The Labor Market Situation September 11, 2013

•

1 like•721 views

The Labor Market Situation September 11, 2013 Dr. Jennifer Hunt, Chief Economist, U.S. Department of Labor

Report

Share

Report

Share

Download to read offline

Recommended

June Jobs Report - U.S. Department of the Treasury

Private sector employment increased by 262,000 jobs in June, the fifth consecutive month exceeding 200,000 jobs added. The unemployment rate fell to 6.1% from 6.3% in May. While most sectors saw employment growth, the growth was entirely in part-time jobs, with part-time employment up 799,000 and full-time employment down 523,000. The report signals ongoing steady job growth, but more growth is still needed to continue lowering unemployment rates.

Business forward 130805v1

The US labor market saw steady job growth in July with 161,000 new jobs added. Over the past year, employment has increased by over 2 million jobs. While the unemployment rate has been steadily declining since 2009, some industries like manufacturing have not recovered to pre-recession employment levels despite increases in output. Retail trade led job growth in July and auto sales have returned to pre-recession volumes, helping employment in the auto industry.

Dr. Jennifer Hunt of the Department of Labor discusses November jobs numbers

The US labor market saw decent growth in November despite the government shutdown and debt ceiling issues earlier in the fall. Nonfarm payrolls grew by 196,000 in November, unemployment dropped to 7.0%, and revisions showed stronger growth over the past few months. While labor force participation only partially rebounded, employment and unemployment rates returned to pre-shutdown levels. The report suggests the economy had more momentum than previously believed in the third quarter. Extending unemployment benefits would help millions of families and support continued economic growth.

Us econ ppt lynchburg 3-4-2011 final_dr.shea

The U.S. economy is recovering slowly with decent GDP growth and a slowly improving labor market, though unemployment remains high. Inflation remains low despite rising commodity prices. Recent forecasts point to accelerating growth in 2011 of around 3.5%. Some data signals like consumer confidence are encouraging, but other data like durable goods orders have been weak. Housing prices continue to decline due to excess supply, which could dampen consumer spending. Upside risks include normal cyclical dynamics boosting growth, while downside risks include higher oil prices and fiscal austerity measures dampening growth.

Economy on the rebound, to pick pace in q2 government

some Indian economy dependent on government decision and this decision give high number of growth in display.in this ppt economy rebound it means economy going high as much assumption.

Activity 4.4

The document discusses Gross Domestic Product (GDP) in Mexico. It notes that GDP is the value of all final goods and services produced in an economy in one year. GDP in Mexico has been increasing due to population growth, growth in capital equipment, and advances in technology. Mexico's GDP grew 0.7% in the last quarter of 2016 compared to the previous quarter. While Mexico has the 14th largest economy based on GDP, it ranks 81st based on GDP per capita. The document also discusses GDP figures and forecasts for Mexico's economic growth in 2017 and 2018.

Daily Economic Update for August 2, 2010

The manufacturing sector continues to grow with improvements in inventories, exports, supplier deliveries and employment. The ISM Manufacturing Index remained above 50, signaling expansion, though it declined slightly from the prior month. Construction spending posted a small increase in June led by growth in public and commercial building, but overall construction spending remains 8% below last year's level.

Economic Review 2015-11

The document summarizes recent economic data from the UK. It notes that GDP growth slowed to 0.5% in the third quarter of 2015, with services growth remaining strong but manufacturing and construction declining. Unemployment has fallen to 5.4%, its lowest since 2008, with reductions across age groups and durations of unemployment. Average weekly earnings grew 2.8% in the latest period, with private sector pay growth stronger than public sector. Real earnings growth has picked up from post-downturn lows but remains below pre-2008 levels in most industries.

Recommended

June Jobs Report - U.S. Department of the Treasury

Private sector employment increased by 262,000 jobs in June, the fifth consecutive month exceeding 200,000 jobs added. The unemployment rate fell to 6.1% from 6.3% in May. While most sectors saw employment growth, the growth was entirely in part-time jobs, with part-time employment up 799,000 and full-time employment down 523,000. The report signals ongoing steady job growth, but more growth is still needed to continue lowering unemployment rates.

Business forward 130805v1

The US labor market saw steady job growth in July with 161,000 new jobs added. Over the past year, employment has increased by over 2 million jobs. While the unemployment rate has been steadily declining since 2009, some industries like manufacturing have not recovered to pre-recession employment levels despite increases in output. Retail trade led job growth in July and auto sales have returned to pre-recession volumes, helping employment in the auto industry.

Dr. Jennifer Hunt of the Department of Labor discusses November jobs numbers

The US labor market saw decent growth in November despite the government shutdown and debt ceiling issues earlier in the fall. Nonfarm payrolls grew by 196,000 in November, unemployment dropped to 7.0%, and revisions showed stronger growth over the past few months. While labor force participation only partially rebounded, employment and unemployment rates returned to pre-shutdown levels. The report suggests the economy had more momentum than previously believed in the third quarter. Extending unemployment benefits would help millions of families and support continued economic growth.

Us econ ppt lynchburg 3-4-2011 final_dr.shea

The U.S. economy is recovering slowly with decent GDP growth and a slowly improving labor market, though unemployment remains high. Inflation remains low despite rising commodity prices. Recent forecasts point to accelerating growth in 2011 of around 3.5%. Some data signals like consumer confidence are encouraging, but other data like durable goods orders have been weak. Housing prices continue to decline due to excess supply, which could dampen consumer spending. Upside risks include normal cyclical dynamics boosting growth, while downside risks include higher oil prices and fiscal austerity measures dampening growth.

Economy on the rebound, to pick pace in q2 government

some Indian economy dependent on government decision and this decision give high number of growth in display.in this ppt economy rebound it means economy going high as much assumption.

Activity 4.4

The document discusses Gross Domestic Product (GDP) in Mexico. It notes that GDP is the value of all final goods and services produced in an economy in one year. GDP in Mexico has been increasing due to population growth, growth in capital equipment, and advances in technology. Mexico's GDP grew 0.7% in the last quarter of 2016 compared to the previous quarter. While Mexico has the 14th largest economy based on GDP, it ranks 81st based on GDP per capita. The document also discusses GDP figures and forecasts for Mexico's economic growth in 2017 and 2018.

Daily Economic Update for August 2, 2010

The manufacturing sector continues to grow with improvements in inventories, exports, supplier deliveries and employment. The ISM Manufacturing Index remained above 50, signaling expansion, though it declined slightly from the prior month. Construction spending posted a small increase in June led by growth in public and commercial building, but overall construction spending remains 8% below last year's level.

Economic Review 2015-11

The document summarizes recent economic data from the UK. It notes that GDP growth slowed to 0.5% in the third quarter of 2015, with services growth remaining strong but manufacturing and construction declining. Unemployment has fallen to 5.4%, its lowest since 2008, with reductions across age groups and durations of unemployment. Average weekly earnings grew 2.8% in the latest period, with private sector pay growth stronger than public sector. Real earnings growth has picked up from post-downturn lows but remains below pre-2008 levels in most industries.

Treasury response to economy emerging from recession

The National Treasury would like to welcome the second quarter Gross Domestic Product (GDP) data, which showed a rebound in economic growth to 2.5% (seasonally adjusted annual rate).

Daily Economic Update for November 1, 2010

Personal incomes and consumer spending grew slightly in September. The ISM manufacturing index rose to 56.9 in October, indicating expansion, driven by increases in new orders, production, and employment. Construction spending increased 0.5% from August to September, with residential construction rising the most at 1.8%. While income growth remains slow, demand for goods and manufacturing employment are positive signs for the labor market and sustained economic recovery.

Economic Update- March 2015

1. The US economy grew at an annual rate of 2.2% in the fourth quarter of 2014, driven by strong growth in consumer spending.

2. The unemployment rate fell to 5.5% in February 2015, near the Federal Reserve's estimate of full employment, however labor force participation remains low at 62.8%.

3. Hiring continued at a strong pace in February with 295,000 new jobs added, however wage growth remained slow at 2% annually and temporary employment declined.

Complete Mismanagement of Economy

India's economic growth has slowed down sharply . In the past 3 Years, the BJP Govt. does not have the faintest idea

of how to stop slide of the Economy.

Economic Indicators September 2013

The document provides an economic outlook overview for September 2013. Key points include:

- GDP growth forecasts improved slightly for the Eurozone, US, and Japan. Recent data also indicates the Eurozone recovery is being maintained.

- Several economic indicators show improvements, such as industrial confidence and consumer confidence rising in the Eurozone. The IFO Business Climate Index for Germany also continued to climb.

- Global ad expenditure is forecast to grow at a slower 3.5% in 2013 due to issues in Europe and South Korea, but a rebound is expected in 2014-2015, led by rising markets. Internet and mobile advertising are outpacing other media in growth.

Economic Indicators August 2013

The document provides an overview of recent economic indicators from Europe, the US, Japan, and Germany. It summarizes that GDP growth forecasts for Europe and the US were slightly lowered, while forecasts for Japan remained unchanged. Several economic indicators for Europe showed improvements, including industrial confidence, consumer confidence, and GDP, pointing to a cautious recovery. The German IFO index rose for the third month in a row, with firms remaining cautiously optimistic.

Economic Review 2015-12

- GDP growth in the UK has slowed slightly in 2015 compared to 2014, with quarterly growth of 0.5% in Q3 2015. Private consumption and investment have remained robust drivers of growth.

- Annual inflation has remained close to zero for most of 2015, driven by falling goods prices, while services inflation has remained around 2.5%.

- The UK labor market continues to strengthen, with record high employment, falling unemployment, and a declining inactivity rate, indicating further tightening in the labor market.

Economic Indicators and Monthly Overview October 2015

The document summarizes economic indicators and forecasts from Europe, the US, and Japan in October 2015. In Europe, GDP growth forecasts remained stable for 2015 but declined slightly for 2016, and industrial confidence increased slightly while consumer confidence declined. In the US, GDP forecasts remained the same for 2015 but declined slightly for 2016. Japan's GDP forecasts declined for both 2015 and 2016, and its credit rating was downgraded. The document also includes charts and data on topics like GDP, inflation, unemployment, and business climate indexes for various countries and regions.

Economic Review 2016-01

1) GDP growth in the UK slowed to 0.4% in Q3 2015, down from a previous estimate of 0.5%, with growth averaging 0.5% in the first three quarters of 2015.

2) Household consumption has been the main driver of GDP growth over the past year, while net trade and private housing investment have dragged on growth.

3) The UK's household saving ratio fell to 4.4% in Q3 2015, its lowest level since early 2010, as consumption growth has outpaced income growth in recent years.

Economic Indicators and Monthly Overview August 2015

The document provides an overview of recent economic indicators from Europe, the US, Japan, and Germany. It summarizes GDP forecasts, inflation rates, unemployment, industrial and consumer confidence indexes, and capacity utilization in the EU. Charts show trends in these indicators. The report also provides data on business climate indexes in Germany and worldwide from IFO and advertising expenditure forecasts from ZenithOptimedia.

Economic Indicators and Monthly Overview April 2015

The document provides an overview of recent economic indicators from Europe, the US, Japan, and globally. Key points include:

- GDP growth forecasts for Europe and Germany improved slightly, while forecasts declined for the US and Japan.

- Industrial confidence in the Eurozone rose again in March, and consumer confidence continued to improve significantly.

- Unemployment rates and inflation rates in the Eurozone are trending downward.

- The IFO Business Climate Index for Germany reached its highest level since July 2014, indicating continued economic expansion.

Employment and Job Market for Canada - March 2016

This presentation will discuss the employment and job market for Canada. The following are the areas of focus:

1. Manufacturing

2. Natural Resources

3. Retail and Wholesale Trade

4. Government jobs

5. Economic Growth

6. Infrastructure Spending

7. Social program spending

8. Power Generation

9. Economic Stimulus

10. Capital Investment

Economic Indicators and Montly Overview September

The document provides an overview of recent economic indicators from Europe, the US, Japan and Germany. It summarizes data on GDP growth, unemployment, inflation, business and consumer confidence indexes. GDP growth forecasts for Europe in 2014 were lowered slightly due to stagnation in the Eurozone recovery. US GDP growth forecasts remained unchanged, while Japan's forecasts saw a small decrease and increase for 2014 and 2015 respectively. Several indexes tracking European industrial and consumer confidence declined further in August.

Economic Survey of India 2008

The Economic Survey of India is published annually by the Central Statistical Organization to provide an overview of the country's economic performance. It analyzes developments in key macroeconomic and microeconomic sectors using statistical data. The 2008-09 survey highlighted that economic growth slowed to 6.7% from 9% the previous year. The fiscal deficit also increased significantly. It provided recommendations such as tax reforms, increasing foreign investment limits, deregulating several industries, and subsidy reforms to restore economic growth.

HRF Centre Hunter Economic Update March 2019

HRF Centre Hunter Economic Update March 2019Hunter Research Foundation Centre (HRFC) University of Newcastle

Half yearly review of the Hunter economy including local and national insights presented at our March 2019 business breakfast in NewcastleEconomic Indicators and Monthly Overview June 2015

The document provides an overview of recent economic indicators from Europe, the US, Japan, and Germany. It summarizes that GDP growth in the EU remained stable in 2015 but declined in the US due to harsh weather and a strong dollar. Industrial confidence in the EU improved slightly while consumer confidence declined. The German economy remains on track with recent data showing accelerated growth, though the IFO Business Climate Index edged downward.

Economic indicators october

This document provides an economic overview and indicators for Europe, the US, Japan, and Germany from October 2014. It summarizes that GDP growth forecasts were lowered slightly for Europe and Japan, while the US forecast improved slightly. Industrial confidence and consumer confidence in Europe continued to decline in September. The German IFO Business Climate Index fell again, indicating the German economy is slowing. Charts show trends in GDP, inflation, unemployment, and other economic indicators for various regions.

Handling Data in AS and A2 Economics

This document provides guidance on summarizing economic data presented in charts and tables for AS and A2 economics exams. It includes examples of summarizing key features of data on UK migration trends, world copper prices, and oil prices. It also demonstrates calculating an index number and explaining causes of trends based on extracted information. The document offers tips for confidently handling different data presentations and accurately describing economic concepts shown in the data.

Economic indicators May 2013

The document provides an overview of recent economic indicators from Europe, the US, and Japan in June 2013. In Europe, GDP forecasts remained stable but consumer and business confidence improved slightly. German business confidence rose after declines, and the economy remains on track. US growth prospects are uncertain due to slowing indicators and fiscal issues. Japan's GDP growth forecast improved considerably. The document also summarizes recent advertising expenditure forecasts from Zenith, predicting a return to growth in major markets in 2013.

Economic Indicators February 2014

The document provides an overview of recent economic indicators from Europe, the US, Japan and Germany. It summarizes GDP forecasts, inflation rates, unemployment, consumer confidence indexes and other metrics. According to the document, GDP growth is expected to improve in the US and Eurozone in 2014, while Japan's GDP forecast was lowered slightly. Inflation remains a concern in the Eurozone. The German economy started 2014 promisingly with rising business sentiment indicators.

Konjunktur und Kapitalmarktausblick 2012 des Erste Group Research Präsentati...

Konjunktur und Kapitalmarktausblick 2012 des Erste Group Research Präsentati...NEWSROOM für Unternehmer

Für 2012 erwartet das Erste Group Research eine Fortsetzung des langsamen Lösungsprozesses der Staatsverschuldungskrise. Weitere Eskalationen, gefolgt von weiteren Maßnahmen – insbesondere Ausweitung der Finanzierungsunterstützung – scheinen absehbar zu sein. Die Analysten erwarten keinen Durchbruch, aber auch kein Auseinanderbrechen der Eurozone. Insgesamt deuten alle Zeichen auf ein „hindurchstolpern“ der Eurozone 2012 hin. Ab 2013 wird wieder Wachstum mit 1,2% erwartet. July 2015 Chicago Employment Update

Employment increased by 23,000 jobs so the expanding labor force only increased the overall unemployment rate by 30 basis points to 6.3 percent. This is the second consecutive month when unemployment increased.

More Related Content

What's hot

Treasury response to economy emerging from recession

The National Treasury would like to welcome the second quarter Gross Domestic Product (GDP) data, which showed a rebound in economic growth to 2.5% (seasonally adjusted annual rate).

Daily Economic Update for November 1, 2010

Personal incomes and consumer spending grew slightly in September. The ISM manufacturing index rose to 56.9 in October, indicating expansion, driven by increases in new orders, production, and employment. Construction spending increased 0.5% from August to September, with residential construction rising the most at 1.8%. While income growth remains slow, demand for goods and manufacturing employment are positive signs for the labor market and sustained economic recovery.

Economic Update- March 2015

1. The US economy grew at an annual rate of 2.2% in the fourth quarter of 2014, driven by strong growth in consumer spending.

2. The unemployment rate fell to 5.5% in February 2015, near the Federal Reserve's estimate of full employment, however labor force participation remains low at 62.8%.

3. Hiring continued at a strong pace in February with 295,000 new jobs added, however wage growth remained slow at 2% annually and temporary employment declined.

Complete Mismanagement of Economy

India's economic growth has slowed down sharply . In the past 3 Years, the BJP Govt. does not have the faintest idea

of how to stop slide of the Economy.

Economic Indicators September 2013

The document provides an economic outlook overview for September 2013. Key points include:

- GDP growth forecasts improved slightly for the Eurozone, US, and Japan. Recent data also indicates the Eurozone recovery is being maintained.

- Several economic indicators show improvements, such as industrial confidence and consumer confidence rising in the Eurozone. The IFO Business Climate Index for Germany also continued to climb.

- Global ad expenditure is forecast to grow at a slower 3.5% in 2013 due to issues in Europe and South Korea, but a rebound is expected in 2014-2015, led by rising markets. Internet and mobile advertising are outpacing other media in growth.

Economic Indicators August 2013

The document provides an overview of recent economic indicators from Europe, the US, Japan, and Germany. It summarizes that GDP growth forecasts for Europe and the US were slightly lowered, while forecasts for Japan remained unchanged. Several economic indicators for Europe showed improvements, including industrial confidence, consumer confidence, and GDP, pointing to a cautious recovery. The German IFO index rose for the third month in a row, with firms remaining cautiously optimistic.

Economic Review 2015-12

- GDP growth in the UK has slowed slightly in 2015 compared to 2014, with quarterly growth of 0.5% in Q3 2015. Private consumption and investment have remained robust drivers of growth.

- Annual inflation has remained close to zero for most of 2015, driven by falling goods prices, while services inflation has remained around 2.5%.

- The UK labor market continues to strengthen, with record high employment, falling unemployment, and a declining inactivity rate, indicating further tightening in the labor market.

Economic Indicators and Monthly Overview October 2015

The document summarizes economic indicators and forecasts from Europe, the US, and Japan in October 2015. In Europe, GDP growth forecasts remained stable for 2015 but declined slightly for 2016, and industrial confidence increased slightly while consumer confidence declined. In the US, GDP forecasts remained the same for 2015 but declined slightly for 2016. Japan's GDP forecasts declined for both 2015 and 2016, and its credit rating was downgraded. The document also includes charts and data on topics like GDP, inflation, unemployment, and business climate indexes for various countries and regions.

Economic Review 2016-01

1) GDP growth in the UK slowed to 0.4% in Q3 2015, down from a previous estimate of 0.5%, with growth averaging 0.5% in the first three quarters of 2015.

2) Household consumption has been the main driver of GDP growth over the past year, while net trade and private housing investment have dragged on growth.

3) The UK's household saving ratio fell to 4.4% in Q3 2015, its lowest level since early 2010, as consumption growth has outpaced income growth in recent years.

Economic Indicators and Monthly Overview August 2015

The document provides an overview of recent economic indicators from Europe, the US, Japan, and Germany. It summarizes GDP forecasts, inflation rates, unemployment, industrial and consumer confidence indexes, and capacity utilization in the EU. Charts show trends in these indicators. The report also provides data on business climate indexes in Germany and worldwide from IFO and advertising expenditure forecasts from ZenithOptimedia.

Economic Indicators and Monthly Overview April 2015

The document provides an overview of recent economic indicators from Europe, the US, Japan, and globally. Key points include:

- GDP growth forecasts for Europe and Germany improved slightly, while forecasts declined for the US and Japan.

- Industrial confidence in the Eurozone rose again in March, and consumer confidence continued to improve significantly.

- Unemployment rates and inflation rates in the Eurozone are trending downward.

- The IFO Business Climate Index for Germany reached its highest level since July 2014, indicating continued economic expansion.

Employment and Job Market for Canada - March 2016

This presentation will discuss the employment and job market for Canada. The following are the areas of focus:

1. Manufacturing

2. Natural Resources

3. Retail and Wholesale Trade

4. Government jobs

5. Economic Growth

6. Infrastructure Spending

7. Social program spending

8. Power Generation

9. Economic Stimulus

10. Capital Investment

Economic Indicators and Montly Overview September

The document provides an overview of recent economic indicators from Europe, the US, Japan and Germany. It summarizes data on GDP growth, unemployment, inflation, business and consumer confidence indexes. GDP growth forecasts for Europe in 2014 were lowered slightly due to stagnation in the Eurozone recovery. US GDP growth forecasts remained unchanged, while Japan's forecasts saw a small decrease and increase for 2014 and 2015 respectively. Several indexes tracking European industrial and consumer confidence declined further in August.

Economic Survey of India 2008

The Economic Survey of India is published annually by the Central Statistical Organization to provide an overview of the country's economic performance. It analyzes developments in key macroeconomic and microeconomic sectors using statistical data. The 2008-09 survey highlighted that economic growth slowed to 6.7% from 9% the previous year. The fiscal deficit also increased significantly. It provided recommendations such as tax reforms, increasing foreign investment limits, deregulating several industries, and subsidy reforms to restore economic growth.

HRF Centre Hunter Economic Update March 2019

HRF Centre Hunter Economic Update March 2019Hunter Research Foundation Centre (HRFC) University of Newcastle

Half yearly review of the Hunter economy including local and national insights presented at our March 2019 business breakfast in NewcastleEconomic Indicators and Monthly Overview June 2015

The document provides an overview of recent economic indicators from Europe, the US, Japan, and Germany. It summarizes that GDP growth in the EU remained stable in 2015 but declined in the US due to harsh weather and a strong dollar. Industrial confidence in the EU improved slightly while consumer confidence declined. The German economy remains on track with recent data showing accelerated growth, though the IFO Business Climate Index edged downward.

Economic indicators october

This document provides an economic overview and indicators for Europe, the US, Japan, and Germany from October 2014. It summarizes that GDP growth forecasts were lowered slightly for Europe and Japan, while the US forecast improved slightly. Industrial confidence and consumer confidence in Europe continued to decline in September. The German IFO Business Climate Index fell again, indicating the German economy is slowing. Charts show trends in GDP, inflation, unemployment, and other economic indicators for various regions.

Handling Data in AS and A2 Economics

This document provides guidance on summarizing economic data presented in charts and tables for AS and A2 economics exams. It includes examples of summarizing key features of data on UK migration trends, world copper prices, and oil prices. It also demonstrates calculating an index number and explaining causes of trends based on extracted information. The document offers tips for confidently handling different data presentations and accurately describing economic concepts shown in the data.

Economic indicators May 2013

The document provides an overview of recent economic indicators from Europe, the US, and Japan in June 2013. In Europe, GDP forecasts remained stable but consumer and business confidence improved slightly. German business confidence rose after declines, and the economy remains on track. US growth prospects are uncertain due to slowing indicators and fiscal issues. Japan's GDP growth forecast improved considerably. The document also summarizes recent advertising expenditure forecasts from Zenith, predicting a return to growth in major markets in 2013.

Economic Indicators February 2014

The document provides an overview of recent economic indicators from Europe, the US, Japan and Germany. It summarizes GDP forecasts, inflation rates, unemployment, consumer confidence indexes and other metrics. According to the document, GDP growth is expected to improve in the US and Eurozone in 2014, while Japan's GDP forecast was lowered slightly. Inflation remains a concern in the Eurozone. The German economy started 2014 promisingly with rising business sentiment indicators.

What's hot (20)

Treasury response to economy emerging from recession

Treasury response to economy emerging from recession

Economic Indicators and Monthly Overview October 2015

Economic Indicators and Monthly Overview October 2015

Economic Indicators and Monthly Overview August 2015

Economic Indicators and Monthly Overview August 2015

Economic Indicators and Monthly Overview April 2015

Economic Indicators and Monthly Overview April 2015

Economic Indicators and Monthly Overview June 2015

Economic Indicators and Monthly Overview June 2015

Viewers also liked

Konjunktur und Kapitalmarktausblick 2012 des Erste Group Research Präsentati...

Konjunktur und Kapitalmarktausblick 2012 des Erste Group Research Präsentati...NEWSROOM für Unternehmer

Für 2012 erwartet das Erste Group Research eine Fortsetzung des langsamen Lösungsprozesses der Staatsverschuldungskrise. Weitere Eskalationen, gefolgt von weiteren Maßnahmen – insbesondere Ausweitung der Finanzierungsunterstützung – scheinen absehbar zu sein. Die Analysten erwarten keinen Durchbruch, aber auch kein Auseinanderbrechen der Eurozone. Insgesamt deuten alle Zeichen auf ein „hindurchstolpern“ der Eurozone 2012 hin. Ab 2013 wird wieder Wachstum mit 1,2% erwartet. July 2015 Chicago Employment Update

Employment increased by 23,000 jobs so the expanding labor force only increased the overall unemployment rate by 30 basis points to 6.3 percent. This is the second consecutive month when unemployment increased.

Weltfrauentag 2016: Finanzielle Abhängigkeiten schwinden nur langsam

Knapp drei Viertel der Frauen können ihren Lebensstandard alleine nicht sichern. Doch obwohl Frauen weniger verdienen, ist der monatliche Sparbetrag der weiblichen Bevölkerung in den letzten 2 Jahren gestiegen. Die Erste Bank stellt anlässlich des Frauentages eine repräsentative IMAS-Studie vor.

Österreichs Geschäftsführer verdienen im Schnitt 292.000 Euro

Je höher der Mitarbeiter in der Unternehmenshierarchie angesiedelt ist, desto negativer entwickelt sich seine Vergütung, heißt es im Kienbaum Vergütungsreport Österreich 2015 . Die jährliche Gesamtvergütung inklusive Boni ist laut Studie bei Geschäftsführern und Bereichsleitern im Vergleich zum Vorjahr um rund zwei Prozent gesunken. Trotz der Gehaltseinbußen sind Geschäftsführer immer noch Spitzenverdiener: Sie erhalten ein durchschnittliches Jahresgehalt von 292.000 Euro. Bereichsleiter verdienen im Schnitt 179.000 Euro, Abteilungsleiter 119.000 Euro und Teamleiter 87.000 Euro.

Wohnstudie 2016: Wieso Wohnen für junge Menschen kaum noch leistbar ist

Die steigenden Immobilen und Mietpreise machen den ÖsterreicherInnen zu schaffen: Mehr als die Hälfte der Studierenden kann sich kein eigenes zu Hause leisten, bei den jungen Erwachsenen sind es 23%. Gesellschaftlich elementare Grundbedürfnisse können bald nicht mehr gedeckt werden.

Das sind Österreichs wertvollste Marken 2016

Red Bulls Markenwert stieg 2016 um zwei Prozent auf 15,11 Mrd. Euro. Wachstumsmeister war aber das zweitplatzierte Swarovski mit einem Plus von 5,3 Prozent auf 3,44 Mrd. Euro. Auf Red Bull entfiel fast die Hälfte des Markenwertes der Top 10 Österreichischen Unternehmen (32 Mrd. Euro). Unter den Top 5 Unternehmen waren auch Novomatic, Spar, ÖBB.

KMU-Ideen-Nacht: Inspiration für neue Wege

Die Eventserie „KMU-Ideen-Nacht“ der Erste Bank Österreich

bringt die großen Veränderungen zu den klein(st)en

Unternehmen und zeigt, wie sich weltweit fast alle Branchen

komplett neu erfinden. Success-Stories wollenb Nachahmer finden.

Welche Firmenwagen wählen Manager in Österreich und Deutschland

In Österreich sind die Unternehmen noch weit von einem „grünen“ Fuhrpark entfernt, haben aber schon etwas mehr in diese Richtung unternommen als deutsche Firmen: 47 Prozent können sich vorstellen, Fahrzeuge mit alternativem Antrieb anzuschaffen, 14 Prozent haben sie bereits in ihrer Firmenwagenflotte und 20 Prozent haben dies konkret geplant. Das sind die Ergebnisse einer Kienbaum-Umfrage – eine Kooperation zwischen Kienbaum Beratungen GmbH und dem Forum Personal des ÖPWZ, unter 246 österreichischen Firmen, deren Angaben in den „Firmenwagenreport 2016 - Österreich“ eingeflossen sind.

Viewers also liked (8)

Konjunktur und Kapitalmarktausblick 2012 des Erste Group Research Präsentati...

Konjunktur und Kapitalmarktausblick 2012 des Erste Group Research Präsentati...

Weltfrauentag 2016: Finanzielle Abhängigkeiten schwinden nur langsam

Weltfrauentag 2016: Finanzielle Abhängigkeiten schwinden nur langsam

Österreichs Geschäftsführer verdienen im Schnitt 292.000 Euro

Österreichs Geschäftsführer verdienen im Schnitt 292.000 Euro

Wohnstudie 2016: Wieso Wohnen für junge Menschen kaum noch leistbar ist

Wohnstudie 2016: Wieso Wohnen für junge Menschen kaum noch leistbar ist

Welche Firmenwagen wählen Manager in Österreich und Deutschland

Welche Firmenwagen wählen Manager in Österreich und Deutschland

Similar to The Labor Market Situation September 11, 2013

Business forward 130708v1

The document summarizes the key points from Dr. Jennifer Hunt's analysis of the July 2013 US labor market situation:

- Job growth has been steady since February 2010, with 202,000 jobs added in June 2013. Over the past year, 2.35 million jobs have been added.

- The unemployment rate has been steadily declining since the end of 2009.

- Leisure and hospitality led job growth in June 2013.

- Many industries have not recovered the jobs lost since the recession ended.

- The share of long-term unemployed Americans is falling.

Hiring Trends - Webinar with the Department of Labor and Business Forward

Dr. Heidi Shierholz, chief economist at the U.S. Department of Labor discusses the latest and trends in hiring and job opening. She talks about the Job Openings and Labor Turnover Survey (JOLTS), which was released earlier that day.

CBIZ Small Business Employment Index - June 2012

The CBIZ Small Business Employment Index (SBEI), a barometer for hiring trends among companies with 300 or fewer employees,

increased by 1.38 percent during June, following an increase of 1.34 percent in May. The SBEI’s gain reflects a continued strengthening

in growth in small business employment and contrasts recent weakening reports from the private sector.

DCR Workforce June 2013 Trendline Report

The document discusses a new OSHA initiative to increase protections for temporary workers. It was prompted by several temporary worker deaths in the past year. The initiative requires staffing firms and client companies to ensure temporary workers have a safe workplace and necessary safety training. Both entities may now be held liable for violations. Research shows temporary workers have higher injury risks due to lack of safety training and some employers view them as expendable. The initiative aims to address this issue and protect temporary worker safety.

DCR Trendline December 2013 – Contingent Worker Forecast and Supply Report

Welcome to the final month of 2013! The staff at TrendLine is pleased to be wrapping up our first full year of publication. It’s been an exciting year in the world of the contingent workforce. In our last issue of 2013 we once again provide you with key insights into the temporary staffing industry. Our thorough research into pivotal trends and current events, along with our in-depth analysis of contingent worker supply and demand, is designed to give you a pulse of the market.

Inside This Issue:

- DCR National Temp Wage Index

- Post Shutdown Impact and Recovery

- OSHA Asked to Further Improve Temp Worker Protections

- TrendLine in 2013

- A Look Back at 2013: Sector By Sector

R42063

This document discusses the relationship between economic growth and unemployment rates. It finds that a persistently high unemployment rate remains a concern for Congress. While the unemployment rate has declined since peaking in 2009 and 2010, it remains elevated by historical standards. The key driver of unemployment over the long run is the rate of economic growth compared to potential growth. For unemployment to significantly decline, growth needs to outpace the combined growth of the labor force and productivity. Recent recoveries, including from the 2007-2009 recession, have seen slow declines in unemployment, described as "jobless recoveries."

JUNE 4 final

This document provides an economic analysis and overview of a diversified portfolio for the years 2013-2015. It summarizes GDP, employment, real estate, government spending, interest rates, and stocks for 2013. GDP grew 2.2% in 2013, driven by personal consumption and residential investment. The unemployment rate fell to 6.7% as hiring improved but wages remained stagnant. Real estate rebounded with home sales and prices rising. Government spending declined as the deficit fell but austerity measures hampered growth. Interest rates remained low as the Fed began tapering quantitative easing. Stocks performed well overall in 2013.

May 2013 Workplace Economy

165,000 new jobs were added in April according to the BLS report, exceeding economists' projections. The unemployment rate dropped to 7.5%, its lowest point since 2008. Several sectors added jobs including finance (9,000), healthcare (19,000), leisure and hospitality (43,000), professional and business services (73,000), retail trade (29,300) and temporary help services (30,800). The positive jobs report eased fears of an economic slowdown in the U.S.

Steven Jagger UK Jobs report October. Candidate Shortage

Candidate availability continues to fall sharply. The rate of decline in permanent staff availability was marked, despite easing slightly to the slowest since May, while temp availability decreased at the fastest pace in three months.

Jobs report sep13

The August 2013 jobs report showed mixed results. While 169,000 jobs were added and the unemployment rate fell slightly to 7.3%, the civilian labor force declined by 312,000. Some economists believe this caused the drop in unemployment. Private sector jobs increased by 152,000 led by gains in professional and business services and temporary help services, but overall job growth was lower than expected. The government also reported a surprise gain of 17,000 public sector jobs.

DCR TrendLine February 2014 – Contingent Worker Forecast and Supply Report

It’s hard to believe that 2014 is already well underway. In the second month of the year, the staff at TrendLine was hard at work to provide you with key insights into the temporary staffing industry. With thorough research and in-depth analysis of data, we aim to supply you with a pulse of the temporary staffing market. As usual, our articles this month uncover trends in the industry and give you hard, actionable information on contingent workforce supply and demand.

March 2015 U.S. employment update and outlook

The national labor market continues to add jobs and maintain the momentum gained over the past few quarters, with 295,000 jobs added in February alone. Year-to-date, the economy has already seen 534,000 new jobs and is poised to sustain this level of growth over the next 12 to 18 months as other macroeconomic indicators—from consumer spending to bond issuance to business investment—continue their upward trajectory.

Unemployment dropped by 20 basis points to 5.5 percent, also enabling the 30-basis-point drop in total unemployment—which includes those not actively seeking work—to 11.0 percent, down from 11.3.

The Economy in 2014

The U.S. economic recovery took a major step forward in 2014, achieving a number of important milestones.

The Labor Market Situation - January 2014 Jobs Report

Dr Jennifer Hunt, U.S Department of Labor's Chief Economist reports on the Labor market situation in January, 2014.

Economic update (may 2013)

The US GDP grew at an annual rate of 2.5% in the first quarter of 2013, driven by strong growth in consumer spending and business investment in inventories. The US jobs report for April 2013 showed an addition of 165,000 jobs, revised upward from previous months. While this signals continued slow improvement in the jobs market, some signs of caution remained such as a decline in average work hours. The unemployment rate held steady at 7.5%.

US Talent Market Monthly March 2014

The document summarizes the February 2014 jobs report. It states that 175,000 new jobs were added in February, less than the average in 2013 but more than December and January. The unemployment rate rose slightly to 6.7% as more people entered the labor force. Gains were led by professional and business services adding 79,000 jobs. The report provides an overview of job growth over previous months and shows that while growth is positive, conditions remain cool with expectations of warming in coming months.

Permanent salaries rise at fastest rate since July 2007

Permanent salaries rise at fastest rate since July 2007, Steeper decline in candidate availability, Permanent and temporary appointments rise at slower rates, Further marked increase in vacancies

The Labor Market Situation - December 2013 Jobs Report

The Labor Market Situation

January 13, 2014

Dr. Jennifer Hunt, Chief Economist, U.S. Department of Labor

DLR_econlaboroutlook2012

The labor market is expected to continue slow growth in 2012, with unemployment remaining elevated around 8.8%. Payroll employment is projected to increase by an average of 110,000 jobs per month in the first half of 2012 and 126,000 in the second half. Wage growth is expected to be modest at around 2% as the large pool of unemployed continues to limit wage pressures. The outlook assumes extensions of payroll tax cuts and unemployment benefits, and downside risks exist if those policies are not continued.

Economic Forecast (August 2012)

This document provides an economic forecast from NAR Research. It includes forecasts and analyses for key economic indicators such as:

- Real GDP growth is forecast to be under 2% for the remainder of 2012 with no recession but also no robust expansion.

- Net new job growth is forecast to be 1.5 million in 2012 and 2.3 million in 2013.

- The unemployment rate is forecast to remain near 8% for most of 2012 and inflation is expected to rise to around 2% in 2013.

- Housing starts are forecast to rise 25% in 2012 and 50% in 2013, with the multifamily sector experiencing a stronger recovery. Existing and new home sales are also forecast to increase in

Similar to The Labor Market Situation September 11, 2013 (20)

Hiring Trends - Webinar with the Department of Labor and Business Forward

Hiring Trends - Webinar with the Department of Labor and Business Forward

DCR Trendline December 2013 – Contingent Worker Forecast and Supply Report

DCR Trendline December 2013 – Contingent Worker Forecast and Supply Report

Steven Jagger UK Jobs report October. Candidate Shortage

Steven Jagger UK Jobs report October. Candidate Shortage

DCR TrendLine February 2014 – Contingent Worker Forecast and Supply Report

DCR TrendLine February 2014 – Contingent Worker Forecast and Supply Report

The Labor Market Situation - January 2014 Jobs Report

The Labor Market Situation - January 2014 Jobs Report

Permanent salaries rise at fastest rate since July 2007

Permanent salaries rise at fastest rate since July 2007

The Labor Market Situation - December 2013 Jobs Report

The Labor Market Situation - December 2013 Jobs Report

More from businessforward

Webinar: Franz Litz on the Regional Greenhouse Gas Initiative

The Acadia Center released a report in September 2019 analyzing the impacts of offshore wind development on the New England electric grid. The report found that offshore wind could provide over 6,000 megawatts of clean energy to the region by 2035 and help states meet their renewable and decarbonization goals. Offshore wind was also shown to provide price stability and hedge against fossil fuel price volatility while creating thousands of jobs in the growing offshore wind industry.

Business Forward Solutions 2020 Policy Working Group

On Tuesday, June 25, Business Forward will welcome Al Fitzpayne, Executive Director of the Aspen Institute Future of Work Initiative, and Massachusetts State Senator Eric Lesser, for a Solutions 2020 Policy Working Group call on the future of work.

This is the second of the Solutions 2020 Future of Work Policy Working Group series. On this working group call, policy experts and business leaders will outline the future of work challenges facing our country and begin discussing policy solutions. This webinar will focus on designing portable benefits to bring financial security to workers in a changing economy.

Solutions 2020: Future of Work Policy Working Group

On Thursday, May 9, Business Forward will welcome Al Fitzpayne from the Aspen Institute and Massachusetts State Senator Eric Lesser for a conference call on the Future of Work.

Webinar: Attracting Immigrants and Growing Local Economies

This document discusses the role of immigrant entrepreneurs and innovation in regional economic development. It contains the following key points:

- Immigrant-owned businesses account for a disproportionately high percentage of export-oriented companies and play an important role in regional economies.

- The Welcoming Economies (WE) Global Network aims to promote inclusive economic development by embracing immigrant communities and recognizing their contributions.

- International students pursue graduate degrees in STEM fields at high rates and the WE Network works to help retain international talent through programs like job fairs and employer events.

- Skilled immigrants face challenges having foreign credentials recognized and the WE Network provides resources and programs to help with licensing, job skills, and career pathways.

Webinar: Carmel Martin on the Future of Work

High school graduates have trouble finding good jobs. There’s a mismatch in our economy, and it is about to get dramatically worse. Business Forward is joined by Carmel Martin, Managing Director of XQ Institute, for a discussion on how to redesign our schools for the 21st century.

Training Webinar: Making Public Policy Issues Relatable

Business Forward is joined by Nat Wood as he demonstrates the best practices and language for advocacy, media, and outreach, using health care reform as a case study.

Arielle Kane Health Care Update

Join Business Forward to welcome Arielle Kane, Director of Health Care at the Progressive Policy Institute, for a discussion on the current state of health care access in America. Kane will discuss how improvements to the ACA are more beneficial than repealing the law and moving to a single-payer system.

Webinar: New York Renews

NY Renews is a coalition of over 140 organizations pushing for 100% renewable energy in New York and protection of frontline communities most impacted by climate change. They support the Climate and Community Protection Act (CCPA), which would transition NY to 100% renewable energy by 2050 and introduce a fee on corporate polluters to fund clean energy and emission reduction programs. To pass the CCPA in 2019, NY Renews will focus on grassroots lobbying of legislators, local forums to raise awareness, and statewide mobilizations including a January direct action and February summit calling on the governor to take action.

Webinar: Recognizing and Responding to Discrimination in the Workplace

Today’s workplace thrives on innovation, empowerment, and an open dialogue. But what happens when social discord and discussion seeps into the workplace, bringing with it polarizing views and sometimes intolerance and discrimination?

Webinar with Carrie Irvin of Charter Board Partners

This document discusses the state of K-12 education in the United States and the role of public charter schools. It finds that student achievement is lagging, especially for low-income and minority students. Public charter schools on average provide stronger student outcomes, including additional learning gains. The nonprofit Charter Board Partners works to strengthen governance and quality at charter schools by recruiting skilled volunteers to serve on boards. Effective charter school boards play an important role in setting goals, overseeing leaders, and advocating for students.

Webinar with Carrie Irvin of Charter Board Partners

This document discusses the underperformance of the US education system and challenges facing students. It finds that only 1 in 3 US 8th graders is proficient in core subjects, many students require remedial college courses, and the US ranks below average in international assessments. It also notes poor and minority students face even greater obstacles. The document argues public charter schools can help address these issues by allowing more flexibility and family choice, and on average produce stronger student outcomes. It encourages business and community leaders to get involved by serving on charter school boards to help schools improve governance and student results.

2018 q2 gdp webinar with paul bishop

The US economy grew at an annual rate of 4.1% in the second quarter of 2018, the fastest pace since 2014. Strong growth was driven by increases in consumer spending, non-residential fixed investment, and net exports. Business investment grew 7.3% during this period, with double digit growth in structures and intellectual property. The housing sector slowed slightly, with a 1.1% decline in residential investment. Overall, the data indicates robust and broad-based economic expansion across many sectors in the first half of the year.

Webinar: Attracting Immigrants and Growing Local Economies

This document discusses building inclusive economies through immigrant integration and economic development initiatives. It highlights how immigrant communities are central to expanding economic opportunities and revitalizing regions. Regional development efforts can help retain immigrants and enhance their economic and social contributions. Examples of initiatives discussed include international student retention programs, skilled immigrant integration services, connector programs to help immigrants network, and support for immigrant entrepreneurship and homeownership. Data shows immigrants own disproportionate shares of high-export companies. The Welcoming Economies Global Network convenes members annually and facilitates city-to-city visits, publications, and webinars to strengthen inclusion efforts.

2018 useer executive summary presentation 6 12-18 business forward

The 2018 U.S. Energy and Employment Report surveyed over 30,000 employers to provide a more comprehensive count of energy jobs in the U.S. than previous Bureau of Labor Statistics data. Key findings include:

- Over 8 million Americans work in energy and energy efficiency jobs, 162,000 more than in 2017, with energy efficiency leading growth.

- Top states for solar employment are California and Massachusetts, while top states for wind are Texas and Iowa.

- 2.25 million Americans work in energy efficiency, a increase of 67,000, with over 1 million in construction and 450,000 in business services.

- Projected growth rates for 2018 are highest in energy efficiency at 9%

2018 Q1 GDP Webinar with Peter Borish

Peter Borish, Chief Investment Strategist and Portfolio Manager, Quad Capital Management Advisors LLC, will discuss the fundamentals of the economy, consumer trends, and areas of potential growth.

Highlights from 2017 Q4 and Year-End Estimates

On Friday, the U.S. Department of Commerce released its estimate of U.S. economic output for the last three months of 2017, as well as its year-end 2017 GDP numbers. Please join us for our quarterly webinar about the economy.

Ed Keon, Managing Director of QMA, a PGIM Company, will discuss the fundamentals of the economy, consumer trends, and areas of potential growth.

Register: http://myaccount.maestroconference.com/conference/register/0EW3K6EYMPO8KS8S

Business Forward's Quarterly GDP Webinar - 3Q2017

Robert Carroll, head of EY's National Director of the Quantitative Economics and Statistics Group and former Deputy Assistant Secretary for Tax Analysis of the U.S. Treasury Department, discusses the fundamentals of the economy, consumer trends, and areas of potential growth

Business Forward's Quarterly GDP Webinar - 3Q2017

The U.S. economy grew 3% in the third quarter of 2017, according to the latest GDP estimate. Consumer spending increased by 1.6% and contributed significantly to economic growth, while private investment grew by 0.98% and net exports increased by 0.41%. Business investment rose by 1.5%, with gains in construction, equipment, and industrial production. Residential investment declined by 0.24%. Overall, the report indicates steady economic growth continued in the third quarter driven by consumer spending and business investment.

The Latest Economic Trends - 1Q2017 GDP Report

The Commerce Department announced that the U.S. economy grew at an annual rate of 0.7 percent in the first quarter of 2017.

PGIM Managing Director Ed Keon will discuss the fundamentals of the economy, consumer trends, and areas of potential growth.

This webinar is the latest in Business Forward’s series on economic indicators. We provide this programming to help you stay up to date on the latest information about the economy and how it may affect your business.

The State of Cyber

EY Principal and Cyber Threat Management Leader Anil Markose shows you best practices for cyber risk management and how to sense, resist, and react to cyber attacks on your company.

More from businessforward (20)

Webinar: Franz Litz on the Regional Greenhouse Gas Initiative

Webinar: Franz Litz on the Regional Greenhouse Gas Initiative

Business Forward Solutions 2020 Policy Working Group

Business Forward Solutions 2020 Policy Working Group

Solutions 2020: Future of Work Policy Working Group

Solutions 2020: Future of Work Policy Working Group

Webinar: Attracting Immigrants and Growing Local Economies

Webinar: Attracting Immigrants and Growing Local Economies

Training Webinar: Making Public Policy Issues Relatable

Training Webinar: Making Public Policy Issues Relatable

Webinar: Recognizing and Responding to Discrimination in the Workplace

Webinar: Recognizing and Responding to Discrimination in the Workplace

Webinar with Carrie Irvin of Charter Board Partners

Webinar with Carrie Irvin of Charter Board Partners

Webinar with Carrie Irvin of Charter Board Partners

Webinar with Carrie Irvin of Charter Board Partners

Webinar: Attracting Immigrants and Growing Local Economies

Webinar: Attracting Immigrants and Growing Local Economies

2018 useer executive summary presentation 6 12-18 business forward

2018 useer executive summary presentation 6 12-18 business forward

Recently uploaded

Salesforce Integration for Bonterra Impact Management (fka Social Solutions A...

Sidekick Solutions uses Bonterra Impact Management (fka Social Solutions Apricot) and automation solutions to integrate data for business workflows.

We believe integration and automation are essential to user experience and the promise of efficient work through technology. Automation is the critical ingredient to realizing that full vision. We develop integration products and services for Bonterra Case Management software to support the deployment of automations for a variety of use cases.

This video focuses on integration of Salesforce with Bonterra Impact Management.

Interested in deploying an integration with Salesforce for Bonterra Impact Management? Contact us at sales@sidekicksolutionsllc.com to discuss next steps.

June Patch Tuesday

Ivanti’s Patch Tuesday breakdown goes beyond patching your applications and brings you the intelligence and guidance needed to prioritize where to focus your attention first. Catch early analysis on our Ivanti blog, then join industry expert Chris Goettl for the Patch Tuesday Webinar Event. There we’ll do a deep dive into each of the bulletins and give guidance on the risks associated with the newly-identified vulnerabilities.

Presentation of the OECD Artificial Intelligence Review of Germany

Consult the full report at https://www.oecd.org/digital/oecd-artificial-intelligence-review-of-germany-609808d6-en.htm

Fueling AI with Great Data with Airbyte Webinar

This talk will focus on how to collect data from a variety of sources, leveraging this data for RAG and other GenAI use cases, and finally charting your course to productionalization.

A Comprehensive Guide to DeFi Development Services in 2024

DeFi represents a paradigm shift in the financial industry. Instead of relying on traditional, centralized institutions like banks, DeFi leverages blockchain technology to create a decentralized network of financial services. This means that financial transactions can occur directly between parties, without intermediaries, using smart contracts on platforms like Ethereum.

In 2024, we are witnessing an explosion of new DeFi projects and protocols, each pushing the boundaries of what’s possible in finance.

In summary, DeFi in 2024 is not just a trend; it’s a revolution that democratizes finance, enhances security and transparency, and fosters continuous innovation. As we proceed through this presentation, we'll explore the various components and services of DeFi in detail, shedding light on how they are transforming the financial landscape.

At Intelisync, we specialize in providing comprehensive DeFi development services tailored to meet the unique needs of our clients. From smart contract development to dApp creation and security audits, we ensure that your DeFi project is built with innovation, security, and scalability in mind. Trust Intelisync to guide you through the intricate landscape of decentralized finance and unlock the full potential of blockchain technology.

Ready to take your DeFi project to the next level? Partner with Intelisync for expert DeFi development services today!

Digital Marketing Trends in 2024 | Guide for Staying Ahead

https://www.wask.co/ebooks/digital-marketing-trends-in-2024

Feeling lost in the digital marketing whirlwind of 2024? Technology is changing, consumer habits are evolving, and staying ahead of the curve feels like a never-ending pursuit. This e-book is your compass. Dive into actionable insights to handle the complexities of modern marketing. From hyper-personalization to the power of user-generated content, learn how to build long-term relationships with your audience and unlock the secrets to success in the ever-shifting digital landscape.

Finale of the Year: Apply for Next One!

Presentation for the event called "Finale of the Year: Apply for Next One!" organized by GDSC PJATK

Driving Business Innovation: Latest Generative AI Advancements & Success Story

Are you ready to revolutionize how you handle data? Join us for a webinar where we’ll bring you up to speed with the latest advancements in Generative AI technology and discover how leveraging FME with tools from giants like Google Gemini, Amazon, and Microsoft OpenAI can supercharge your workflow efficiency.

During the hour, we’ll take you through:

Guest Speaker Segment with Hannah Barrington: Dive into the world of dynamic real estate marketing with Hannah, the Marketing Manager at Workspace Group. Hear firsthand how their team generates engaging descriptions for thousands of office units by integrating diverse data sources—from PDF floorplans to web pages—using FME transformers, like OpenAIVisionConnector and AnthropicVisionConnector. This use case will show you how GenAI can streamline content creation for marketing across the board.

Ollama Use Case: Learn how Scenario Specialist Dmitri Bagh has utilized Ollama within FME to input data, create custom models, and enhance security protocols. This segment will include demos to illustrate the full capabilities of FME in AI-driven processes.

Custom AI Models: Discover how to leverage FME to build personalized AI models using your data. Whether it’s populating a model with local data for added security or integrating public AI tools, find out how FME facilitates a versatile and secure approach to AI.

We’ll wrap up with a live Q&A session where you can engage with our experts on your specific use cases, and learn more about optimizing your data workflows with AI.

This webinar is ideal for professionals seeking to harness the power of AI within their data management systems while ensuring high levels of customization and security. Whether you're a novice or an expert, gain actionable insights and strategies to elevate your data processes. Join us to see how FME and AI can revolutionize how you work with data!

Main news related to the CCS TSI 2023 (2023/1695)

An English 🇬🇧 translation of a presentation to the speech I gave about the main changes brought by CCS TSI 2023 at the biggest Czech conference on Communications and signalling systems on Railways, which was held in Clarion Hotel Olomouc from 7th to 9th November 2023 (konferenceszt.cz). Attended by around 500 participants and 200 on-line followers.

The original Czech 🇨🇿 version of the presentation can be found here: https://www.slideshare.net/slideshow/hlavni-novinky-souvisejici-s-ccs-tsi-2023-2023-1695/269688092 .

The videorecording (in Czech) from the presentation is available here: https://youtu.be/WzjJWm4IyPk?si=SImb06tuXGb30BEH .

AWS Cloud Cost Optimization Presentation.pptx

This presentation provides valuable insights into effective cost-saving techniques on AWS. Learn how to optimize your AWS resources by rightsizing, increasing elasticity, picking the right storage class, and choosing the best pricing model. Additionally, discover essential governance mechanisms to ensure continuous cost efficiency. Whether you are new to AWS or an experienced user, this presentation provides clear and practical tips to help you reduce your cloud costs and get the most out of your budget.

dbms calicut university B. sc Cs 4th sem.pdf

Its a seminar ppt on database management system using sql

Monitoring and Managing Anomaly Detection on OpenShift.pdf

Monitoring and Managing Anomaly Detection on OpenShift

Overview

Dive into the world of anomaly detection on edge devices with our comprehensive hands-on tutorial. This SlideShare presentation will guide you through the entire process, from data collection and model training to edge deployment and real-time monitoring. Perfect for those looking to implement robust anomaly detection systems on resource-constrained IoT/edge devices.

Key Topics Covered

1. Introduction to Anomaly Detection

- Understand the fundamentals of anomaly detection and its importance in identifying unusual behavior or failures in systems.

2. Understanding Edge (IoT)

- Learn about edge computing and IoT, and how they enable real-time data processing and decision-making at the source.

3. What is ArgoCD?

- Discover ArgoCD, a declarative, GitOps continuous delivery tool for Kubernetes, and its role in deploying applications on edge devices.

4. Deployment Using ArgoCD for Edge Devices

- Step-by-step guide on deploying anomaly detection models on edge devices using ArgoCD.

5. Introduction to Apache Kafka and S3

- Explore Apache Kafka for real-time data streaming and Amazon S3 for scalable storage solutions.

6. Viewing Kafka Messages in the Data Lake

- Learn how to view and analyze Kafka messages stored in a data lake for better insights.

7. What is Prometheus?

- Get to know Prometheus, an open-source monitoring and alerting toolkit, and its application in monitoring edge devices.

8. Monitoring Application Metrics with Prometheus

- Detailed instructions on setting up Prometheus to monitor the performance and health of your anomaly detection system.

9. What is Camel K?

- Introduction to Camel K, a lightweight integration framework built on Apache Camel, designed for Kubernetes.

10. Configuring Camel K Integrations for Data Pipelines

- Learn how to configure Camel K for seamless data pipeline integrations in your anomaly detection workflow.

11. What is a Jupyter Notebook?

- Overview of Jupyter Notebooks, an open-source web application for creating and sharing documents with live code, equations, visualizations, and narrative text.

12. Jupyter Notebooks with Code Examples

- Hands-on examples and code snippets in Jupyter Notebooks to help you implement and test anomaly detection models.

System Design Case Study: Building a Scalable E-Commerce Platform - Hiike

This case study explores designing a scalable e-commerce platform, covering key requirements, system components, and best practices.

Nunit vs XUnit vs MSTest Differences Between These Unit Testing Frameworks.pdf

When it comes to unit testing in the .NET ecosystem, developers have a wide range of options available. Among the most popular choices are NUnit, XUnit, and MSTest. These unit testing frameworks provide essential tools and features to help ensure the quality and reliability of code. However, understanding the differences between these frameworks is crucial for selecting the most suitable one for your projects.

leewayhertz.com-AI in predictive maintenance Use cases technologies benefits ...

Predictive maintenance is a proactive approach that anticipates equipment failures before they happen. At the forefront of this innovative strategy is Artificial Intelligence (AI), which brings unprecedented precision and efficiency. AI in predictive maintenance is transforming industries by reducing downtime, minimizing costs, and enhancing productivity.

Recently uploaded (20)

Deep Dive: AI-Powered Marketing to Get More Leads and Customers with HyperGro...

Deep Dive: AI-Powered Marketing to Get More Leads and Customers with HyperGro...

Salesforce Integration for Bonterra Impact Management (fka Social Solutions A...

Salesforce Integration for Bonterra Impact Management (fka Social Solutions A...

Presentation of the OECD Artificial Intelligence Review of Germany

Presentation of the OECD Artificial Intelligence Review of Germany

A Comprehensive Guide to DeFi Development Services in 2024

A Comprehensive Guide to DeFi Development Services in 2024

WeTestAthens: Postman's AI & Automation Techniques

WeTestAthens: Postman's AI & Automation Techniques

Digital Marketing Trends in 2024 | Guide for Staying Ahead

Digital Marketing Trends in 2024 | Guide for Staying Ahead

Driving Business Innovation: Latest Generative AI Advancements & Success Story

Driving Business Innovation: Latest Generative AI Advancements & Success Story

Overcoming the PLG Trap: Lessons from Canva's Head of Sales & Head of EMEA Da...

Overcoming the PLG Trap: Lessons from Canva's Head of Sales & Head of EMEA Da...

Nordic Marketo Engage User Group_June 13_ 2024.pptx

Nordic Marketo Engage User Group_June 13_ 2024.pptx

Monitoring and Managing Anomaly Detection on OpenShift.pdf

Monitoring and Managing Anomaly Detection on OpenShift.pdf

System Design Case Study: Building a Scalable E-Commerce Platform - Hiike

System Design Case Study: Building a Scalable E-Commerce Platform - Hiike

Nunit vs XUnit vs MSTest Differences Between These Unit Testing Frameworks.pdf

Nunit vs XUnit vs MSTest Differences Between These Unit Testing Frameworks.pdf

leewayhertz.com-AI in predictive maintenance Use cases technologies benefits ...

leewayhertz.com-AI in predictive maintenance Use cases technologies benefits ...

The Labor Market Situation September 11, 2013

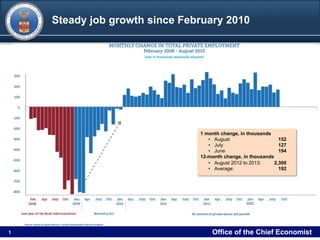

- 1. DRAFT 11Filename/RPS Number Office of the Chief Economist1 Steady job growth since February 2010 1 month change, in thousands • August 152 • July 127 • June 194 12-month change, in thousands • August 2012 to 2013: 2,300 • Average: 192

- 2. DRAFT 22Filename/RPS Number Office of the Chief Economist2 Steady unemployment decline since end 2009

- 3. DRAFT 33Filename/RPS Number Office of the Chief Economist3 Employment-to-population ratio has not recovered to pre-recession rates

- 4. DRAFT 44Filename/RPS Number Office of the Chief Economist4 Retail Trade has led job growth the past three months

- 5. DRAFT 55Filename/RPS Number Office of the Chief Economist5 Involuntary part time for economic reasons has fallen among private-sector and non-Federal Government Source: Bureau of Labor Statistics, Current Population Survey, www.bls.gov/cps

- 6. DRAFT 66Filename/RPS Number Office of the Chief Economist6 Since ACA became law, 9 out of 10 new positions are full time

- 7. DRAFT 77Filename/RPS Number Office of the Chief Economist7 No systemic evidence employers are shifting employees to <30 hours per week Source: Bureau of Labor Statistics, Current Population Survey, www.bls.gov/cps

- 8. DRAFT 88Filename/RPS Number Office of the Chief Economist8 Mix of full-time and part-time employment is typical for an economic recovery

- 9. DRAFT 99Filename/RPS Number Office of the Chief Economist9 Thank you!