Download to read offline

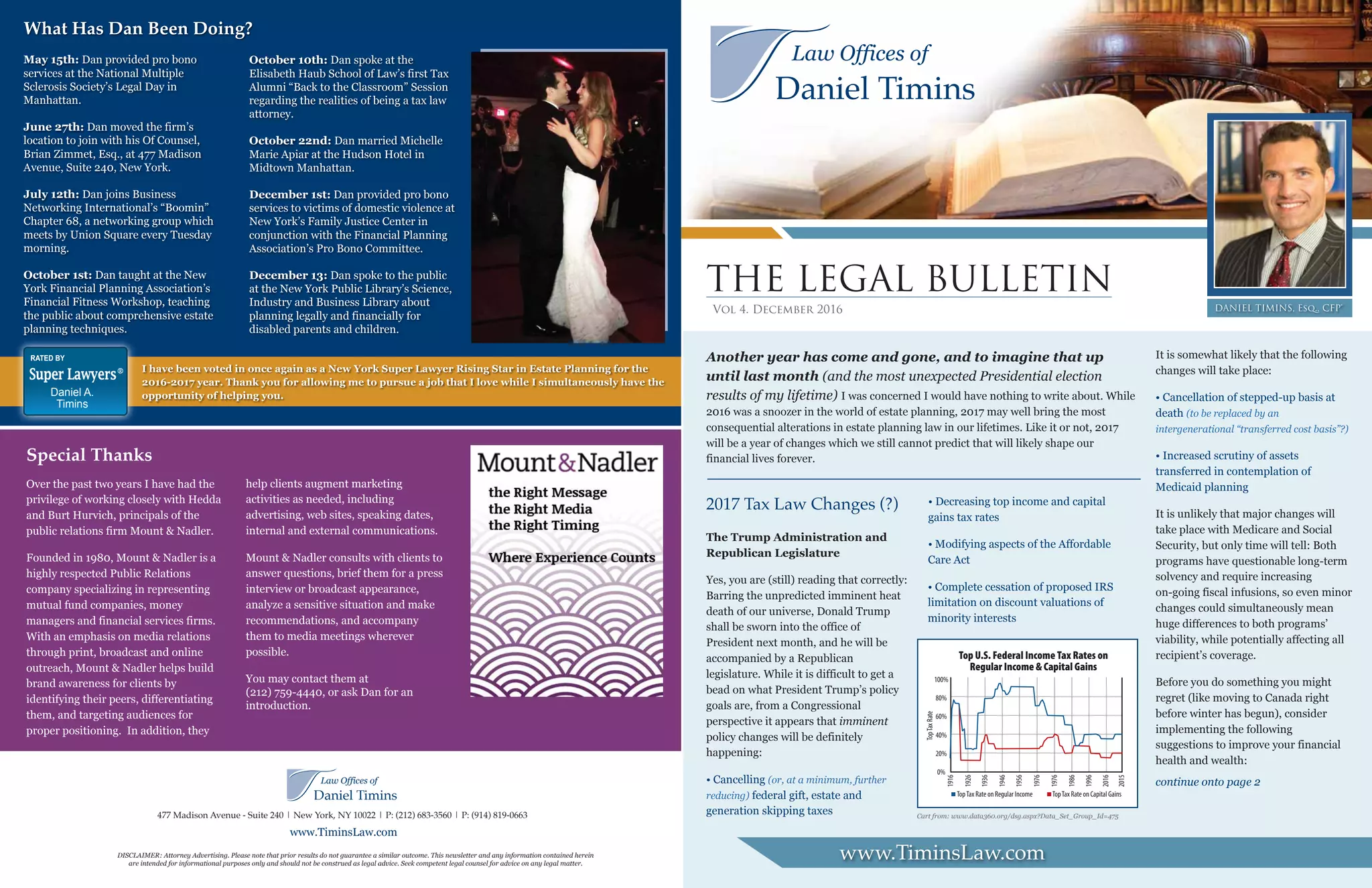

The document discusses how 2017 may bring significant changes to estate planning law due to potential tax law changes under the new Trump administration and Republican legislature. It suggests that changes like cancelling the federal estate tax and decreasing income and capital gains taxes are possible. This would likely lead to increased scrutiny of Medicaid planning transfers and changes to the stepped-up basis rule. The summary also notes that while trusts will still be important for protecting assets from creditors, divorces, and ensuring qualification for government assistance, estate attorneys will continue to have relevance beyond estate tax planning.

![A New Product Line Irs Supermarket[1]](https://cdn.slidesharecdn.com/ss_thumbnails/anewproductlineirssupermarket1-100310144627-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)