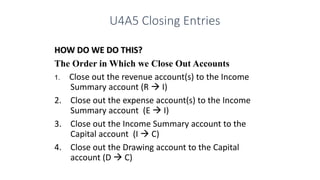

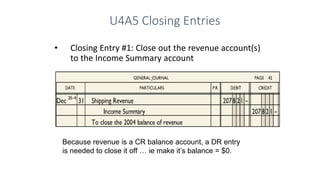

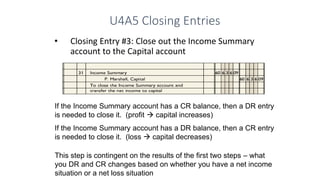

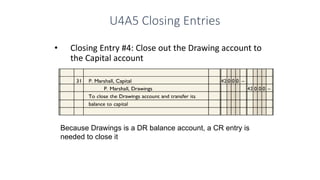

Closing entries are made at the end of an accounting period to close out the nominal accounts of revenues, expenses, and drawings so that their balances do not carry over to the next period. There are four closing entry steps: 1) revenues are closed to the income summary account, 2) expenses are closed to the income summary account, 3) the income summary account is closed to capital, and 4) the drawings account is closed to capital. After the closing entries, a post-closing trial balance is prepared to check the accuracy of the ledger and ensure the nominal accounts have zero balances.