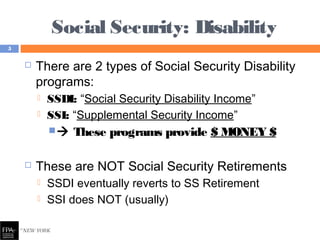

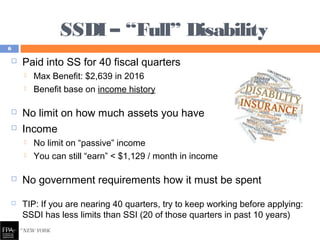

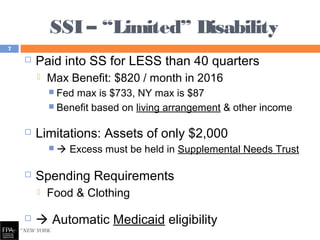

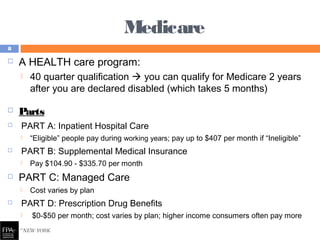

Download to read offline

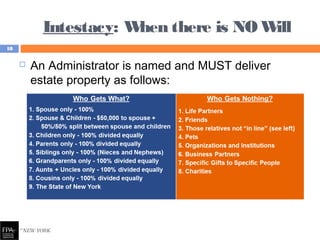

![Probate v. Non-Probate

“Operation of Law” Transfers Probate /Administration

Anything with a “Beneficiary Designation”

Because we kno w who it g o e s to at de ath

•Jointly Owned Property

•Some Business Agreements

•Retirement Plans

•Life Insurance

•Transfer on Death [“TOD”] accounts

•Trusts

All you need is a Death Certificate to

collect these (if you are the beneficiary)

This is what transfers through your

WILL or Intestacy

Because we do n’t auto m atically

kno w who it g o e s to at de ath

This includes all property not listed

under “Operation of Law”

(I.e. everything else)

2 Legal Procedures:

• If there is a valid Will = “Probate”

• If NO Will = “Administration”

16](https://image.slidesharecdn.com/8cac7710-db38-41e4-a258-8899421ff4a9-161215164035/85/SIBL-Presentation-Planning-for-the-Disabled-16-320.jpg)

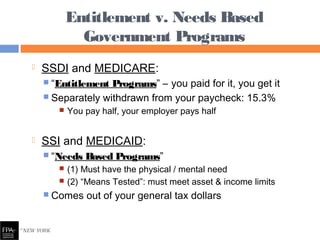

(1) The document discusses financial planning strategies for disabled individuals and their beneficiaries to optimize the use of government programs while protecting family assets. (2) It explains the differences between entitlement programs like SSDI and Medicaid, which are based on contributions, versus needs-based programs like SSI that have asset and income limits. (3) The document provides an overview of trusts, such as supplemental needs trusts, Medicaid asset protection trusts, and pooled trusts, that allow beneficiaries to receive government benefits while preserving assets for their care and quality of life.