Downloaded 11 times

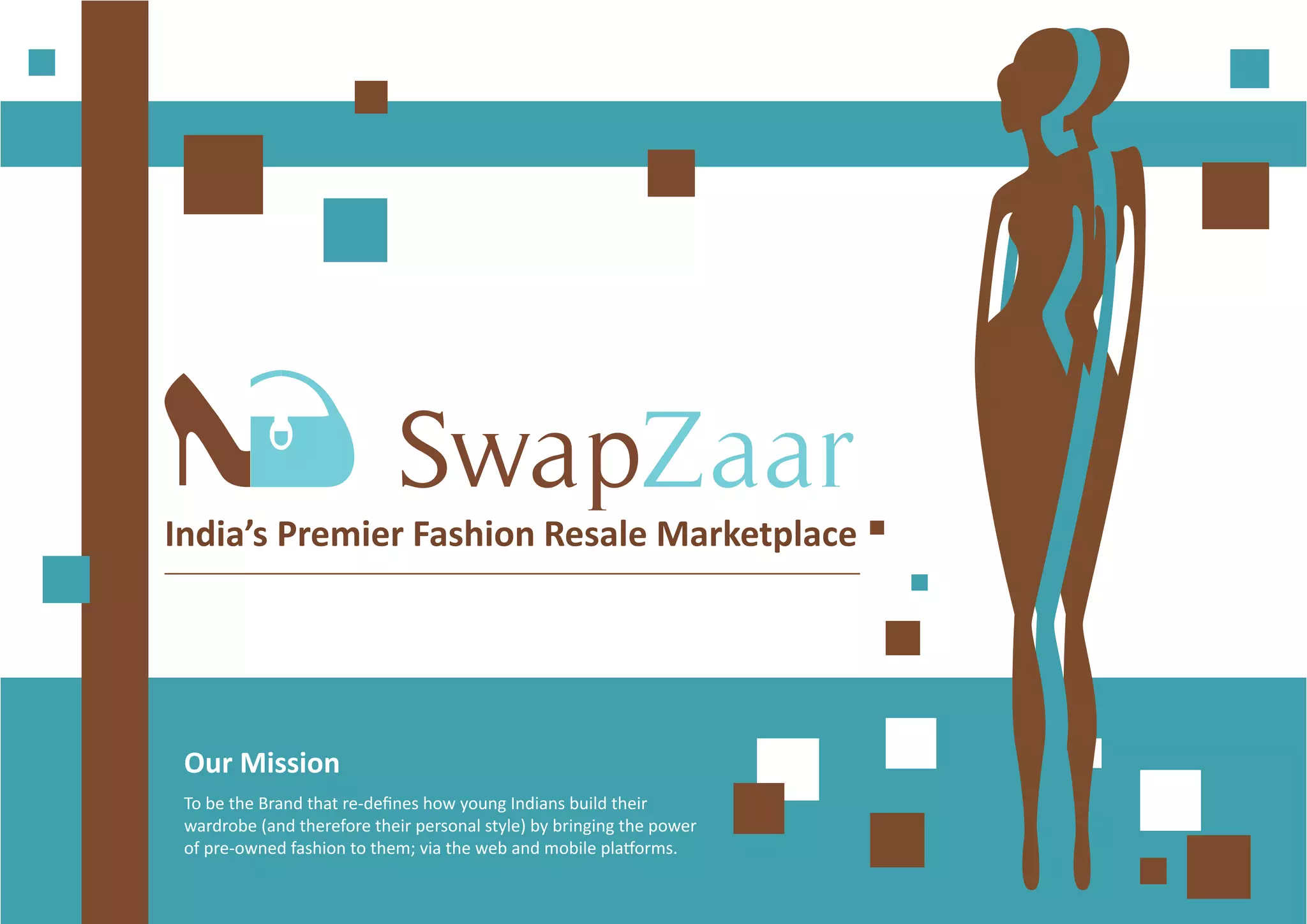

This document discusses the growing trend of the sharing economy, especially in the fashion resale market. Some key points: - The sharing economy, which includes companies like AirBnB, Uber, and Rent the Runway, is growing significantly and could be worth $335 billion by 2025. Younger generations are more open to sharing and renting goods rather than ownership. - Popular fashion resale companies like The RealReal and Rent the Runway have millions of members and hundreds of millions in revenues and valuations, showing the significant size of the resale market. - The global second-hand luxury goods market was worth an estimated €16 billion in 2014. Emerging markets like India and

![Luxury Ecommerce [infusion 3rd october 2014]](https://cdn.slidesharecdn.com/ss_thumbnails/luxuryecommerceinfusion3rdoctober2014-141003092252-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)