Download to read offline

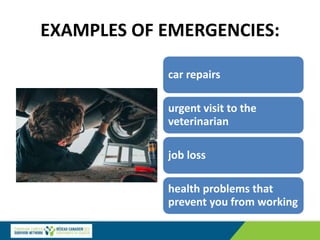

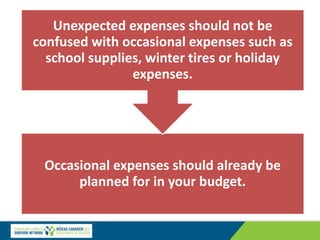

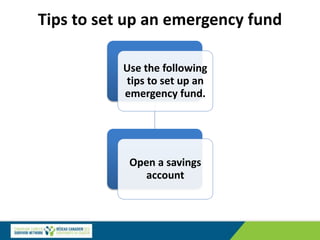

This document provides information to help individuals better manage their finances when dealing with a health issue like cancer. It discusses creating a budget to balance costs and limited income. Tips for the budget include setting financial goals, tracking spending, and creating an emergency fund. The document also addresses resources for healthy eating on a limited budget, managing debt, using credit counseling, and understanding consumer rights regarding debt collection. Overall, the information aims to help gain confidence in financial planning and allow a focus on medical treatment and recovery.