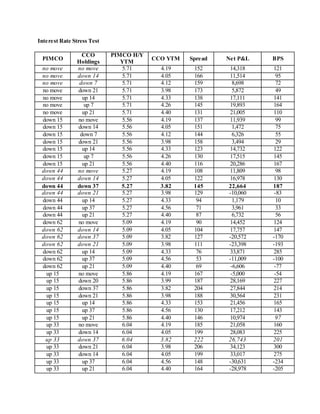

The document recommends swapping a Pimco bond for a Clear Channel Holdings bond. It analyzes both bonds and predicts a 25 basis point decline in interest rates. Clear Channel's bond has a longer duration and maturity, higher yield, and is expected to decrease 44 basis points more than Pimco based on its correlations with treasury yields and stock market performance. The swap would increase the portfolio's duration and expected return.