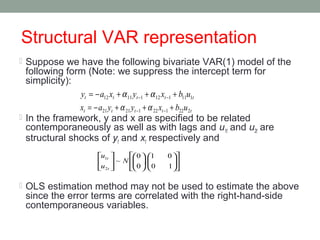

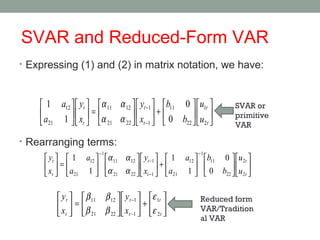

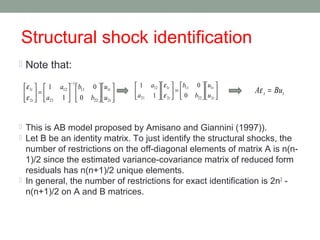

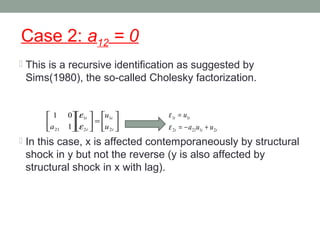

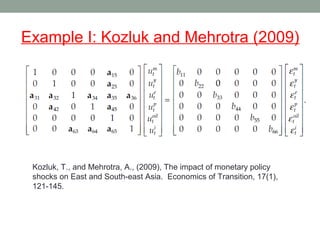

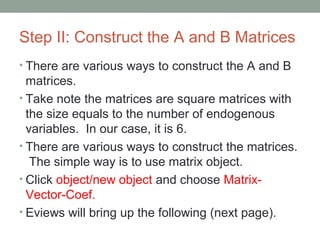

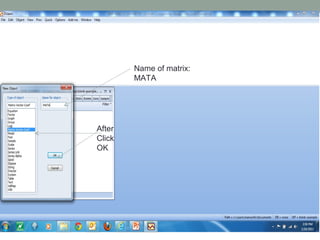

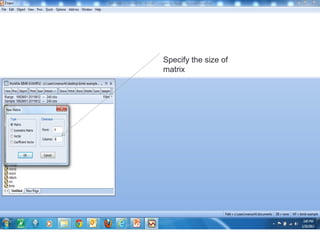

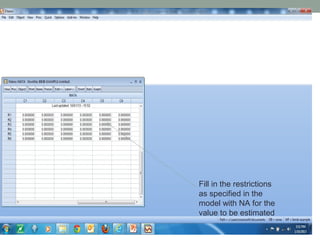

The document discusses the structural VAR (SVAR) model, emphasizing the importance of shock identification within the VAR framework. It outlines the theoretical foundations and methodologies for estimating structural relationships among multiple variables, showcasing the AB model proposed by Amisano and Giannini (1997). The text also provides step-by-step guidance for constructing and estimating structural factorization in empirical applications.