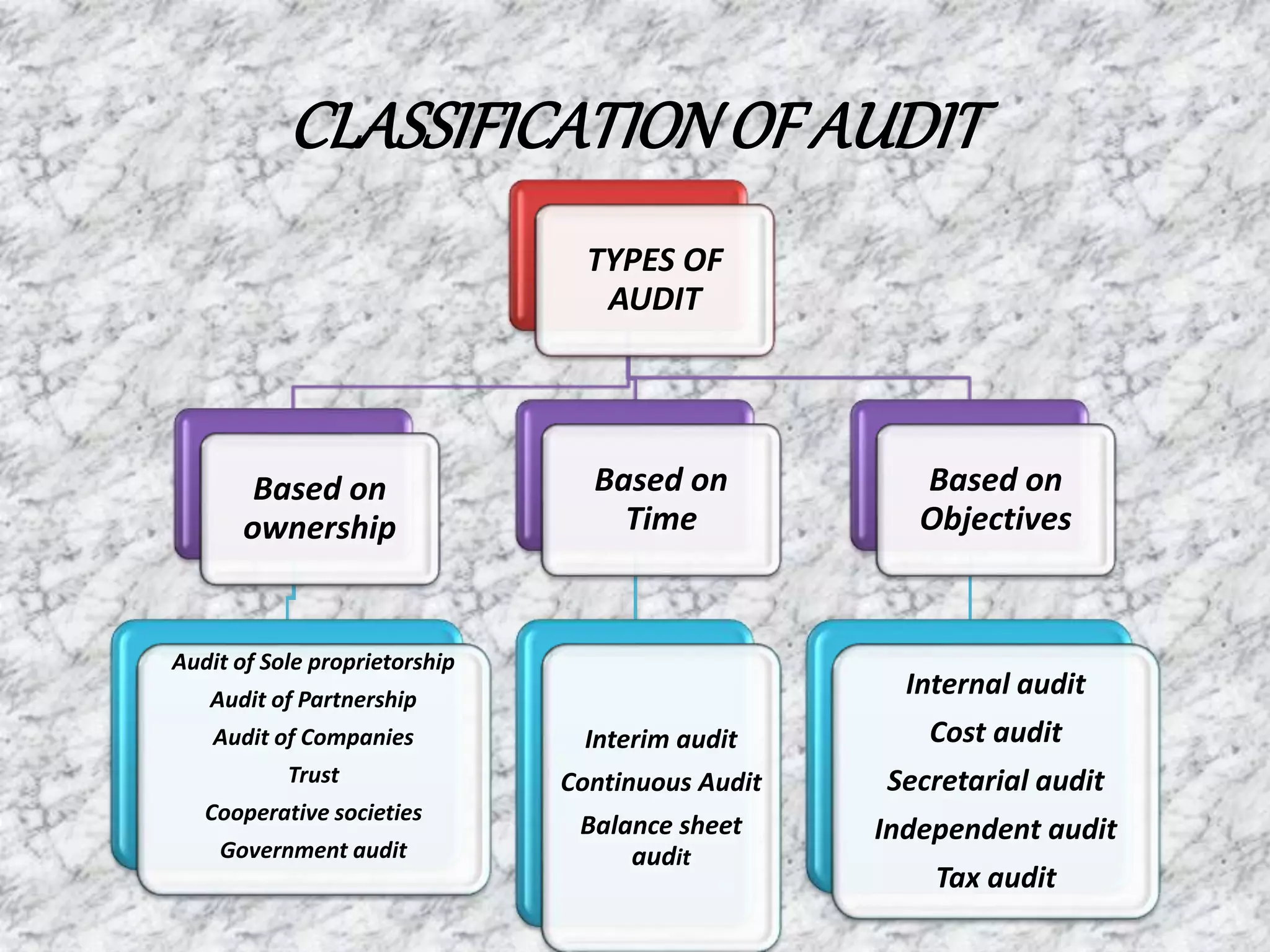

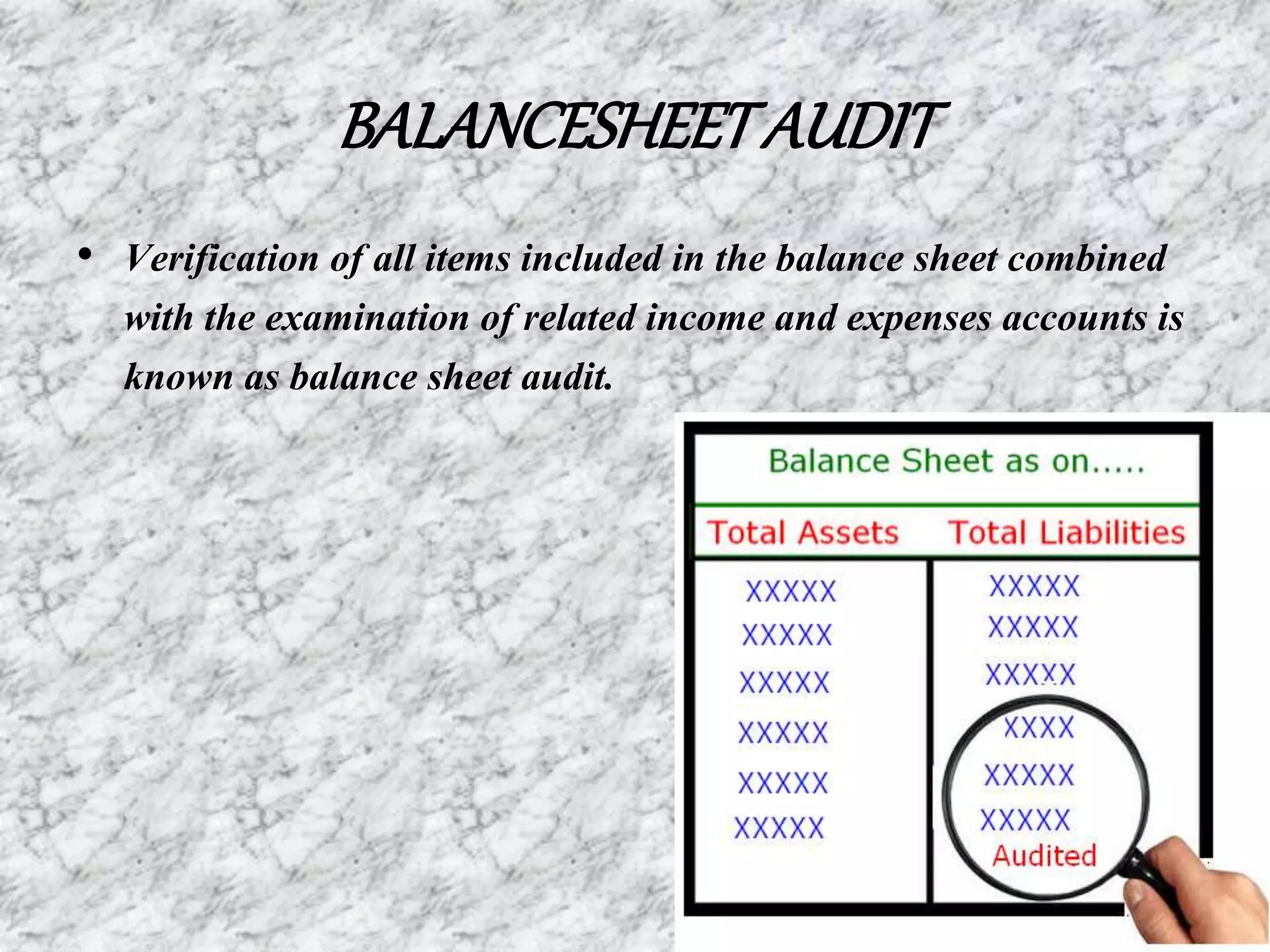

The document discusses different types of audits classified based on ownership, time, and objectives. Audits can be of sole proprietorships, partnerships, companies, trusts, cooperative societies, and government. They can also be interim, continuous, or balance sheet audits based on time. Objectives of audits include internal, independent, cost, secretarial, and tax audits. Company, partnership, and cooperative society audits have specific legal requirements and procedures to follow.