Downloaded 13 times

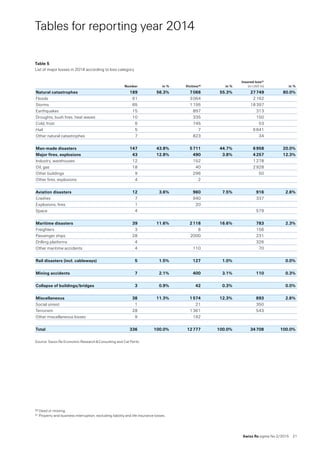

In 2014, there were 336 recorded disaster events, including a record 189 natural catastrophes and 147 man-made disasters, resulting in over 12,700 fatalities. Total economic losses reached approximately USD 110 billion, significantly lower than previous years, with Asia suffering the most from severe weather. Insured losses amounted to USD 35 billion, primarily driven by severe thunderstorms and harsh winter conditions in the US and Japan.