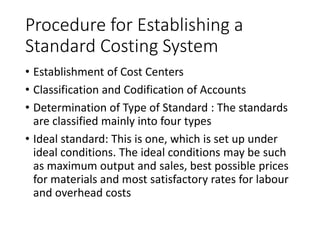

This document outlines the procedure for establishing a standard costing system including:

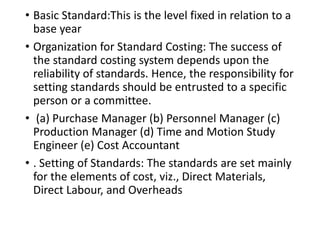

1) Establishing cost centers, classifying accounts, and determining the type of standard which can be ideal, expected, normal, or basic.

2) Organizing responsibility for setting standards which is typically given to a purchase manager, personnel manager, production manager, time and motion study engineer, or cost accountant.

3) Setting standards for direct materials, direct labor, variable overhead, and fixed overhead which includes standard quantities, prices, times, rates, budgets, and output to calculate recovery rates.