Downloaded 89 times

![…. Contd.

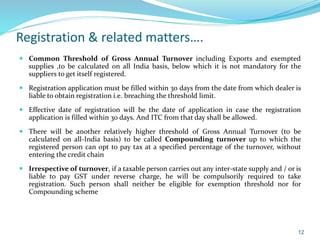

For each State the taxable person will have to take a separate registration, even

though the taxable person may be supplying goods or services or both from more than

one State as a single legal entity.

Multiple registrations within one State to business verticals [as defined in Accounting

Standard (AS) 17 issued by ICAI] of a taxable person may also be permitted, subject to all

the verticals being on the same scheme of tax treatment if the GST Law so provides.

Non-resident Supplier is a person who, in the course of business, makes an intra-state

supply of goods or services or both, but is not a resident in the state in which he has

applied for registration, but is already registered in any other state.

Supplier who is not registered on regular basis, whether on mandatory or voluntary basis,

in other State (s) and desires to conduct business in a particular State for a limited

period, will have to obtain registration in that State for that limited period. Such

suppliers are known as casual dealers and shall not be allowed to opt for composition

scheme. However, the supplier would be eligible to claim ITC on purchases / inward

supplies.

13](https://image.slidesharecdn.com/gst-151223044535/85/Understanding-GST-and-its-implications-13-320.jpg)

This document provides information on India's current and proposed indirect tax structures. The current system includes taxes levied by the central and state governments, while the proposed GST system would introduce CGST, SGST and IGST. Key features of GST include a dual-levy structure, seamless credit across states, and the replacement of multiple taxes with one. The document also outlines registration requirements, returns, and other operational details of the proposed GST system.