This document discusses household budgeting and provides tips for addressing a budget deficit. It defines key budgeting terms like current expenditure, capital expenditure, accruals, and savings. It also outlines five possible changes a family could make to their budget if facing a deficit, such as cutting discretionary spending, reducing household costs through better buying, spreading large payments over multiple months, increasing income through overtime or part-time work. Maintaining a budget requires estimating future income and expenses to plan finances.

At homework1 you can be benefited in a multifaceted way and you also select the best service provider from the market. We offer quality macroeconomics homework help at very affordable price.

At homework1 you can be benefited in a multifaceted way and you also select the best service provider from the market. We offer quality macroeconomics homework help at very affordable price.

All the information about the fiscal policy is provided in this slide for ever BBA student it is easy to understand the fiscal policy and its terms and types INFORMATION FOR CLASS PROJECTS AND CLASS PRESENTATION

Unit one of Floyd Saunders' Personal Money Management Seminars - Learn the basics of budgeting and why managing your money starts with controlling spending. This is the first unit in a series of six that include: buying your first home, credit cards, living on your own, handling credit and savings/investing. Contact me for the instructor's guide and participant workbooks.

Reasons for Developing a Personal BudgetKevin Waida

A communications student at the University of Missouri, Kevin Waida is also pursuing a minor in personal financial planning. Viewing this as his primary professional interest, Kevin Waida has joined the Financial Planning Association.

Through this presentation you can get idea regarding Nominal GDP ,and i have also solved Nominal GDP problem ,so i hope it can help you to understand Nominal GDP.

All the information about the fiscal policy is provided in this slide for ever BBA student it is easy to understand the fiscal policy and its terms and types INFORMATION FOR CLASS PROJECTS AND CLASS PRESENTATION

Unit one of Floyd Saunders' Personal Money Management Seminars - Learn the basics of budgeting and why managing your money starts with controlling spending. This is the first unit in a series of six that include: buying your first home, credit cards, living on your own, handling credit and savings/investing. Contact me for the instructor's guide and participant workbooks.

Reasons for Developing a Personal BudgetKevin Waida

A communications student at the University of Missouri, Kevin Waida is also pursuing a minor in personal financial planning. Viewing this as his primary professional interest, Kevin Waida has joined the Financial Planning Association.

Through this presentation you can get idea regarding Nominal GDP ,and i have also solved Nominal GDP problem ,so i hope it can help you to understand Nominal GDP.

1. This is combined money earned by, the father and mother (if she is working). and other working members of the family.

2. money earned from working as employees of a commercial/ industrial services companies.

3. money earned from selling real estate, insurance, appliances, educational plans, life plans, and the like.

4. money given as addition to a regular income as a recognition for a number of years of service in a company.

5. money granted by the govemment or private companies upon one's retirement from the service.

6. money earned from operating a business.

7. One of the most effective tools to handle money wisely.

1. family income

2. salaries/wages

3. commission

4. bonus

5. pension

6. profit

7. budget

Will you go over budget this holiday season? How will you know? Learn how to budget for periodic expenses. Learn how to track spending so you know how much you have to spend.

Cash Flow Planning Bonus ProjectPlan AheadWe are told, inMaximaSheffield592

Cash Flow Planning Bonus Project

Plan Ahead

We are told, in business, that we should be proactive; and broadly what is meant by that is to focus our efforts and attention on the long-term and to think in terms of the long-term consequences of our actions.

Proactive people simply will not accept that there is nothing that can be done about the unreasonable boss or the events of daily life - they will point out that there are always choices. It is by the decisions we make, our responses to people, events and circumstances that proactive people can and do affect the future. We may have no control over what life throws at us but we always have a choice about how we are to respond. —Stephen Covey's landmark book The 7 Habits of Highly Effective People

The purpose of creating a Cash Flow Plan is to spend your paycheck on paper before you actually spend it during the month

Remember:

Money is active and always moving

Wealth is no longer measured in what you make a year

Wealth is measured in what you do with your money during a year

You will either be on your way to being wealthy, broke, or poor

Give your money a name

Rent/Mortgage, food, utilities, taxes, insurance, etc.

Money that is simply left unaccounted for will always find a way out of your personal financial plan

This Cash Flow Plan should be done every pay period!

Recommended Percentages used for Budgeting

The following are a compilation of several sources to derive the suggested percentage guidelines. However, these are only recommended percentages and will change dramatically if you have a very high or very low income.

For instance, if you have a very low income, your necessities percentages will be high. If you have a high income your necessities will be a lower percentage of income and hopefully savings (not debt) will be higher than recommended.

ITEMACTUAL %RECOMMENDED %

CHARITABLE GIFTS _________ 10%

SAVING _________ 5-10%

HOUSING _________ 25 -35%

UTILITIES _________ 10-15%

FOOD _________ 15%

TRANSPORTATION _________ 10%

CLOTHING _________ 2-7%

MEDICAL/HEALTH _________ 5-10%

PERSONAL _________ 5-10%

RECREATION _________ 5%

DEBTS _________ 5-10%

Cash Flow Planning

Every dollar of your income should be allocated to some category on this sheet. Money "left over" should be put back into a category even if you make up a new category. You are making the spending decisions ahead of time here. Almost every category (except debt) should have some dollar amount in it.

Fill in the amount for each subcategory under "Subtotal" and then the total each main category under "Total." As you go through your first month, fill in the "Actually Spent" column with your real expenses or the saving you did for that area. If there is a substantial difference in the plan versus the reality something has to give. You will either have to adjust the amount allocated to that area up and another down or you will have to better c ...

Australian Lifeskills - Budgeting Level 3Teejay Maths

Suits ages 11-15 after completion of Level 2 Financial Maths lessons

Lesson Objective:

By the end of the lesson, pupils will be expected to understand the purpose of a budget and the impact changes to income and expenditure will have to the overall budget.

Outcomes:

I can budget effectively, manage money and plan for future expenses making use of technology and other methods, to

In this Webinar, participants will learn about:

– Balancing rising costs and a limited budget

– Eating healthily, food banks, other resources in your community

– Budget formats that work for cancer patients

– Money management

– Debit and credit management

– Credit counselling

– Consumer protection

Budgeting and Savings with ING Driect and ACCION USAACCION East

Make sure to look out for the next workshop that ACCION and ING wil host at http://www.accionusa.org/home/small-business-loans/financial-education-resources/workshop-calendar.aspx

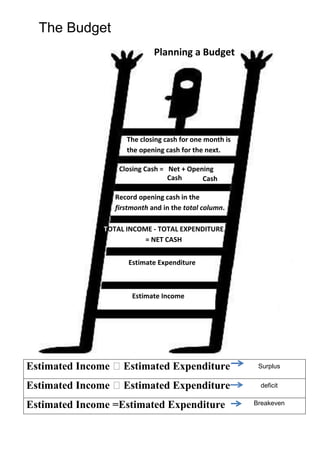

1. The Budget

Estimated Income ˃Estimated Expenditure Surplus

Estimated Income ˃Estimated Expenditure deficit

Estimated Income =Estimated Expenditure Breakeven

Planning a Budget

Estimate Income

Estimate Expenditure

TOTAL INCOME - TOTAL EXPENDITURE

= NET CASH

Record opening cash in the

firstmonth and in the total column.

Closing Cash = Net + Opening

CashCash

The closing cash for one month is

the opening cash for the next.

2. The Budget

If a family had a deficit for the year, what possible changes could they make to the

household budget?

1. Cut back on discretionary expenditure- birthdays, holidays, entertainment,

presents, etc.

2. Reduce household coststhrough better buying.

3. Cut back on household costs and car costs.

4. Spread large payments over a number of months rather than paying for them all at

once, e.g. car insurance, health insurance.

5. Try and increase income by doing overtime or part-time work.

CURRENT EXPENDITURE

This is spending on items that we need to run the house

on a daily basis, e.g. food, fuel, clothes, etc.

CAPITAL EXPENDITURE

This is spending on items that will last a long time,e.g.

car, television, cooker, washing machine, etc.

ACCRUALS These are services that we do not pay for at the time of

use, e.g. electricity, telephone bill.

We pay for the amount we owe when we get the bill.

SAVINGS

This is putting money aside for the future, e.g.

emergencies, to buy a car, to pay for children’s

education.

Remember:

A budget is a plan which forecasts future income, future expenditure and savings.

We must guess what these figures will be.