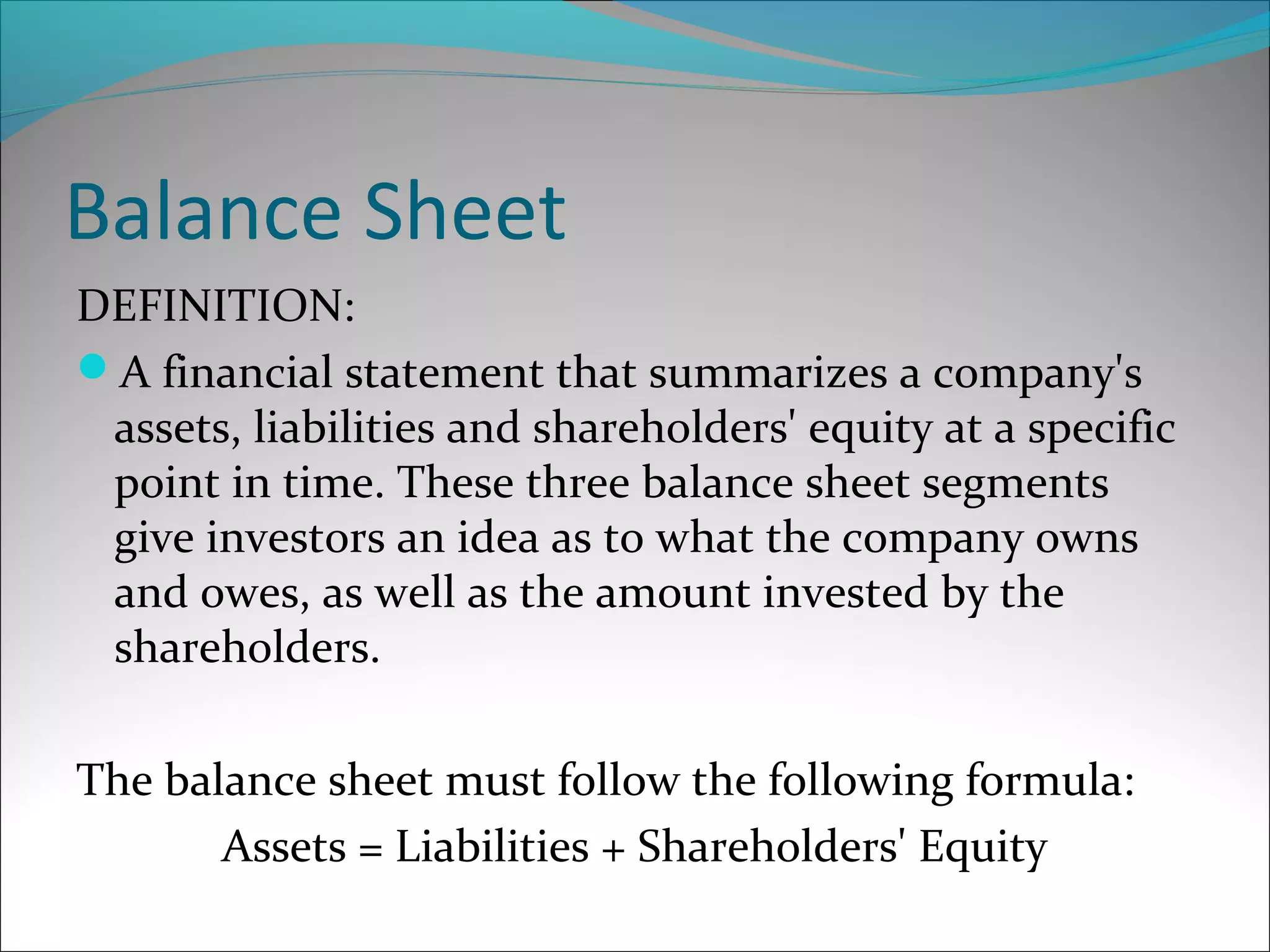

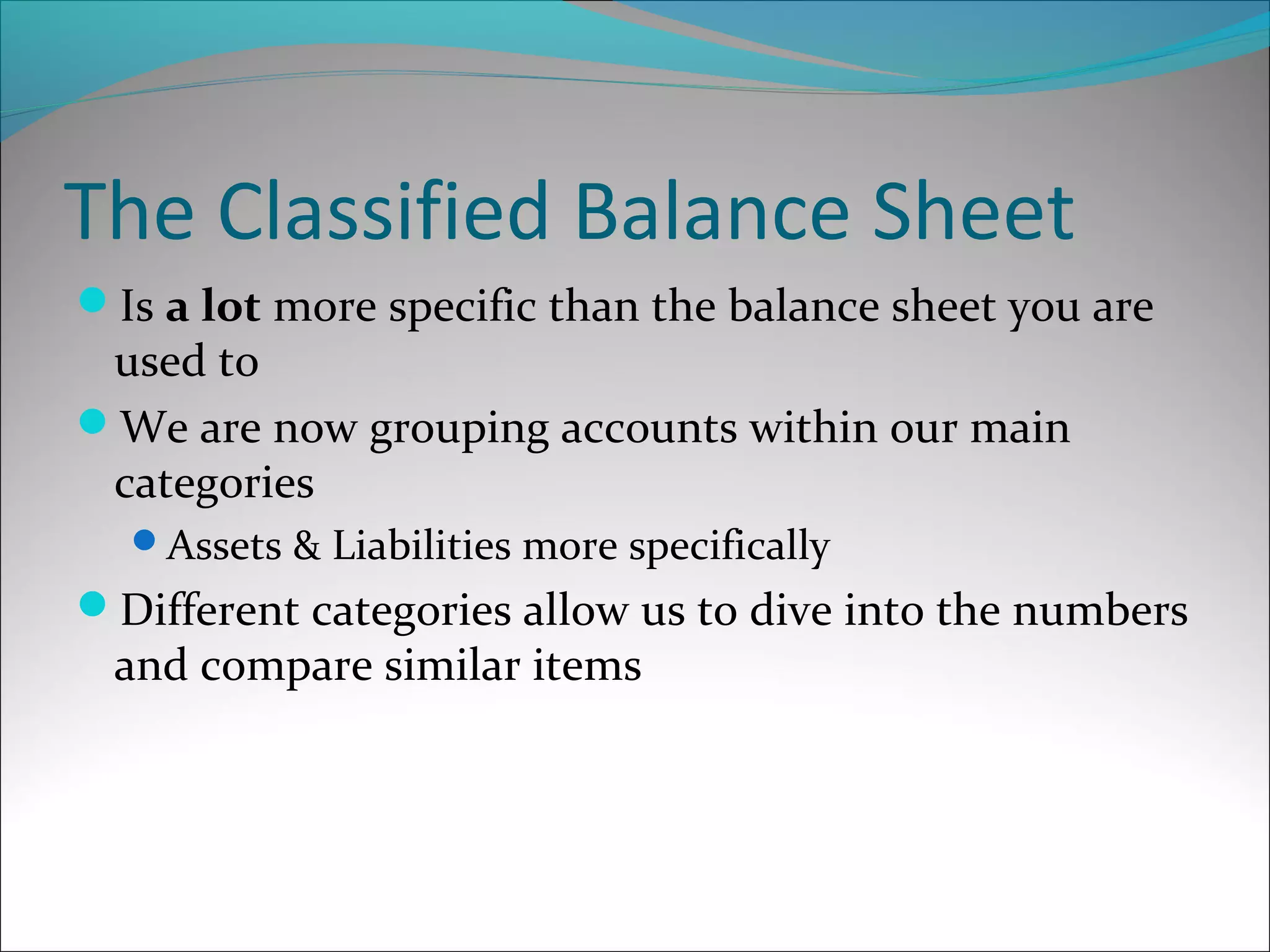

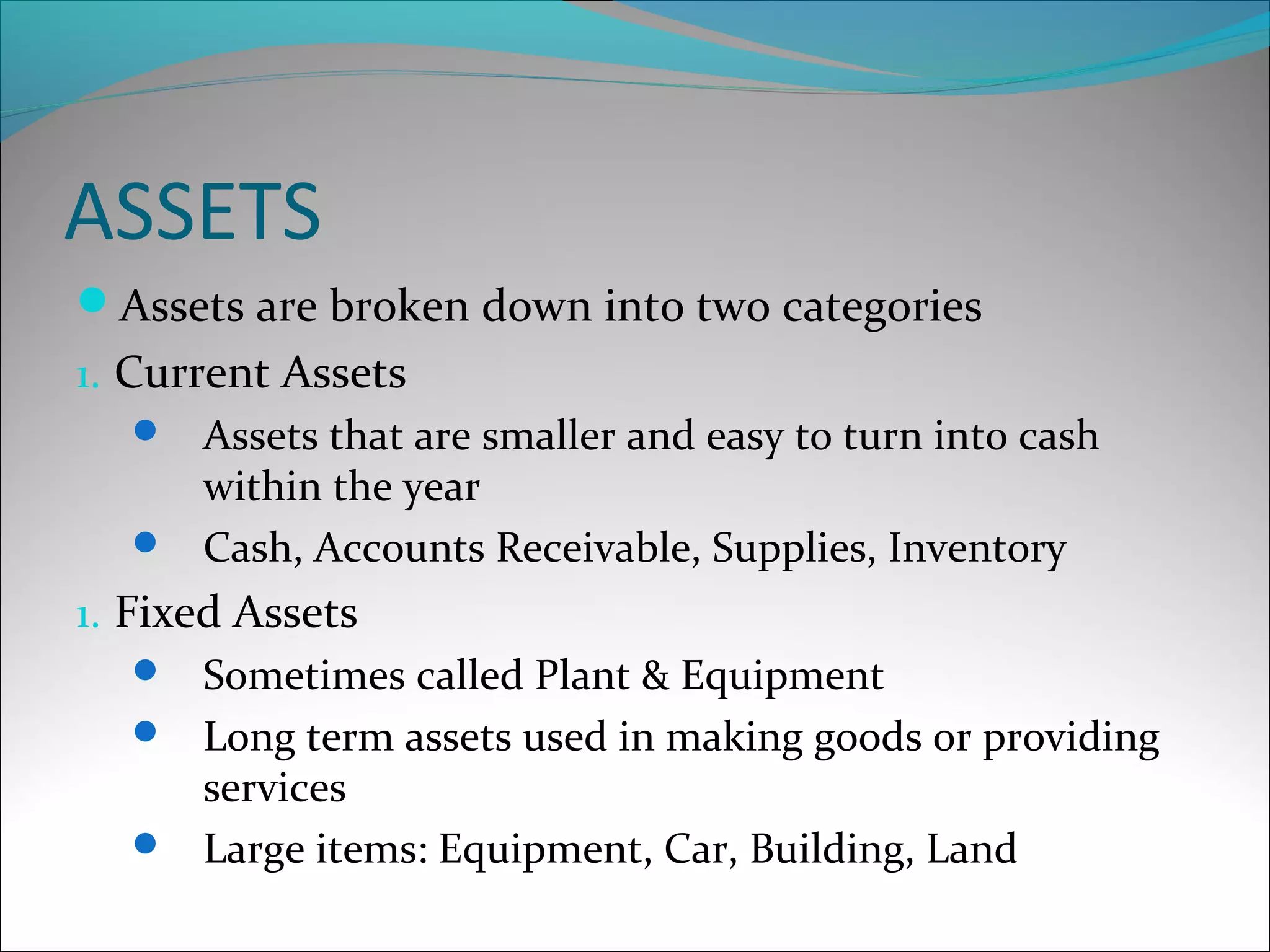

The document provides an overview of balance sheets, explaining that a balance sheet summarizes a company's assets, liabilities, and shareholders' equity at a specific point in time. It discusses the components of a balance sheet, including current and fixed assets, current and long-term liabilities, and owners' equity. The document also demonstrates how to construct a classified balance sheet that categorizes accounts in more detail than a regular balance sheet.