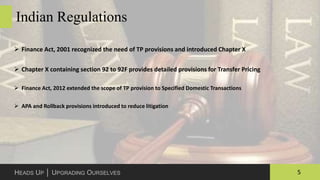

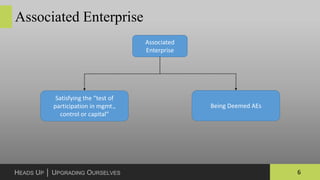

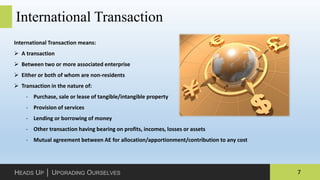

1. Transfer pricing regulations are necessary for tax administrations and taxpayers to protect tax bases, eliminate double taxation, and enhance cross-border trade. Under Indian regulations, transfer pricing provisions apply to international transactions between associated enterprises and specified domestic transactions.

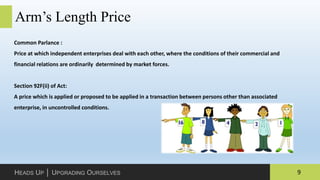

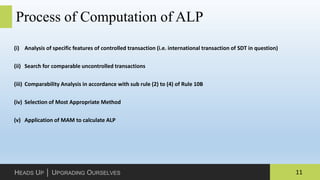

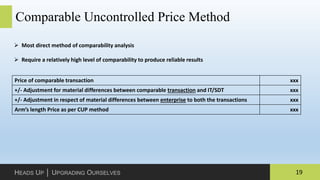

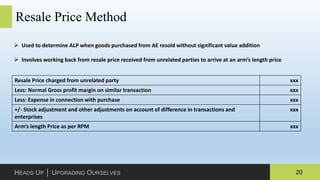

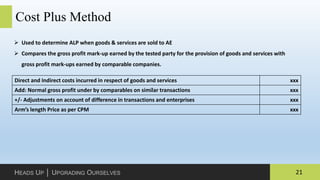

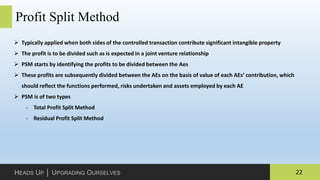

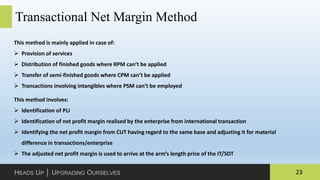

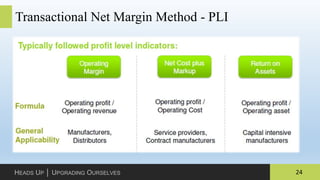

2. To determine the arm's length price for related party transactions, taxpayers must analyze transaction features, identify comparable uncontrolled transactions, select the most appropriate transfer pricing method, and apply the method to calculate the arm's length price. Common methods include comparable uncontrolled price method, resale price method, cost plus method, transactional net margin method, and profit split method.

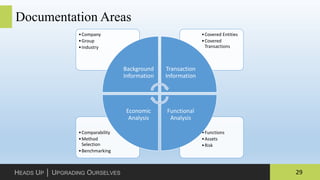

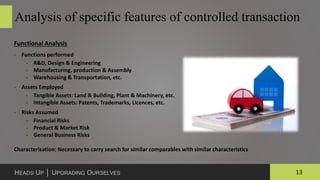

3. Taxpayers must maintain thorough transfer pricing documentation covering functions, assets, risks, comparables analysis

![27HEADS UP │ UPGRADING OURSELVES

Contemporaneity of Data [Contd…]

Current Developments:

Data for current year or FY preceding the current year shall be used for comparability

Where the CUT has been identified on the basis of data relating to the current year and the enterprise

undertaking the said uncontrolled transaction has in either or both of the two financial years immediately

preceding the current year undertaken similar comparable uncontrolled transaction, then the weighted average

of the prices of the CUT undertaken in the current year and in the preceding two years shall be used.

Where the CUT has been identified on the basis of the data relating to the financial year immediately preceding

the current year and the enterprises undertaking the said uncontrolled transaction, has in the financial year

immediately preceding the said financial year undertaken the same or similar comparable uncontrolled

transaction, then the weighted average of the prices of the CUT undertaken in the aforesaid period of two years

shall be used for determining the arm’s length price.](https://image.slidesharecdn.com/transferpricing-basics-160725081052/85/Transfer-pricing-basics-27-320.jpg)