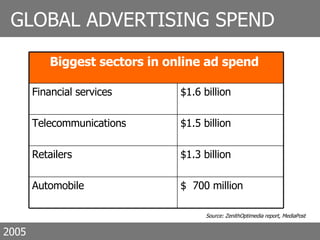

Downloaded 2,488 times

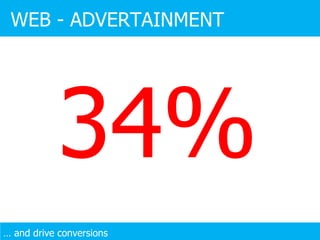

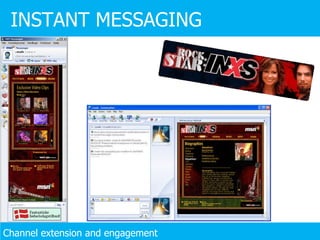

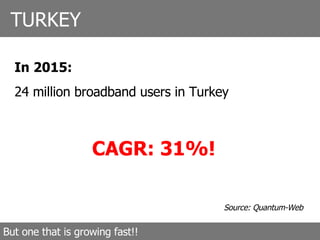

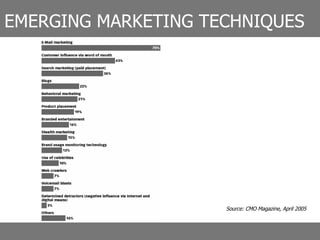

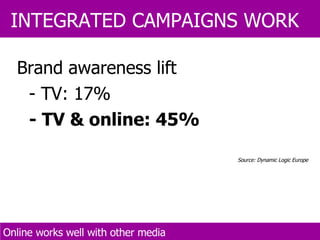

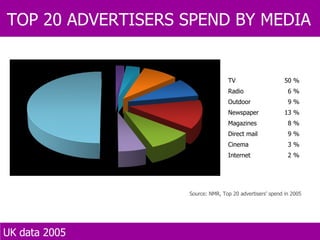

![Source: Dynamic Logic MarketNorms MarketNorms data through June 30, 2004; N=199 European campaigns, n=163,262 respondents Percent Online Ad Effectiveness, European Averages ONLINE BUILDS BRANDS +5.4% Which of the following [brands, products] have you heard of before?” Of those who had not seen the online ad, 68.9% were aware of the brand Of those who had seen the online ad, 72.6% were aware of the brand So, the ad caused a 5.4% increase in awareness](https://image.slidesharecdn.com/tviralbrazil052007-1213660832037838-9/85/Digital-Marketing-103-320.jpg)

![Casper M ø ller CEO, T-Viral E: [email_address] T: +44 (0)20 7231 1320 42 Pump House Close London SE16 7HS United Kingdom I: www.t-viral.com](https://image.slidesharecdn.com/tviralbrazil052007-1213660832037838-9/85/Digital-Marketing-188-320.jpg)

The document discusses the evolution and importance of digital marketing, emphasizing the need for brands to adapt to changes in consumer behavior and media consumption. It highlights the impact of technology on marketing strategies, the rise of digital channels, and the significance of consumer engagement through online platforms. Additionally, it outlines the effectiveness and benefits of digital advertising, suggesting brands allocate a portion of their budgets to digital efforts to enhance brand awareness and consumer interaction.