Download to read offline

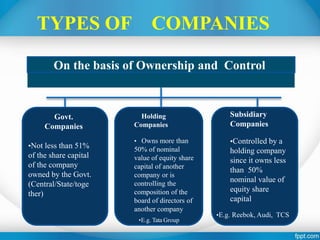

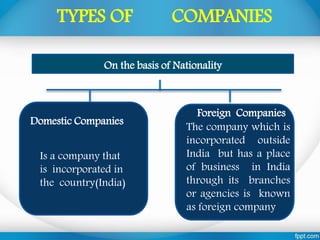

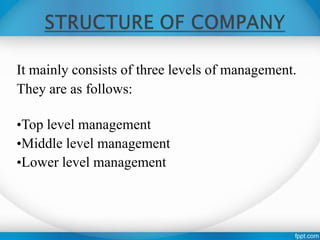

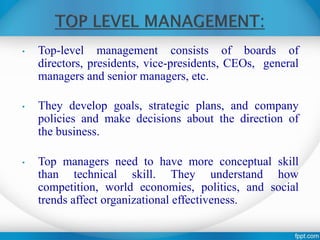

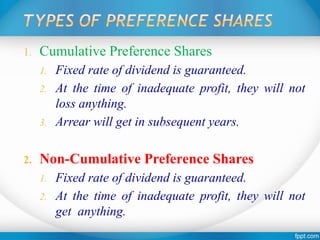

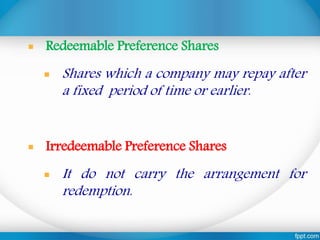

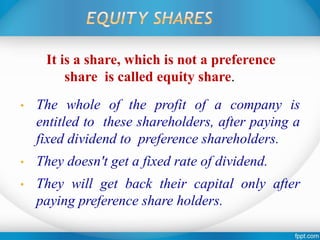

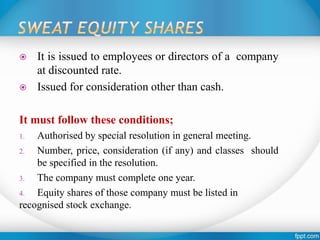

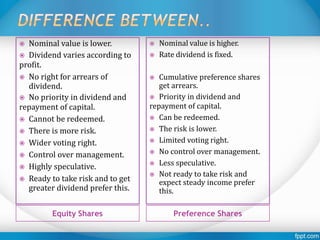

This document provides information about company accounts and types of companies. It begins with definitions of a company and its key characteristics such as separate legal entity, perpetual succession, and limited liability. It then discusses various types of companies based on incorporation (chartered, statutory, registered), liability (limited by shares, unlimited), number of members (private, public), ownership and control (government, holding, subsidiary), and nationality (domestic, foreign). The document also describes the three levels of management in a company and different types of shares such as preference shares, equity shares, employee stock options, and their key characteristics.