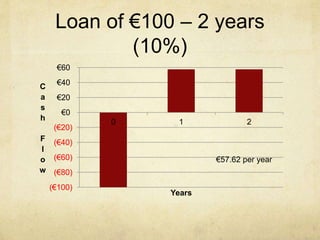

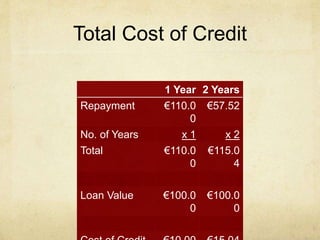

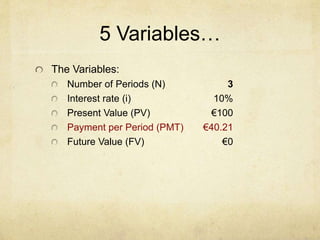

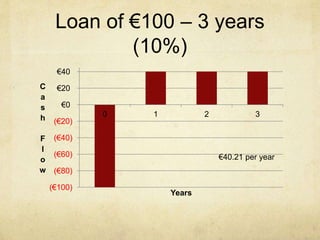

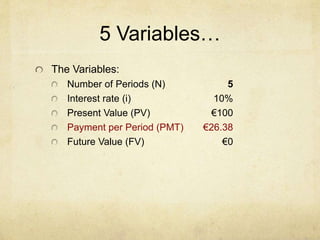

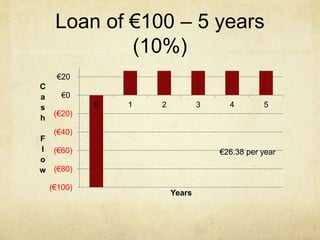

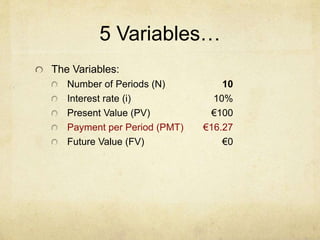

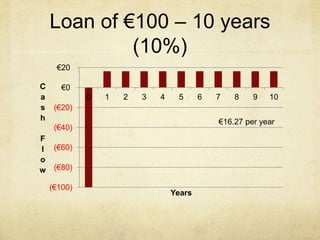

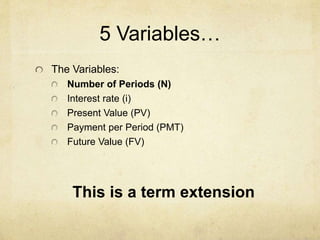

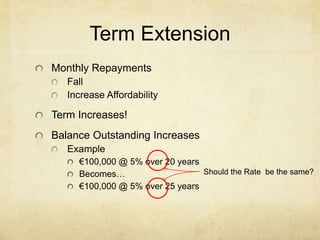

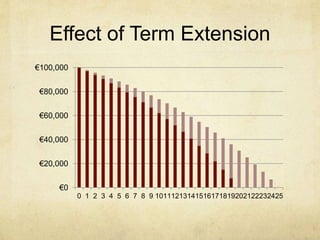

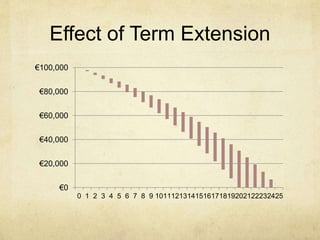

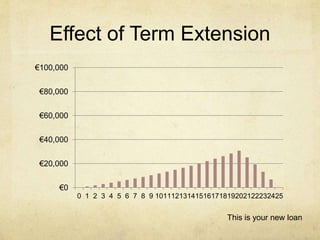

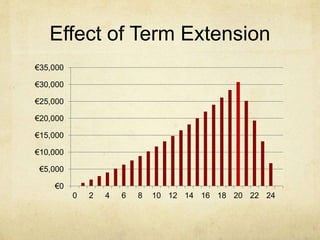

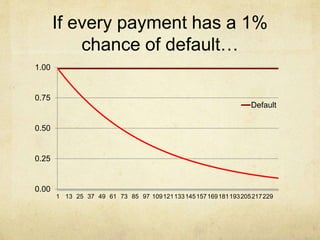

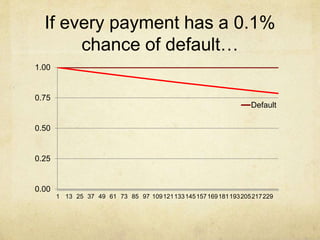

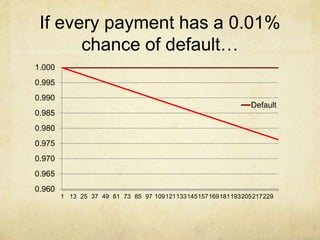

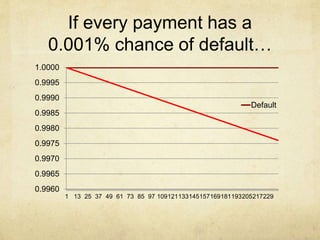

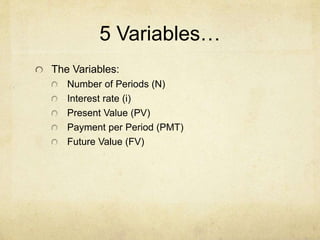

This document provides an introduction to quantification tools for loan restructuring. It discusses topics such as the CAMPARI framework for credit analysis, the 5 Cs and 5 variables used to analyze loans, and how compounding interest, risk, and term extensions impact the total cost of credit. Quantitative examples are provided to illustrate concepts like how increasing the loan term reduces monthly payments but increases the total interest paid over the life of the loan.

![[Financial Calculator]](https://image.slidesharecdn.com/566cd327-09af-46c1-97b3-aaca9f176f51-151117115218-lva1-app6891/85/The-Quantification-of-Loan-Restructuring-11-320.jpg)