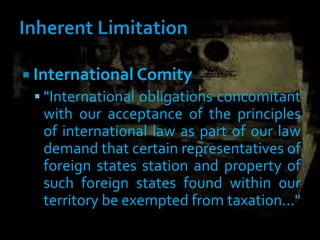

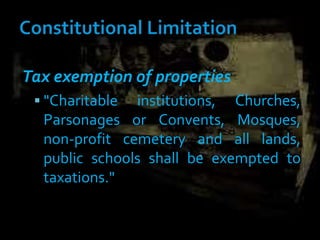

The document discusses the key principles of taxation according to Philippine law. It defines taxation as the enforced proportional contributions from people and property levied by the sovereign state to support the government and public needs. The main points are:

1) Taxation is justified based on the necessity theory, that government needs funds to operate, and the benefit-protection theory, that citizens pay taxes in exchange for benefits of organized society.

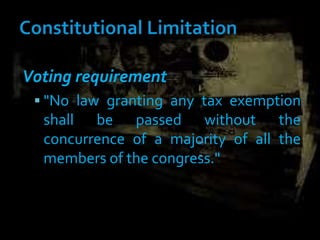

2) The legislative body has broad powers to determine what is taxed, tax rates, and collection methods, provided it is for a public purpose.

3) Taxes are a personal obligation and corporations' tax debts cannot be enforced against stockholders, with some exceptions.

4)

![Philippine%20taxation..[1]](https://cdn.slidesharecdn.com/ss_thumbnails/philippine20taxation-150909111327-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)

![Taxation lectures[1]](https://cdn.slidesharecdn.com/ss_thumbnails/taxation-lectures1-101011032905-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Basic concept-principle-of-taxation[1]](https://cdn.slidesharecdn.com/ss_thumbnails/basic-concept-principle-of-taxation1-180927025348-thumbnail.jpg?width=640&height=640&fit=bounds)