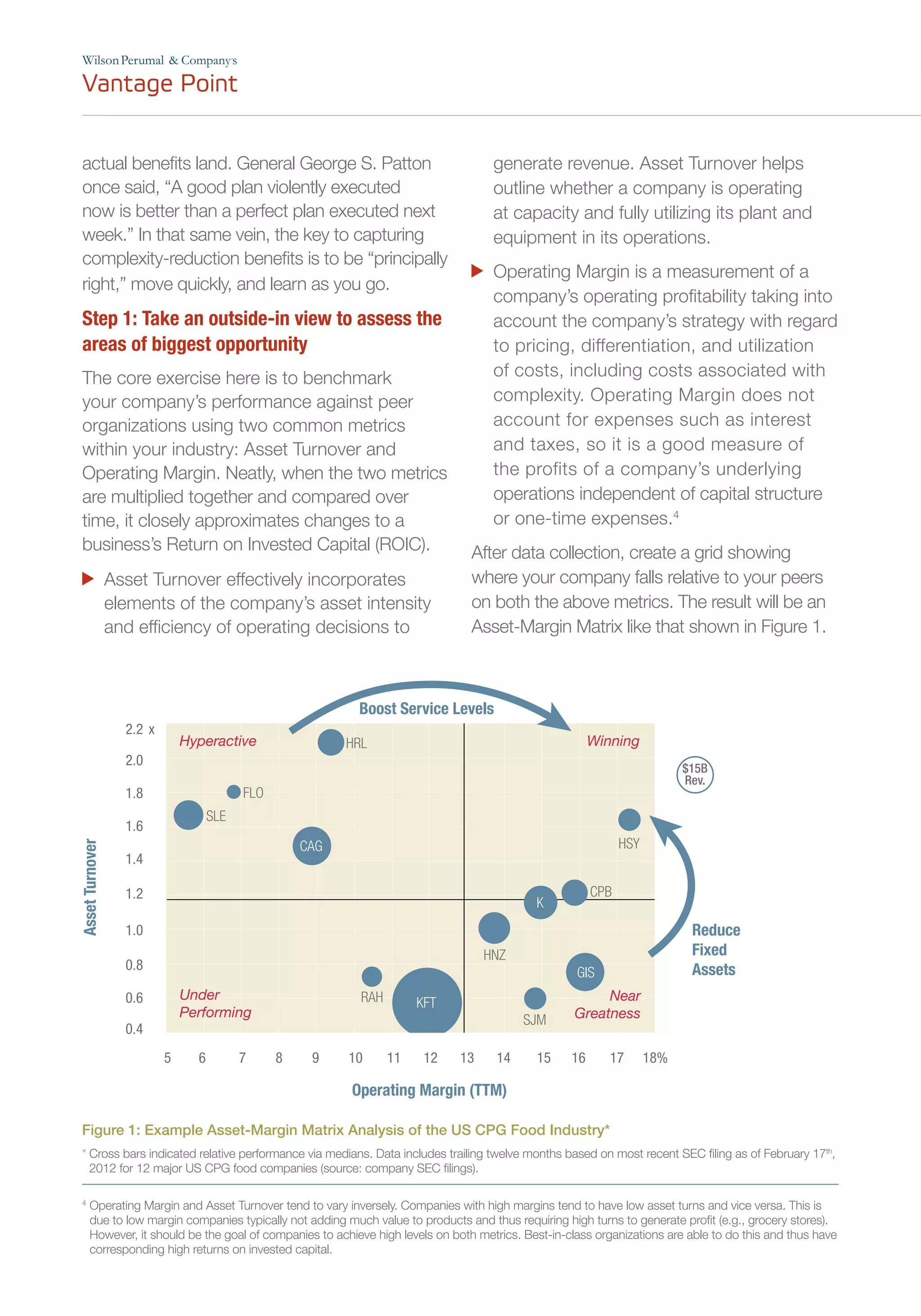

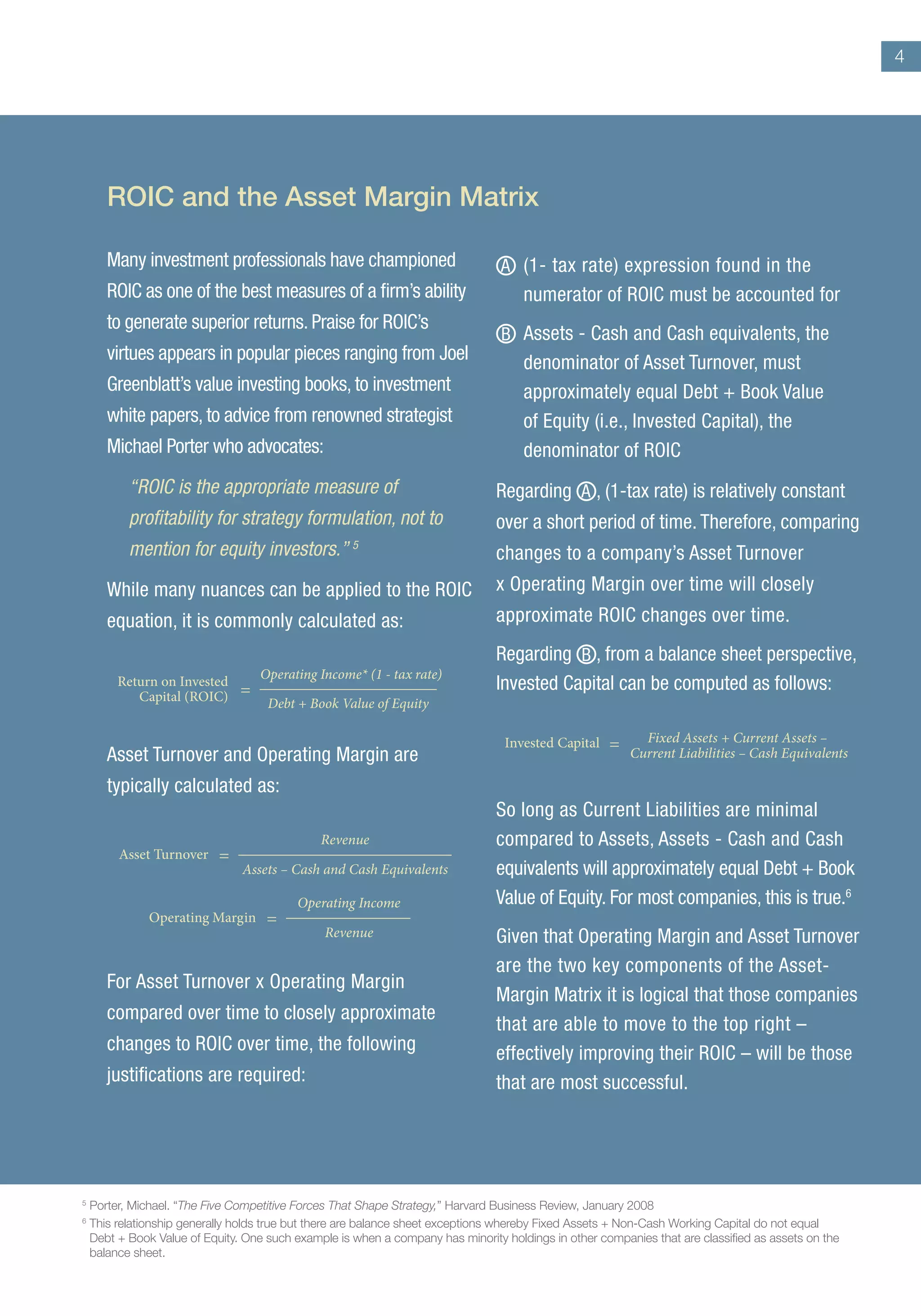

Download to read offline

Companies often struggle to fully realize the benefits of reducing complexity in their operations. This document discusses how companies can plan from the start to capture these benefits. It recommends explicitly considering benefit capture as part of complexity reduction efforts. Companies should identify which benefits, such as reducing costs or improving customer service, will provide the greatest value. They should also understand what changes are needed internally to achieve these benefits. With a clear plan to convert reduced complexity into financial gains, companies can better ensure the benefits of their efforts materialize.

![[Whitepaper] The “Theory of Constraints:” What’s Limiting Your Organization?](https://cdn.slidesharecdn.com/ss_thumbnails/theoryof-210212191639-thumbnail.jpg?width=640&height=640&fit=bounds)