The document provides an overview of various topics related to insurance. It discusses the introduction and history of insurance in India. It then explains key concepts like the importance of insurance, terms used, the concept of assurance, reinsurance and various principles of insurance like utmost good faith. The document also discusses major players in the Indian insurance sector like LIC and GIC. It provides details about various types of insurance policies including life, health, fire, marine and vehicle insurance.

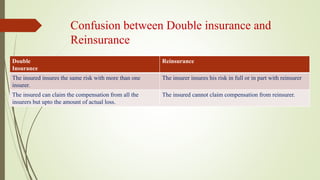

![LIC (Life insurance

Corporation)

Life Insurance Corporation of India (LIC) is an Indian state-owned insurance

group and investment company headquartered in Mumbai.

It is the largest insurance company in India with an estimated asset value of ₹1,560,482

crore (US$240 billion).[3] As of 2013 it had total life fund of Rs.1433103.14 crore with total

value of policies sold of 367.82 lakh that year.

The Life Insurance Corporation of India was founded in 1956 when the Parliament of

India passed the Life Insurance of India Act that nationalised the private insurance industry in

India. Over 245 insurance companies and provident societies were merged to create the state

owned Life Insurance Corporation.](https://image.slidesharecdn.com/insurance-180326141034/85/Insurance-22-320.jpg)