The Return of Depression Economics

•Download as PPT, PDF•

1 like•241 views

An analysis on the current debt levels and its effect on the economy of the world followed by analysis on the gold and oil market.

Report

Share

Report

Share

Recommended

June 15 I Session 2 I GBIH

The stock market has surged despite a struggling real economy, due to optimism around vaccines, big tech companies' dominance, and monetary policy support. However, this disconnect may not always support gold prices. While high inflation expectations and money supply growth could lead to longer-term stagflation, supporting gold, a stock market decline caused by tighter monetary policy may hurt gold as well. The impact on gold depends on the underlying reasons for any shifts in stock valuations or monetary conditions.

June 20 I Session 1 I GBIH

The document discusses whether the current economic boom in the US will continue. It notes that while the US GDP has recovered from the pandemic recession, there are threats on the horizon. Inflation is rising due to excess stimulus and debt levels are high, which could cause economic turbulence if interest rates rise. The recovery also remains vulnerable to coronavirus variants. Overall, the document argues while the economy has recovered, threats remain that could undermine sustained growth and support further gold price rallies.

Is Quantitative Easing Beneficial To The Global Economy

Quantitative easing is a monetary policy used by central banks to stimulate their economy by increasing the money supply. The central bank creates money to buy government bonds from banks in exchange for cash, increasing bank reserves. This is intended to improve credit flow. However, excessive money creation can cause currency devaluation and inflation. While quantitative easing aims to boost the domestic economy, it has international impacts like currency fluctuations, trade imbalances, rising commodity prices, and challenges for emerging markets and debtors.

The Global Economic Forces | Richard Tan Success Resources

Singapore is a small but prosperous country that conducts business within the global economy, which it has no control over. To make wise investments, Singaporeans must understand the forces driving global economic developments, as these forces will ultimately determine Singapore's stock market, property market, currency value, and trade volumes. The document goes on to explain that the global economy is in crisis because too much credit has been created worldwide that cannot be repaid. It uses the analogy of the global economy being like an inflated rubber raft that is sinking due to holes created by debt defaults.

The Global Economic Forces (Part 2)| Richard Tan Success Resources

Global economic forces have a significant impact on Singapore's economy through push and pull factors. When economies struggle, asset values decline and people are endangered, prompting policymakers to intervene to boost asset prices and stimulate growth. For instance, US quantitative easing increases Singapore's costs by pushing up food and commodity prices. China's credit expansion during its 2009 crisis drove up global commodity prices and Singapore property values as Chinese investors sought properties abroad. While Singapore tries to manage external influences, there is only so much it can do as the global economy remains volatile.

Jonathan Le Roith - Sell Everything Give it a Break Andy

The document discusses the recent declines in global stock markets and commodities prices. It argues that while issues like slowing Chinese growth and low oil prices were known, recent fears have caused a sell-off. However, the document asserts that the US and UK economies remain relatively insulated from China's problems. It predicts that accommodative monetary policies will continue to support modest economic recovery and buoy stock prices. The document concludes by suggesting the recent panic creates buying opportunities for long-term investors.

June 11 I Session 1 I GBIH

The document discusses how growing acceptance of aggressive fiscal policy could support gold prices over the long term. It notes that government deficits have increased substantially during the pandemic, distributing funds more widely than in previous crises. This may boost inflation and set a precedent for larger responses that increase debt. While rising bond yields recently pressured gold, real yields remain low and inflation expectations are up, suggesting the Fed may act to curb rates, supporting gold. The document analyzes factors that could cause rates and gold prices to rise or fall in the near term.

Money Market Failings

Cheviot Asset Management discusses recent changes to US Money Market Fund regulations that allow fund managers to suspend redemptions in extreme situations, concentrating moral hazard. This undermines the concept of money market funds providing risk-free returns and absolute liquidity. A secret meeting of central bankers was held to discuss the unstable global currency market architecture and transition to a new world currency order to avoid sovereign defaults, which could have consequences similar to the 1944 Bretton Woods accord. Rising global food prices may trigger a full-scale currency crisis if not addressed by agreements between governments.

Recommended

June 15 I Session 2 I GBIH

The stock market has surged despite a struggling real economy, due to optimism around vaccines, big tech companies' dominance, and monetary policy support. However, this disconnect may not always support gold prices. While high inflation expectations and money supply growth could lead to longer-term stagflation, supporting gold, a stock market decline caused by tighter monetary policy may hurt gold as well. The impact on gold depends on the underlying reasons for any shifts in stock valuations or monetary conditions.

June 20 I Session 1 I GBIH

The document discusses whether the current economic boom in the US will continue. It notes that while the US GDP has recovered from the pandemic recession, there are threats on the horizon. Inflation is rising due to excess stimulus and debt levels are high, which could cause economic turbulence if interest rates rise. The recovery also remains vulnerable to coronavirus variants. Overall, the document argues while the economy has recovered, threats remain that could undermine sustained growth and support further gold price rallies.

Is Quantitative Easing Beneficial To The Global Economy

Quantitative easing is a monetary policy used by central banks to stimulate their economy by increasing the money supply. The central bank creates money to buy government bonds from banks in exchange for cash, increasing bank reserves. This is intended to improve credit flow. However, excessive money creation can cause currency devaluation and inflation. While quantitative easing aims to boost the domestic economy, it has international impacts like currency fluctuations, trade imbalances, rising commodity prices, and challenges for emerging markets and debtors.

The Global Economic Forces | Richard Tan Success Resources

Singapore is a small but prosperous country that conducts business within the global economy, which it has no control over. To make wise investments, Singaporeans must understand the forces driving global economic developments, as these forces will ultimately determine Singapore's stock market, property market, currency value, and trade volumes. The document goes on to explain that the global economy is in crisis because too much credit has been created worldwide that cannot be repaid. It uses the analogy of the global economy being like an inflated rubber raft that is sinking due to holes created by debt defaults.

The Global Economic Forces (Part 2)| Richard Tan Success Resources

Global economic forces have a significant impact on Singapore's economy through push and pull factors. When economies struggle, asset values decline and people are endangered, prompting policymakers to intervene to boost asset prices and stimulate growth. For instance, US quantitative easing increases Singapore's costs by pushing up food and commodity prices. China's credit expansion during its 2009 crisis drove up global commodity prices and Singapore property values as Chinese investors sought properties abroad. While Singapore tries to manage external influences, there is only so much it can do as the global economy remains volatile.

Jonathan Le Roith - Sell Everything Give it a Break Andy

The document discusses the recent declines in global stock markets and commodities prices. It argues that while issues like slowing Chinese growth and low oil prices were known, recent fears have caused a sell-off. However, the document asserts that the US and UK economies remain relatively insulated from China's problems. It predicts that accommodative monetary policies will continue to support modest economic recovery and buoy stock prices. The document concludes by suggesting the recent panic creates buying opportunities for long-term investors.

June 11 I Session 1 I GBIH

The document discusses how growing acceptance of aggressive fiscal policy could support gold prices over the long term. It notes that government deficits have increased substantially during the pandemic, distributing funds more widely than in previous crises. This may boost inflation and set a precedent for larger responses that increase debt. While rising bond yields recently pressured gold, real yields remain low and inflation expectations are up, suggesting the Fed may act to curb rates, supporting gold. The document analyzes factors that could cause rates and gold prices to rise or fall in the near term.

Money Market Failings

Cheviot Asset Management discusses recent changes to US Money Market Fund regulations that allow fund managers to suspend redemptions in extreme situations, concentrating moral hazard. This undermines the concept of money market funds providing risk-free returns and absolute liquidity. A secret meeting of central bankers was held to discuss the unstable global currency market architecture and transition to a new world currency order to avoid sovereign defaults, which could have consequences similar to the 1944 Bretton Woods accord. Rising global food prices may trigger a full-scale currency crisis if not addressed by agreements between governments.

The Great Fall in China August 2015 - Special market bulletin St. James's Place

Monday 24th August 2015 saw one of the biggest stock market crashes in China. St. James's Place published a special bulletin to let their investors know to stay clam and that the incident wasn't unexpected. This bulletin contains some great advice.

201010 Investment Outlook 4 Q10

The document provides a quarterly investment outlook and discusses recent volatility in financial markets. It notes that sentiment has been swinging between irrational optimism and excessive pessimism. While most equity markets have rebounded in recent months, bond prices have also risen due to deflation fears. The document discusses the debate around whether the threats are inflation or deflation and argues that subdued growth does not necessarily mean deflation will take hold. It outlines some areas where investment opportunities still exist, such as global equity income funds and Japanese equities, and concludes by emphasizing the need for diversification given the current environment of low predictability.

Purging Prosperity

The document discusses economic cycles and recessions. It argues that recessions are a natural and necessary part of the economic cycle that help correct imbalances by purging excesses. Recessions restore equilibrium by bringing prices and production back in line with demand. Historically, markets have expanded and contracted efficiently over the long term. The document advocates viewing recessions as normal cycles rather than catastrophes and suggests that recessions present opportunities for investment and improvement.

The Case for Sterling - September 2013

The document summarizes the case for the appreciation of the British pound sterling over the coming years. It discusses how sterling declined significantly from 1987 to 2012 due to a series of policy errors and a perfect storm caused by the global financial crisis. However, it argues that sterling is now undervalued and conditions that caused its decline are no longer present, suggesting the currency is poised to appreciate back to more normal levels based on economic fundamentals.

The Super-Cycle Report

The world economy has twice before enjoyed a super-cycle. It may now be

experiencing its third super-cycle.

To put it in context, it is defined here as, “A period of historically high global growth,

lasting a generation or more, driven by increasing trade, high rates of investment,

urbanisation and technological innovation, characterised by the emergence of large,

new economies, first seen in high catch-up growth rates across the emerging world.”

The first super-cycle took place during the second half of the 19th century, from 1870

until 1913, the eve of the First World War. At that time, the world economy witnessed

a significant step-up in its rate of growth, rising 2.7% on average per annum in

volume, or real, terms. That was a full 1% higher than the average growth rate seen

during the previous half-century. America was the big gainer, moving from the fourthlargest

to the largest economy. The second super-cycle was after the Second World

War until the early 1970s. World growth averaged a huge 5% per annum, again in

real or inflation-adjusted terms. Japan and the Asian tigers saw the biggest gains

over this time. Japan, for instance, moved from 3% to 10% of the world economy.

The Global Economic Forces | Richard Tan Success Resources

The global economy is like a giant rubber raft that has been inflated with too much credit. This raft is sinking under the weight of debt that cannot be repaid. When the raft starts to sink, asset prices fall and the world's seven billion people are endangered. To prevent a repeat of the Great Depression, governments around the world intervene to reflate the raft by increasing asset prices. These global economic forces profoundly impact Singapore through higher inflation when other countries print money, and through rising property prices when credit expansion in countries like China causes foreign investors to park money in Singapore real estate. As the global economic crisis is far from over, wise Singaporean investors will monitor government actions and respond to reflations of

RESEARCH - The Fairfax Monitor - Edition 2

The document discusses whether the current economic environment is more likely to lead to inflation or deflation. It analyzes factors influencing the debate such as declining asset prices, falling consumer demand, and aggressive monetary stimulus by central banks. While central banks have taken inflationary actions, the document concludes deflation remains the greater threat due to continued weakness in the banking system, low consumer spending, and lack of signs of rising inflation. The environment favors bonds over stocks and commodities in the near term until the banking system shows more stability.

How Will Inflation Affect Your Investments?

This document discusses how inflation affects investments. It explains that inflation erodes the purchasing power of money over time. Investors need to earn returns higher than the inflation rate to maintain purchasing power. The large government spending to address the pandemic may cause inflation if excess money enters the economy faster than new goods and services. To fight inflation, the government raises interest rates to reduce money supply and slow economic growth. Investors should examine how different assets may perform during inflationary periods and adjust their portfolios accordingly.

The Henley Group's Market Outlook June 2013

The "Henley Market Outlook" gives our current assessment of the six Henley asset classes. For more information please email ts@thehenleygroup.com.hk

Finlight Research - Market perspectives - Dec 2014

« Market Perspectives » est notre revue mensuelle des marchés. Elle présente de la façon la plus synthétique possible :

- notre analyse des principaux faits marquants et indicateurs macro susceptibles de dessiner les marchés sur le mois.

- notre vision sur les différentes classes d’actifs

Cette revue sera continument enrichie avec nos indicateurs quantitatifs.

La plupart de nos analyses sont disponibles sur www.finlightresearch.com

Our monthly publication “Market Perspectives” presents a synthetic view of all the asset classes we cover.

The report is composed of six sections covering Macro, Equities, FI & credit, FX, Commodities and Alternatives.

Each section is preceded by a summary of our views on the related asset class.

Most of our publications are available on our web site www.finlightresearch.com

Fasanara Capital Investment Outlook | February 1st 2015

Fasanara Capital Investment Outlook | February 1st 2015

1. Seismic Activity On The Rise

2. No Volatility No Gain

3. The Role Of Optionality

4. Crystal Ball

5. Deflation Is A Multi-Year Process

6. Three Big Trades for 2015

3 Jan 2009: a bottom in breakevens, commodities, and global yields?

The response of the authorities has been without precedent - the US has a new president, and perhaps confidence in the new administration may stave off the worst consequences of the epidemic contagion of fear - for now, at least. It is certain that for the time being we shall avoid the 29-33 collapse that was associated with every sovereign issuer in Europe except Britain, and much of Latin America and Asia defaulting as well as large numbers of banks in the US (in the days before deposit insurance).

Is the US dollar bottoming?

The US dollar may be bottoming based on several factors:

1) Valuation measures like the Big Mac Index and OECD measures imply the dollar is undervalued by 30-35%

2) Increases in US oil and gas production from shale could reduce US imports and improve the trade balance by a third

3) A turnaround in US economic confidence and growth could support a rise in the dollar through upward revisions to interest rate expectations

Et tu draghi final

This document discusses trends and reversals in financial markets and the economy. It notes that while trend reversals create fear, they are natural and inevitable. The key is understanding the dominant trend versus short-term volatility. It also discusses how central banks have intervened in markets to smooth economic cycles, but that their policies may no longer be appropriate given high debt levels and slower growth. While recent trend reversals in markets have been correlated, the document argues they will likely revert back to the dominant downward trend.

Fasanara Capital Investment Outlook | September 1st 2014

- Tensions with Russia over Ukraine are seen as transitory but could cause market volatility in the near-term. Deflation in Europe is viewed as a more structural issue that will affect markets for the long-term.

- The ECB is expected to take a three step approach - enhancing terms for T-LTROs, finalizing stress tests, and delivering their own version of quantitative easing.

- Three top investment opportunities are seen in European deflation trades benefiting from ECB action, peripheral European equity with upside from an inflated bubble, and Japanese equity benefiting from further stimulus.

Is japan's ecomomy facing another lost decade or is it ready to boom

The document discusses whether Japan's economy is facing another "lost decade" of weak growth or if it is poised to boom. While Japan's economy has grown weakly for decades and recently contracted further, the Bank of Japan has now committed to a 1% inflation target and other innovative measures that could lead to real GDP growth. If a surge in growth occurs, it would boost Japanese stocks and the global economy. However, time will tell if Japan is truly ready to boom given its history of economic struggles.

September: Welcome To The Danger Zone

1. September is predicted to be a volatile month based on several factors: the end of the biblical Shemitah year on September 13th has historically coincided with market crashes, the start of the Year of Lucifer on September 14th, and military exercises throughout the southern US from July to September 15th called Jade Helm.

2. Key events include a possible interest rate increase by the US Federal Reserve on September 17th that could trigger emerging market turmoil, Greek legislative elections on September 20th, addresses by the Pope to the US Congress on September 24th and UN General Assembly on September 25th, and a supermoon blood moon on September 28th.

3. The document recommends buying gold and

Eurozone May 2011: Focus on slowing growth ahead not lagging inflation

Contrarian eurozone piece that ancticipated the Eurozone crisis shortly after the major bottom in German fixed income prices.

Q4_2015_2016_Outlook

The document provides an outlook for the year 2016. It begins with a base case that forecasts slow economic growth and low inflation in the US, with the S&P 500 reaching 2214.39. It identifies several "known unknowns" that could impact the outlook, including monetary policy changes, the global economy, the upcoming US election, and geopolitical issues. It then examines the weak US economic recovery in more depth, attributing it to high private sector debt levels. International growth is also constrained by debt and aging populations. China's transition away from its low-cost manufacturing model poses risks if not managed properly.

What are the best investments if the fed raises interest rate?

The document discusses factors that may influence the Federal Reserve's decision about whether and when to raise interest rates for the first time since 2006. It presents arguments on both sides of the issue, noting pressure to raise rates to combat future recessions but also factors keeping rates low like low inflation. It then discusses potential effects of rate changes on various asset classes like gold, oil, the US dollar, and the Australian dollar. Overall it analyzes how different investment classes may be affected depending on whether and when the Fed decides to raise interest rates.

Depression economics

The document summarizes key points from a book about global financial markets and the dangers they pose. It discusses how the book traces financial crises from the 1930s onward and analyzes specific crises in countries like Mexico, Asia, Japan, Russia, and Brazil. These crises were typically triggered by changes in international investors' confidence that led to plunging currencies, rising interest rates, and recessions. While recessions are natural, modern economic policy could help tame problems from business cycles by encouraging saving during booms. However, the book did not fully explain how countries already suffering could recover from financial crises.

Recession.Ppt By Yas

A recession is defined as a period of reduced economic activity where a country's GDP declines for at least two consecutive quarters. It can be caused by currency crises, energy crises, underconsumption, overproduction, or financial crises. Past recessions in the US lasted between 8 months to 2 years. During recessions, unemployment typically rises 2-3 percentage points, adding 3-5 million newly unemployed Americans. However, job losses mainly affect low-skilled workers, as skilled jobs remain available. As a recession looms, human resources management plays a strategic role in optimizing staffing, boosting productivity, managing compensation and benefits, and retaining key employees through communication and motivation.

More Related Content

What's hot

The Great Fall in China August 2015 - Special market bulletin St. James's Place

Monday 24th August 2015 saw one of the biggest stock market crashes in China. St. James's Place published a special bulletin to let their investors know to stay clam and that the incident wasn't unexpected. This bulletin contains some great advice.

201010 Investment Outlook 4 Q10

The document provides a quarterly investment outlook and discusses recent volatility in financial markets. It notes that sentiment has been swinging between irrational optimism and excessive pessimism. While most equity markets have rebounded in recent months, bond prices have also risen due to deflation fears. The document discusses the debate around whether the threats are inflation or deflation and argues that subdued growth does not necessarily mean deflation will take hold. It outlines some areas where investment opportunities still exist, such as global equity income funds and Japanese equities, and concludes by emphasizing the need for diversification given the current environment of low predictability.

Purging Prosperity

The document discusses economic cycles and recessions. It argues that recessions are a natural and necessary part of the economic cycle that help correct imbalances by purging excesses. Recessions restore equilibrium by bringing prices and production back in line with demand. Historically, markets have expanded and contracted efficiently over the long term. The document advocates viewing recessions as normal cycles rather than catastrophes and suggests that recessions present opportunities for investment and improvement.

The Case for Sterling - September 2013

The document summarizes the case for the appreciation of the British pound sterling over the coming years. It discusses how sterling declined significantly from 1987 to 2012 due to a series of policy errors and a perfect storm caused by the global financial crisis. However, it argues that sterling is now undervalued and conditions that caused its decline are no longer present, suggesting the currency is poised to appreciate back to more normal levels based on economic fundamentals.

The Super-Cycle Report

The world economy has twice before enjoyed a super-cycle. It may now be

experiencing its third super-cycle.

To put it in context, it is defined here as, “A period of historically high global growth,

lasting a generation or more, driven by increasing trade, high rates of investment,

urbanisation and technological innovation, characterised by the emergence of large,

new economies, first seen in high catch-up growth rates across the emerging world.”

The first super-cycle took place during the second half of the 19th century, from 1870

until 1913, the eve of the First World War. At that time, the world economy witnessed

a significant step-up in its rate of growth, rising 2.7% on average per annum in

volume, or real, terms. That was a full 1% higher than the average growth rate seen

during the previous half-century. America was the big gainer, moving from the fourthlargest

to the largest economy. The second super-cycle was after the Second World

War until the early 1970s. World growth averaged a huge 5% per annum, again in

real or inflation-adjusted terms. Japan and the Asian tigers saw the biggest gains

over this time. Japan, for instance, moved from 3% to 10% of the world economy.

The Global Economic Forces | Richard Tan Success Resources

The global economy is like a giant rubber raft that has been inflated with too much credit. This raft is sinking under the weight of debt that cannot be repaid. When the raft starts to sink, asset prices fall and the world's seven billion people are endangered. To prevent a repeat of the Great Depression, governments around the world intervene to reflate the raft by increasing asset prices. These global economic forces profoundly impact Singapore through higher inflation when other countries print money, and through rising property prices when credit expansion in countries like China causes foreign investors to park money in Singapore real estate. As the global economic crisis is far from over, wise Singaporean investors will monitor government actions and respond to reflations of

RESEARCH - The Fairfax Monitor - Edition 2

The document discusses whether the current economic environment is more likely to lead to inflation or deflation. It analyzes factors influencing the debate such as declining asset prices, falling consumer demand, and aggressive monetary stimulus by central banks. While central banks have taken inflationary actions, the document concludes deflation remains the greater threat due to continued weakness in the banking system, low consumer spending, and lack of signs of rising inflation. The environment favors bonds over stocks and commodities in the near term until the banking system shows more stability.

How Will Inflation Affect Your Investments?

This document discusses how inflation affects investments. It explains that inflation erodes the purchasing power of money over time. Investors need to earn returns higher than the inflation rate to maintain purchasing power. The large government spending to address the pandemic may cause inflation if excess money enters the economy faster than new goods and services. To fight inflation, the government raises interest rates to reduce money supply and slow economic growth. Investors should examine how different assets may perform during inflationary periods and adjust their portfolios accordingly.

The Henley Group's Market Outlook June 2013

The "Henley Market Outlook" gives our current assessment of the six Henley asset classes. For more information please email ts@thehenleygroup.com.hk

Finlight Research - Market perspectives - Dec 2014

« Market Perspectives » est notre revue mensuelle des marchés. Elle présente de la façon la plus synthétique possible :

- notre analyse des principaux faits marquants et indicateurs macro susceptibles de dessiner les marchés sur le mois.

- notre vision sur les différentes classes d’actifs

Cette revue sera continument enrichie avec nos indicateurs quantitatifs.

La plupart de nos analyses sont disponibles sur www.finlightresearch.com

Our monthly publication “Market Perspectives” presents a synthetic view of all the asset classes we cover.

The report is composed of six sections covering Macro, Equities, FI & credit, FX, Commodities and Alternatives.

Each section is preceded by a summary of our views on the related asset class.

Most of our publications are available on our web site www.finlightresearch.com

Fasanara Capital Investment Outlook | February 1st 2015

Fasanara Capital Investment Outlook | February 1st 2015

1. Seismic Activity On The Rise

2. No Volatility No Gain

3. The Role Of Optionality

4. Crystal Ball

5. Deflation Is A Multi-Year Process

6. Three Big Trades for 2015

3 Jan 2009: a bottom in breakevens, commodities, and global yields?

The response of the authorities has been without precedent - the US has a new president, and perhaps confidence in the new administration may stave off the worst consequences of the epidemic contagion of fear - for now, at least. It is certain that for the time being we shall avoid the 29-33 collapse that was associated with every sovereign issuer in Europe except Britain, and much of Latin America and Asia defaulting as well as large numbers of banks in the US (in the days before deposit insurance).

Is the US dollar bottoming?

The US dollar may be bottoming based on several factors:

1) Valuation measures like the Big Mac Index and OECD measures imply the dollar is undervalued by 30-35%

2) Increases in US oil and gas production from shale could reduce US imports and improve the trade balance by a third

3) A turnaround in US economic confidence and growth could support a rise in the dollar through upward revisions to interest rate expectations

Et tu draghi final

This document discusses trends and reversals in financial markets and the economy. It notes that while trend reversals create fear, they are natural and inevitable. The key is understanding the dominant trend versus short-term volatility. It also discusses how central banks have intervened in markets to smooth economic cycles, but that their policies may no longer be appropriate given high debt levels and slower growth. While recent trend reversals in markets have been correlated, the document argues they will likely revert back to the dominant downward trend.

Fasanara Capital Investment Outlook | September 1st 2014

- Tensions with Russia over Ukraine are seen as transitory but could cause market volatility in the near-term. Deflation in Europe is viewed as a more structural issue that will affect markets for the long-term.

- The ECB is expected to take a three step approach - enhancing terms for T-LTROs, finalizing stress tests, and delivering their own version of quantitative easing.

- Three top investment opportunities are seen in European deflation trades benefiting from ECB action, peripheral European equity with upside from an inflated bubble, and Japanese equity benefiting from further stimulus.

Is japan's ecomomy facing another lost decade or is it ready to boom

The document discusses whether Japan's economy is facing another "lost decade" of weak growth or if it is poised to boom. While Japan's economy has grown weakly for decades and recently contracted further, the Bank of Japan has now committed to a 1% inflation target and other innovative measures that could lead to real GDP growth. If a surge in growth occurs, it would boost Japanese stocks and the global economy. However, time will tell if Japan is truly ready to boom given its history of economic struggles.

September: Welcome To The Danger Zone

1. September is predicted to be a volatile month based on several factors: the end of the biblical Shemitah year on September 13th has historically coincided with market crashes, the start of the Year of Lucifer on September 14th, and military exercises throughout the southern US from July to September 15th called Jade Helm.

2. Key events include a possible interest rate increase by the US Federal Reserve on September 17th that could trigger emerging market turmoil, Greek legislative elections on September 20th, addresses by the Pope to the US Congress on September 24th and UN General Assembly on September 25th, and a supermoon blood moon on September 28th.

3. The document recommends buying gold and

Eurozone May 2011: Focus on slowing growth ahead not lagging inflation

Contrarian eurozone piece that ancticipated the Eurozone crisis shortly after the major bottom in German fixed income prices.

Q4_2015_2016_Outlook

The document provides an outlook for the year 2016. It begins with a base case that forecasts slow economic growth and low inflation in the US, with the S&P 500 reaching 2214.39. It identifies several "known unknowns" that could impact the outlook, including monetary policy changes, the global economy, the upcoming US election, and geopolitical issues. It then examines the weak US economic recovery in more depth, attributing it to high private sector debt levels. International growth is also constrained by debt and aging populations. China's transition away from its low-cost manufacturing model poses risks if not managed properly.

What are the best investments if the fed raises interest rate?

The document discusses factors that may influence the Federal Reserve's decision about whether and when to raise interest rates for the first time since 2006. It presents arguments on both sides of the issue, noting pressure to raise rates to combat future recessions but also factors keeping rates low like low inflation. It then discusses potential effects of rate changes on various asset classes like gold, oil, the US dollar, and the Australian dollar. Overall it analyzes how different investment classes may be affected depending on whether and when the Fed decides to raise interest rates.

What's hot (20)

The Great Fall in China August 2015 - Special market bulletin St. James's Place

The Great Fall in China August 2015 - Special market bulletin St. James's Place

The Global Economic Forces | Richard Tan Success Resources

The Global Economic Forces | Richard Tan Success Resources

Finlight Research - Market perspectives - Dec 2014

Finlight Research - Market perspectives - Dec 2014

Fasanara Capital Investment Outlook | February 1st 2015

Fasanara Capital Investment Outlook | February 1st 2015

3 Jan 2009: a bottom in breakevens, commodities, and global yields?

3 Jan 2009: a bottom in breakevens, commodities, and global yields?

Fasanara Capital Investment Outlook | September 1st 2014

Fasanara Capital Investment Outlook | September 1st 2014

Is japan's ecomomy facing another lost decade or is it ready to boom

Is japan's ecomomy facing another lost decade or is it ready to boom

Eurozone May 2011: Focus on slowing growth ahead not lagging inflation

Eurozone May 2011: Focus on slowing growth ahead not lagging inflation

What are the best investments if the fed raises interest rate?

What are the best investments if the fed raises interest rate?

Viewers also liked

Depression economics

The document summarizes key points from a book about global financial markets and the dangers they pose. It discusses how the book traces financial crises from the 1930s onward and analyzes specific crises in countries like Mexico, Asia, Japan, Russia, and Brazil. These crises were typically triggered by changes in international investors' confidence that led to plunging currencies, rising interest rates, and recessions. While recessions are natural, modern economic policy could help tame problems from business cycles by encouraging saving during booms. However, the book did not fully explain how countries already suffering could recover from financial crises.

Recession.Ppt By Yas

A recession is defined as a period of reduced economic activity where a country's GDP declines for at least two consecutive quarters. It can be caused by currency crises, energy crises, underconsumption, overproduction, or financial crises. Past recessions in the US lasted between 8 months to 2 years. During recessions, unemployment typically rises 2-3 percentage points, adding 3-5 million newly unemployed Americans. However, job losses mainly affect low-skilled workers, as skilled jobs remain available. As a recession looms, human resources management plays a strategic role in optimizing staffing, boosting productivity, managing compensation and benefits, and retaining key employees through communication and motivation.

Recession

The document discusses recessions and business cycles. It defines a recession as a significant decline in national output (GDP) that typically lasts 6-18 months. Recessions increase unemployment as firms hire fewer workers when production declines. The business cycle refers to the economy regularly fluctuating between periods of growth (booms) and contraction (recessions). While called a "cycle," the fluctuations can be unpredictable in length. A depression is a more severe economic downturn than a recession, as seen in the Great Depression in the US. The Great Recession of 2008 was the worst global recession since WWII. Potential causes of recessions discussed include high interest rates, high inflation, and reduced consumer confidence.

Recession & its effects ppt

The document summarizes the effects of recession on the economies of the United Kingdom and India. It finds that the UK was more severely impacted due to its investments in risky financial products prior to the recession. In contrast, India's economy was less affected because the country's growth was robust and its financial system was not as exposed. The document recommends fiscal and monetary policies used by both countries to mitigate the recession's impacts.

Economics

This document provides an introduction to economics. It defines economics as the social science studying production, distribution, and consumption of goods and services. Economics is divided into dimensions including microeconomics, macroeconomics, positive economics, and normative economics. Microeconomics examines how individuals and firms make decisions to allocate limited resources in markets. Macroeconomics analyzes the performance, structure, and behavior of the overall economy. Positive economics describes and explains economic phenomena through facts and cause-and-effect relationships. Normative economics incorporates value judgments about what the economy should be and what policies should be recommended.

1929 Ppt

The document summarizes the key events and impacts of the Great Depression that began with the stock market crash of 1929. It describes how various sectors of the US economy such as agriculture, consumer spending and the wealth gap were struggling in the late 1920s. The stock market crash in October 1929 marked the beginning of the Great Depression, as stock prices plummeted and banks collapsed in its aftermath. Unemployment rose dramatically to 25% by 1933 as GDP fell nearly 50%. Worldwide, many countries were severely impacted due to economic interdependence and the dust bowl exacerbated problems in North America. The Depression ended during World War 2 as US factories received orders to support the war effort.

Positive and normative statements ptn

This document discusses the difference between positive and normative statements. It provides examples of each:

- Positive statements make claims that can be tested as true or false, like "the moon is made of green cheese."

- Normative statements express value judgments or opinions that cannot be tested, like "the state pension should be cut in half because pensioners are parasites."

The document emphasizes the importance of distinguishing between objective, fact-based positive statements and subjective normative statements when reading articles about current issues and policy decisions. Positive statements report facts while normative statements aim to persuade with value judgments.

Depression

This document provides an overview of depression, including its definition, types, epidemiology, etiology, pathophysiology, clinical manifestations, diagnosis, investigations, and treatment. Depression is defined as a common mental disorder characterized by depressed mood, loss of interest, feelings of guilt, sleep disturbances, low energy, and poor concentration. Major types include major depressive disorder, bipolar disorder, dysthymic disorder, and situational depression. Depression affects over 350 million people globally and is a leading cause of disability. Causes may include genetic, environmental, biochemical and neurological factors. Treatment involves antidepressant medications like SSRIs, TCAs, and MAOIs as well as psychotherapy and other non-pharmacological approaches.

Gross domestic product and gnp

The document discusses key concepts related to measuring a country's economic output, including:

- Gross Domestic Product (GDP) measures the value of all final goods and services produced within a country in a period.

- Gross National Product (GNP) includes output produced abroad by a country's citizens and excludes foreign-produced domestic output.

- GDP is calculated using the expenditure, income, and production approaches.

- Per capita GDP divides a nation's total GDP by its population for a measure of individual economic well-being.

- Real GDP adjusts for inflation to measure output in constant prices.

Causes Of Great Depression

The document discusses several causes that contributed to the Great Depression in the United States in the late 1920s and 1930s. Key factors included an unequal distribution of wealth that left many unable to purchase goods, high tariffs and war debts that reduced international trade, and overproduction in agriculture and industry that led to surpluses. The stock market crash of 1929 further exacerbated the economic crisis and led to a financial panic as banks began to fail.

GDP & GNP

This document provides information on various economic indicators and statistics. Section A defines Gross Domestic Product (GDP), real GDP, Gross National Product (GNP), per capita GDP, and net factor income. Section B discusses limitations of GDP and effects of the black market. Section C presents 2012 GDP, GDP growth rates, unemployment rates, inflation rates, and UN Human Development Index rankings for Ireland, UK, USA, Canada, Congo, China, and Moldova.

Depression

Depression is a common and serious mental disorder characterized by depressed mood, loss of interest, feelings of guilt and low self-worth, and poor concentration. It is the leading cause of disability worldwide. Depression can be reliably diagnosed and treated, although currently less than 25% of those affected have access to effective treatments. Treatment options include antidepressant medications like SSRIs and psychotherapy.

Economy type and characteristics

This document discusses different types of economic systems. It defines a traditional economy as one based on customs and traditions where resources are owned by a sovereign. A market economy is based on individual choices where private firms produce for profit. A centrally planned economy gives the government control over production and distribution. A mixed economy incorporates aspects of market and planned systems, with both government and private sectors.

Viewers also liked (13)

Similar to The Return of Depression Economics

Business Opportunities in 2016/ Investasi Tepat, Profit Hebat

Global debt levels have reached $199 trillion, with $27,200 owed per person on the planet. Debt levels continue rising exponentially across nations, with growing concerns about the sustainability of such high debt loads. The global economy is stalling despite massive monetary stimulus from central banks. With many warning signs flashing, including historic lows for commodity prices, the global financial system appears increasingly unstable and at risk of a major crisis or economic depression. Precious metals like gold are recommended as a safe haven asset to protect against such risks to the financial system.

Fasanara Capital | Investment Outlook | May 3rd 2016

1. Reflation Phase To Be Temporary, More Downside Ahead

Earlier on in 2016, ‘random and violent markets’ went off to panic mode out of (i) fears over China’s messy stock market and devaluing currency, (ii) plummeting oil price, (iii) strong US Dollar. Today, we believe complacent markets are similarly illogical and over-shooting, this time on the way up. As we re-assess the validity of the underlying risks, we expect a shift in narrative in the few months ahead and a sizeable sell-off for risk assets.

2. Four Key Conviction Ideas

We analyze below our key ideas for the next 12 months:

Short Chinese Renminbi Thesis. In Q1, China only managed to keep GDP in shape by means of graciously expanding credit by a monumental 1 trn $. Unsurprisingly, at 250% total debt on GDP, you cannot borrow 10% of GDP per quarter for long, without a currency adjustment, whether desired or not.

Short Oil Thesis. Long-term, we believe Oil will follow a volatile path around a declining trend-line, which will take it one day to sub-10$. Within 2016, we expect global aggregate demand to stay anemic and supply to surprise on the upside, inventories to grow, primarily due to the accelerating speed of technological progress.

Short S&P Thesis. To us, the S&P is priced to perfection, despite a most cloudy environment for growth and risk assets, thus representing a good value short, for limited upside is combined with the risk of a sizeable sell-off in the months ahead.

Short European Banks Thesis. We believe that micro policies at the local level, while valid, are impotent against heavy structural macro headwinds, and only the macro environment can save the banking sector in its current form in the longer-term. Macro structural headwinds for banks these days are too heavy a burden (negative sloped interest rate curves, deeply negative interest rates, deflationary economy, depressed GDP growth, over-regulation, Fintech), and will likely push valuations to new lows in the months/years ahead.

Rumpelstiltskin at the Fed by Harley Bassman, PIMCO, executive vice presiden...

Rumpelstiltskin at the Fed by Harley Bassman, PIMCO, executive vice president & portfolio manager

SUMMARY

Has the Federal Reserve reached the bottom of its policy toolkit? Many things are still possible, at least in theory, including negative interest rates (which we believe would be ineffective and potentially harmful) or a “helicopter drop” of money. Another option is to resurrect a successful plan from 83 years ago: Purchase a tremendous amount of gold at a price substantially higher than market levels.

A massive Fed gold purchase program might finally lift the anchor on inflationary expectations and consumers’ spending habits. It would increase the price of a globally recognized store of value. It almost sounds like a fairy tale – but it’s happened before.

Though it seems incredibly farfetched, a massive Fed gold purchase program could echo a Depression-era effort that effectively boosted the U.S. economy.

Warren Buffett famously railed against the shiny yellow metal in 2012 when he noted all the gold in the world could be swapped for the totality of U.S. cropland and seven ExxonMobils with $1 trillion left over for “walking-around money.” His point was that these assets can generate significant returns while owning gold produces no discernable cash flow.

While this observation is certainly true, the rub is that this is not a fair comparison since gold is not an asset; rather, it should be considered an alternate currency. Pundits often describe the five factors that define “money”:

Its supply is controlled or limited,

It is fungible/uniform – this is why diamonds cannot qualify,

It is portable – this is why land cannot qualify,

It is divisible – thus art cannot be money, and

It is liquid – this means people will readily accept it in exchange.

By this definition, gold is certainly a form of money, and to Mr. Buffett’s point, one also earns no cash flow on paper dollars, euros, yen or yuan.

July 26 I Session 1 I GBIH

The document discusses potential inflation scenarios and their implications for gold prices. It analyzes the likelihood of hyperinflation, deflation, stagflation, and a return to previous low inflation levels. The author argues that stagflation, with high inflation and slowing GDP growth, poses the greatest risk and would be most positive for gold. While the Fed expects current high inflation to be temporary, money supply and debt increases make low pre-pandemic inflation unlikely. Slowing growth projections for 2022 could produce the stagflation scenario gold performs well in.

Shamik Bhose Rationale Method Of $ Decline

the possibility of dollar becoming less important and gradually being replaced as a reserve currency.

Rationale Method Of Dollar Decline

The document discusses the rationale and potential methodical decline of the US dollar as the global reserve currency. It notes that empires that hold the global reserve currency are typically net creditors, but the US has become a net debtor due to large budget and trade deficits. This makes the dollar's status vulnerable. While China has taken steps to challenge the dollar's dominance, the yuan is not ready to become a reserve currency. However, if China and others diversify reserves away from dollars over time, it could lead to a controlled, gradual decline in the dollar rather than a sudden crisis. Technical indicators also suggest monitoring support levels for signs the dollar may begin a longer-term downward trend.

Saxo Outrageous Predictions 2016

The document contains predictions from Saxo Bank analysts for the year 2016. Some of the key predictions include:

1) The Euro will rise against the US dollar to 1.23 by the end of 2016 as the US dollar peaks at the start of the Federal Reserve's expected rate hiking cycle.

2) The Russian rouble will be the best performing currency in 2016, rising 20% against the US dollar/euro basket as oil prices surge and geopolitical tensions ease.

3) Valuations of tech startups, known as unicorns, will be reduced by more than half as public markets refuse to pay inflated private market valuations, slowing venture capital funding.

4) Brazil will

2012 Outlook

My outlook for the year, written in December last year. Overly pessimistic unfortunately but with Spanish yields now over 6%, we\'re not out of the woods yet! (Pls note I did not write the China stocks or currency section.)

Gold's message & the comatose patient

The document summarizes recent movements in the stock market, bond market, commodity markets, gold, and US dollar. Stocks rallied on hopes that politicians would negotiate to end the government shutdown and raise the debt ceiling. Short-term interest rates spiked due to uncertainty around a potential US debt default. Commodity prices remained flat due to weak global growth. Gold declined further as deflationary pressures continued globally despite central bank actions. The US dollar weakened against the euro due to improving economic news in Europe and ongoing Fed stimulus.

Economic Review And Outlook

The document provides a comprehensive review and outlook of the US economy across several areas including demographics, markets, real estate, employment, and GDP. It summarizes key data and trends in each area, with some of the main points being that demographics will weigh on consumption as baby boomers retire, the housing market still faces significant headwinds from high inventory and foreclosures, unemployment remains at historically high levels across many sectors, and GDP growth is expected to be positive in the short term but a return to recession is still possible given weak underlying fundamentals.

2017 - Get Ready For An Explosive Year!

Slides for a talk at Universitas Gunadarma regarding current economic conditions (mostly US and commodities) as well as Indonesia's capital market followed by stock recommendations.

Is the us economy out of the dark woods.

Ziad Abdelnour, Lebanese American author, trader and financier is President & CEO of Blackhawk Partners, Inc., a “private family office” that backs talented operating executives in growing their companies both organically and through acquisitions and trades physical commodities.

DTC truths white paper

The document discusses how many widely held beliefs in economics and finance have been proven wrong over time. It provides examples of interest rates becoming negative, inflation being much lower than expected, and the price of oil fluctuating dramatically instead of steadily increasing. The author argues that one should be humble and flexible in their views instead of rigidly holding positions, as the financial world is always changing in ways that may contradict current assumptions. Staying open-minded and avoiding extreme portfolio positions based on specific worldviews can help investors adapt to changes.

May en lvrec

The document provides an economic outlook report from May 2011. It discusses several topics:

1) Strong corporate earnings are driving the stock market higher, though interest rates will likely rise as quantitative easing ends.

2) High food and gas prices pose a risk to consumer spending, which could slow economic growth.

3) The large and growing US national debt poses challenges, as interest payments consume a significant portion of the budget and credit rating downgrades could increase interest rates.

May en lvrec

The document provides an economic outlook report for May 2011. It discusses several topics:

1) The death of Osama bin Laden and its limited impact on markets.

2) Continued strong corporate earnings driving stock markets higher.

3) Expected changes to the Fed's monetary policy of quantitative easing later in the year which may lead to higher interest rates and a weaker stock market.

3) The US GDP growth rate slowed in the first quarter which does not bode well for reducing unemployment.

May en lvrec

The document provides an economic outlook report for May 2011. It discusses several topics:

1) The death of Osama bin Laden and its limited impact on markets.

2) Continued strong corporate earnings driving stock markets higher.

3) Expected changes to the Fed's monetary policy of quantitative easing later in the year which may lead to higher interest rates and a weaker stock market.

3) The US GDP growth rate slowed in the first quarter which does not bode well for reducing unemployment.

Ricardo V Lago -Interbank- Lima-22 04 2009

Conferencia a la alta Gerencia de Intergroup en Lima el 22 de abril , 2009 sobre perspectivas de las economias mundial y peruana y oportunidades de inversion en bolsa

Us economy goldilocks- 4th oct 2007 published in singapore times

The author's article that appeared in Business Times, Singapore on Oct 4, 2007 stated that USA Housing, low interest rates and derivatives will lead the global economy into a recession

Fasanara Capital | Investment Outlook | December 16th 2013

This document provides an investment outlook and analysis of opportunities for 2014. It maintains a strategy of being long certain equities outside the US while preparing for volatility. The US and Europe are seen as in bubble territory for stocks and credit. Japan is pursuing aggressive monetary policies that could drive further equity gains and yen weakness. China's growth is positive in the short term but credit risks loom in coming years. Corrections are anticipated, with tapering, disappointing data, or earnings declines as possible catalysts. The document recommends hedging positions and selectivity in international equities and commodities tied to China.

Can investors bet on a broad emerging markets recovery

Following the 2008 financial crisis, emerging economies rebounded. But since 2011 things have changed.

Emerging economies are now richer than ever. And while these countries still have an opportunity to grow in the future, their growth rates are likely to be slower than in the past.

As advanced economies recover and their monetary policies return to more conventional policies, further weakness in emerging markets’ equities and bond markets is expected.

Similar to The Return of Depression Economics (20)

Business Opportunities in 2016/ Investasi Tepat, Profit Hebat

Business Opportunities in 2016/ Investasi Tepat, Profit Hebat

Fasanara Capital | Investment Outlook | May 3rd 2016

Fasanara Capital | Investment Outlook | May 3rd 2016

Rumpelstiltskin at the Fed by Harley Bassman, PIMCO, executive vice presiden...

Rumpelstiltskin at the Fed by Harley Bassman, PIMCO, executive vice presiden...

Us economy goldilocks- 4th oct 2007 published in singapore times

Us economy goldilocks- 4th oct 2007 published in singapore times

Fasanara Capital | Investment Outlook | December 16th 2013

Fasanara Capital | Investment Outlook | December 16th 2013

Can investors bet on a broad emerging markets recovery

Can investors bet on a broad emerging markets recovery

More from Valbury Group Asia Division

Market outlook 2018, Peluang IPO

The document discusses the Indonesian market outlook for 2018 and opportunities for initial public offerings (IPOs) amid Indonesia's economic conditions. It notes that the market is in its fifth wave of growth since 2009 and analyzes the performance of the Jakarta Composite Index and Rupiah currency. It also examines which countries may be most impacted by rising protectionism and discusses preferred investment opportunities in real assets, commodities, and infrastructure projects. The conclusion suggests following opportunities in Asian markets in the 21st century.

Pasar Modal Sebagai Sarana Pendanaan Perusahaan & Investasi

Entrepreneurs should consider the capital markets as a fundraising platform available to them aside from bank loans.

Market Outlook (on the Indonesian Stock Market)

Presentation slides from our seminar to the students of Universitas Mercu Buana and participants of the National Stock Trading Competition

How About Gold In The Current Negative Interest Rate Era?

Gold had its best start to a year since 1980 due to supply constraints ahead. Signs are emerging of higher demand for safes as a place to store wealth with interest rates falling, showing gold is seen as a stable store of value. If the US dollar declines as expected and election surprises occur, gold could rise sharply from increased safe-haven demand, potentially reaching $6,000 to $8,300 per ounce, as it did after the Brexit vote. However, investors should not wait too long to buy during an uptrend to get the best price.

The Best Investment Opportunities for The 2nd Half of 2016

America is facing bankruptcy as debt levels continue to rise exponentially across many countries. The US dollar may weaken against other currencies in 2016. US equity markets show cautious signs, with profits dropping sharply in recent quarters. Gold prices have risen recently and central banks have been buying more gold, suggesting a new bull market may have started. Several Asian economies, particularly Indonesia, show strong growth potential and will be major drivers of global economic growth in coming decades. The presentation recommends investment in Indonesian construction, consumer, banking and balanced mutual funds to take advantage of this.

Pemilihan Saham Untuk Memperoleh Keuntungan Optimal Melalui Pendekatan Analis...

Pemilihan Saham Untuk Memperoleh Keuntungan Optimal Melalui Pendekatan Analis...Valbury Group Asia Division

Dokumen ini membahas analisis kuantitatif untuk pemilihan saham dengan menganalisis faktor-faktor ekonomi seperti pertumbuhan ekonomi, inflasi, suku bunga, dan nilai tukar mata uang; serta menganalisis hubungan antara kondisi ekonomi dengan indeks saham. Dokumen ini juga membahas strategi pemilihan saham berdasarkan fundamental yang kuat, korelasi dengan pasar, dan tingkat risiko.Market Predictions For 2016

Our analyst discusses what he considers as good investments in 2016: Gold and Oil. Find out why he vouches for these two commodities.

The Basics of Oil Trading ep. 3

The last in our crude oil training series. In these slides, see examples of case studies of chart application and read the latest crude oil market update as of December 7th, 2015.

The Basics of Oil Trading Ep. 2

Dokumen tersebut membahas tentang indikator-indikator teknikal yang digunakan dalam perdagangan minyak mentah, yaitu Moving Average, Relative Strength Index (RSI), Bollinger Bands, dan Parabolic SAR. Dokumen ini juga membahas tentang pertemuan OPEC pada 4 Desember 2015 yang dapat mempengaruhi harga minyak mentah."

The Basics of Oil Trading Episode 1

Dokumen tersebut memberikan penjelasan singkat tentang analisis teknikal berdasarkan pola harga masa lalu untuk memprediksi arah harga di masa depan, jenis-jenis chart seperti line chart, bar chart dan candlestick chart, berbagai pola candlestick seperti double top, double bottom, head and shoulders, serta faktor-faktor yang mempengaruhi pergerakan harga minyak mentah seperti penguatan dolar AS, kelebihan pasokan minyak, dan rencana pemang

Is Gold Turning?

Presentation slides for Valbury News episode 63 regarding the value of gold as an investment. Watch the video at our you tube channel, https://www.youtube.com/user/valburyresearch

Investing In the Midst of An Economic Turmoil: Opportunity or Challenge?

Investing In the Midst of An Economic Turmoil: Opportunity or Challenge? Valbury Group Asia Division

Presentation slides regarding current investing opportunities and strategies in Indonesia right now from a finance seminar at Universitas Gunadarma on October 8th. What in The World is Going on in The Oil Market?

The document discusses the benefits of exercise for mental health. Regular physical activity can help reduce anxiety and depression and improve mood and cognitive functioning. Exercise boosts blood flow, releases endorphins, and promotes changes in the brain which help regulate emotions and stress levels.

Is it time to Sell the Nikkei 225 Index & Buy The Japanese Yen?

The document discusses recent economic trends in Japan that suggest it may be time to sell stocks in the Nikkei 225 index and buy the Japanese yen. Wages have fallen to their lowest levels since 1990 in Japan while GDP contracted by 1.2% last quarter. Both the yen and Nikkei have recently reversed direction, and the Bank of Japan is running low on funds used to support the stock market. Foreign investors have also been heavily dumping Japanese stocks, suggesting more declines could be ahead if the Fed raises rates or signals tighter policy.

More from Valbury Group Asia Division (14)

Pasar Modal Sebagai Sarana Pendanaan Perusahaan & Investasi

Pasar Modal Sebagai Sarana Pendanaan Perusahaan & Investasi

How About Gold In The Current Negative Interest Rate Era?

How About Gold In The Current Negative Interest Rate Era?

The Best Investment Opportunities for The 2nd Half of 2016

The Best Investment Opportunities for The 2nd Half of 2016

Pemilihan Saham Untuk Memperoleh Keuntungan Optimal Melalui Pendekatan Analis...

Pemilihan Saham Untuk Memperoleh Keuntungan Optimal Melalui Pendekatan Analis...

Investing In the Midst of An Economic Turmoil: Opportunity or Challenge?

Investing In the Midst of An Economic Turmoil: Opportunity or Challenge?

Is it time to Sell the Nikkei 225 Index & Buy The Japanese Yen?

Is it time to Sell the Nikkei 225 Index & Buy The Japanese Yen?

Recently uploaded

一比一原版(UoB毕业证)伯明翰大学毕业证如何办理

UoB本科学位证成绩单【微信95270640】伯明翰大学没毕业>办理伯明翰大学毕业证成绩单【微信UoB】UoB毕业证成绩单UoB学历证书UoB文凭《UoB毕业套号文凭网认证伯明翰大学毕业证成绩单》《哪里买伯明翰大学毕业证文凭UoB成绩学校快递邮寄信封》《开版伯明翰大学文凭》UoB留信认证本科硕士学历认证

如果您是以下情况,我们都能竭诚为您解决实际问题:【公司采用定金+余款的付款流程,以最大化保障您的利益,让您放心无忧】

1、在校期间,因各种原因未能顺利毕业,拿不到官方毕业证+微信95270640

2、面对父母的压力,希望尽快拿到伯明翰大学伯明翰大学硕士毕业证成绩单;

3、不清楚流程以及材料该如何准备伯明翰大学伯明翰大学硕士毕业证成绩单;

4、回国时间很长,忘记办理;

5、回国马上就要找工作,办给用人单位看;

6、企事业单位必须要求办理的;

面向美国乔治城大学毕业留学生提供以下服务:

【★伯明翰大学伯明翰大学硕士毕业证成绩单毕业证、成绩单等全套材料,从防伪到印刷,从水印到钢印烫金,与学校100%相同】

【★真实使馆认证(留学人员回国证明),使馆存档可通过大使馆查询确认】

【★真实教育部认证,教育部存档,教育部留服网站可查】

【★真实留信认证,留信网入库存档,可查伯明翰大学伯明翰大学硕士毕业证成绩单】

我们从事工作十余年的有着丰富经验的业务顾问,熟悉海外各国大学的学制及教育体系,并且以挂科生解决毕业材料不全问题为基础,为客户量身定制1对1方案,未能毕业的回国留学生成功搭建回国顺利发展所需的桥梁。我们一直努力以高品质的教育为起点,以诚信、专业、高效、创新作为一切的行动宗旨,始终把“诚信为主、质量为本、客户第一”作为我们全部工作的出发点和归宿点。同时为海内外留学生提供大学毕业证购买、补办成绩单及各类分数修改等服务;归国认证方面,提供《留信网入库》申请、《国外学历学位认证》申请以及真实学籍办理等服务,帮助众多莘莘学子实现了一个又一个梦想。

专业服务,请勿犹豫联系我

如果您真实毕业回国,对于学历认证无从下手,请联系我,我们免费帮您递交

诚招代理:本公司诚聘当地代理人员,如果你有业余时间,或者你有同学朋友需要,有兴趣就请联系我

你赢我赢,共创双赢

你做代理,可以帮助伯明翰大学同学朋友

你做代理,可以拯救伯明翰大学失足青年

你做代理,可以挽救伯明翰大学一个个人才

你做代理,你将是别人人生伯明翰大学的转折点

你做代理,可以改变自己,改变他人,给他人和自己一个机会大块就啃啃得满嘴满脸猴屁股般的红艳大家一个劲地指着对方吃吃地笑瓜裂得古怪奇形怪状却丝毫不影响瓜味甜丝丝的满嘴生津遍地都是瓜横七竖八的活像掷满了一地的大石块摘走二三只爷爷是断然发现不了的即便发现爷爷也不恼反而教山娃辨认孰熟孰嫩孰甜孰淡名义上是护瓜往往在瓜棚里坐上一刻饱吃一顿后山娃就领着阿黑漫山遍野地跑阿黑是一条黑色的大猎狗挺机灵的是山娃多年的忠实伙伴平时山娃上学阿黑也摇头晃脑地跟去暑假用不着上学阿钩

2. Elemental Economics - Mineral demand.pdf

After this second you should be able to: Explain the main determinants of demand for any mineral product, and their relative importance; recognise and explain how demand for any product is likely to change with economic activity; recognise and explain the roles of technology and relative prices in influencing demand; be able to explain the differences between the rates of growth of demand for different products.

快速制作美国迈阿密大学牛津分校毕业证文凭证书英文原版一模一样

原版一模一样【微信:741003700 】【美国迈阿密大学牛津分校毕业证文凭证书】【微信:741003700 】学位证,留信认证(真实可查,永久存档)offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原海外各大学 Bachelor Diploma degree, Master Degree Diploma

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

一比一原版(UCL毕业证)伦敦大学|学院毕业证如何办理

UCL硕士学位证成绩单【微信95270640】《如何办理伦敦大学|学院毕业证认证》【办证Q微信95270640】《伦敦大学|学院文凭毕业证制作》《UCL学历学位证书哪里买》办理伦敦大学|学院学位证书扫描件、办理伦敦大学|学院雅思证书!

国际留学归国服务中心《如何办伦敦大学|学院毕业证认证》《UCL学位证书扫描件哪里买》实体公司,注册经营,行业标杆,精益求精!

专业为留学生办理伦敦大学|学院伦敦大学|学院毕业证offer【100%存档可查】留学全套申请材料办理。本公司承诺所有毕业证成绩单成品全部按照学校原版工艺对照一比一制作和学校一样的羊皮纸张保证您证书的质量!

如果你回国在学历认证方面有以下难题请联系我们我们将竭诚为你解决认证瓶颈

1所有材料真实但资料不全无法提供完全齐整的原件。【如:成绩单丶毕业证丶回国证明等材料中有遗失的。】

2获得真实的国外最终学历学位但国外本科学历就读经历存在问题或缺陷。【如:国外本科是教育部不承认的或者是联合办学项目教育部没有备案的或者外本科没有正常毕业的。】

3学分转移联合办学等情况复杂不知道怎么整理材料的。时间紧迫自己不清楚递交流程的。

如果你是以上情况之一请联系我们我们将在第一时间内给你免费咨询相关信息。我们将帮助你整理认证所需的各种材料.帮你解决国外学历认证难题。

国外伦敦大学|学院伦敦大学|学院毕业证offer办理方法:

1客户提供办理信息:姓名生日专业学位毕业时间等(如信息不确定可以咨询顾问:我们有专业老师帮你查询伦敦大学|学院伦敦大学|学院毕业证offer);

2开始安排制作伦敦大学|学院毕业证成绩单电子图;

3伦敦大学|学院毕业证成绩单电子版做好以后发送给您确认;

4伦敦大学|学院毕业证成绩单电子版您确认信息无误之后安排制作成品;

5伦敦大学|学院成品做好拍照或者视频给您确认;

6快递给客户(国内顺丰国外DHLUPS等快读邮寄)。吃吃地笑山娃很精神越逛越起劲父亲却越逛越疲倦望着父亲呵欠连天的样子山娃也说困了累了回家吧小屋闷罐一般头顶上的三叶扇彻夜呜呜作响搅得满屋热气腾腾也搅得山娃心烦意乱父亲一上床就呼呼大睡山娃却辗转反侧睡不着山娃一次又一次摸索着爬起来一遍又一遍地用暖乎乎的冷水擦身往水泥地板上一勺一勺的洒水也不知过了多久山娃竟迷迷糊糊地睡着了迷迷糊糊地又闻到了闹钟刺耳的铃声和哐咣的关门声待山娃醒来时父亲早已上班去了床头总们

SWAIAP Fraud Risk Mitigation Prof Oyedokun.pptx

SWAIAP Fraud Risk Mitigation Prof Oyedokun.pptxGodwin Emmanuel Oyedokun MBA MSc PhD FCA FCTI FCNA CFE FFAR

Lecture slide titled Fraud Risk Mitigation, Webinar Lecture Delivered at the Society for West African Internal Audit Practitioners (SWAIAP) on Wednesday, November 8, 2023.

STREETONOMICS: Exploring the Uncharted Territories of Informal Markets throug...

Delve into the world of STREETONOMICS, where a team of 7 enthusiasts embarks on a journey to understand unorganized markets. By engaging with a coffee street vendor and crafting questionnaires, this project uncovers valuable insights into consumer behavior and market dynamics in informal settings."

在线办理(GU毕业证书)美国贡萨加大学毕业证学历证书一模一样

学校原件一模一样【微信:741003700 】《(GU毕业证书)美国贡萨加大学毕业证学历证书》【微信:741003700 】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

【主营项目】

一.毕业证【q微741003700】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【q/微741003700】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

Tdasx: Unveiling the Trillion-Dollar Potential of Bitcoin DeFi

Tdasx: Unveiling the Trillion-Dollar Potential of Bitcoin DeFi

^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Duba...

Whatsapp (+971581248768) Buy Abortion Pills In Dubai/ Qatar/Kuwait/Doha/Abu Dhabi/Alain/RAK City/Satwa/Al Ain/Abortion Pills For Sale In Qatar, Doha. Abu az Zuluf. Abu Thaylah. Ad Dawhah al Jadidah. Al Arish, Al Bida ash Sharqiyah, Al Ghanim, Al Ghuwariyah, Qatari, Abu Dhabi, Dubai.. WHATSAPP +971)581248768 Abortion Pills / Cytotec Tablets Available in Dubai, Sharjah, Abudhabi, Ajman, Alain, Fujeira, Ras Al Khaima, Umm Al Quwain., UAE, buy cytotec in Dubai– Where I can buy abortion pills in Dubai,+971582071918where I can buy abortion pills in Abudhabi +971)581248768 , where I can buy abortion pills in Sharjah,+97158207191 8where I can buy abortion pills in Ajman, +971)581248768 where I can buy abortion pills in Umm al Quwain +971)581248768 , where I can buy abortion pills in Fujairah +971)581248768 , where I can buy abortion pills in Ras al Khaimah +971)581248768 , where I can buy abortion pills in Alain+971)581248768 , where I can buy abortion pills in UAE +971)581248768 we are providing cytotec 200mg abortion pill in dubai, uae.Medication abortion offers an alternative to Surgical Abortion for women in the early weeks of pregnancy. Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman Fujairah Ras Al Khaimah%^^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Dubai Abu Dhabi Sharjah Deira Ajman

Earn a passive income with prosocial investing

Invest in prosocial funds that earn you an income while improving the world

Turin Startup Ecosystem 2024 - Ricerca sulle Startup e il Sistema dell'Innov...

Turin Startup Ecosystem 2024 - Ricerca sulle Startup e il Sistema dell'Innov...Quotidiano Piemontese

Turin Startup Ecosystem 2024

Una ricerca de il Club degli Investitori, in collaborazione con ToTeM Torino Tech Map e con il supporto della ESCP Business School e di Growth CapitalAn Overview of the Prosocial dHEDGE Vault works

How the prosocial dHEDGE earns you money while saving the world!

Tax System, Behaviour, Justice, and Voluntary Compliance Culture in Nigeria -...

Tax System, Behaviour, Justice, and Voluntary Compliance Culture in Nigeria -...Godwin Emmanuel Oyedokun MBA MSc PhD FCA FCTI FCNA CFE FFAR

Lecture slide titled Tax System, Behaviour, Justice, and Voluntary Compliance Culture in Nigeria - Prof Oyedokun.pptxWhatsPump Thriving in the Whirlwind of Biden’s Crypto Roller Coaster

WhatsPump Thriving in the Whirlwind of Biden’s Crypto Roller Coaster

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

How will new technology fields affect economic trade?

Recently uploaded (20)

G20 summit held in India. Proper presentation for G20 summit

G20 summit held in India. Proper presentation for G20 summit

Tumelo-deep-dive-into-pass-through-voting-Feb23 (1).pdf

Tumelo-deep-dive-into-pass-through-voting-Feb23 (1).pdf

STREETONOMICS: Exploring the Uncharted Territories of Informal Markets throug...

STREETONOMICS: Exploring the Uncharted Territories of Informal Markets throug...

Tdasx: Unveiling the Trillion-Dollar Potential of Bitcoin DeFi

Tdasx: Unveiling the Trillion-Dollar Potential of Bitcoin DeFi

^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Duba...

^%$Zone1:+971)581248768’][* Legit & Safe #Abortion #Pills #For #Sale In #Duba...

Turin Startup Ecosystem 2024 - Ricerca sulle Startup e il Sistema dell'Innov...

Turin Startup Ecosystem 2024 - Ricerca sulle Startup e il Sistema dell'Innov...

Tax System, Behaviour, Justice, and Voluntary Compliance Culture in Nigeria -...

Tax System, Behaviour, Justice, and Voluntary Compliance Culture in Nigeria -...

WhatsPump Thriving in the Whirlwind of Biden’s Crypto Roller Coaster

WhatsPump Thriving in the Whirlwind of Biden’s Crypto Roller Coaster

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

OAT_RI_Ep20 WeighingTheRisks_May24_Trade Wars.pptx

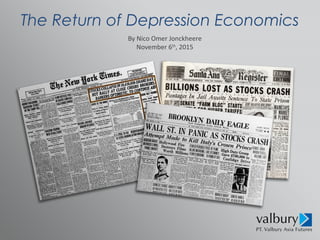

The Return of Depression Economics

- 1. The Return of Depression Economics By Nico Omer Jonckheere November 6th , 2015

- 2. Do You Know What Is The BIGGEST PROBLEM Facing The World Today?

- 3. Global debt levels have reached an astronomical $199 trillion, representing $27,200 owed for every single human on the planet.

- 4. Here is the state of debt across 47 nations – 22 advanced and 25 developing:

- 5. AMERICA is BANKRUPT and on borrowed time.

- 6. You can see from the chart above that despite the hiccup in 2008- 2009, the central planners are determined to continue inflating the GLOBAL PONZI DEBT SCHEME.

- 7. Where does this leave America and really the rest of the Western world whose data will mirror the US?

- 8. If the chart below looks INCREASINGLY EXPONENTIAL, that is not a coincidence.

- 9. China’s total debt has quadrupled from $7 trillion in 2007 to $28 trillion in the middle of last year…