Downloaded 11 times

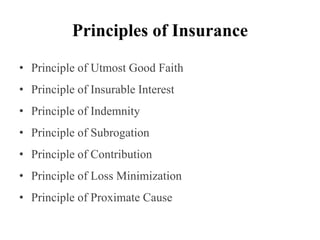

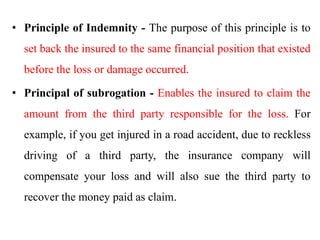

Non-banking financial services include insurance. There are two main types of insurance - life insurance and general insurance. Life insurance provides coverage for death and can include term life, whole life, endowment, and unit-linked plans. General insurance covers property and casualty risks like motor, health, home, and marine insurance. Insurance policies are regulated in India by IRDA and follow principles like utmost good faith, indemnity, and subrogation.