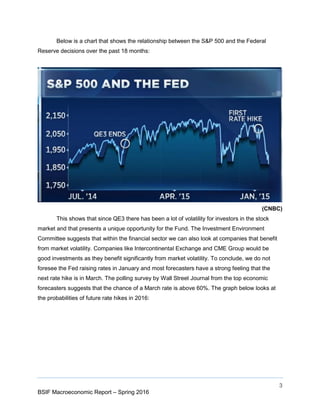

The report provides an overview of macroeconomic trends and outlooks for various regions and sectors. For the domestic economy, while facing some headwinds, growth is expected to continue in 2016 driven by strong consumer spending. In Europe, recovery is expected to continue but at a slow pace due to global uncertainties. China is undergoing an economic transition and growth is projected to slow, posing risks globally. Emerging markets face challenges from China's slowdown and commodity price declines but conditions are projected to improve in 2016.