1. Erste Group Research – Trade between China and the West: three historical highlights Page 1

Erste Group Research

CEE Special Report: Trade between China and the West

30 November 2012

Trade between China and the West: three

historical highlights

We examine three historical periods in human history when China and Western

nations have engaged in significant expansion of trade.

Maryan Zablotskyy

maryan.zablotskyy@erstebank.ua

Foreword

Growing trade between Western nations and China has been one of the key

factors to shape the world in the past decade. This is the third time in history

that there has been an explosion of trade volume between East and West.

Quite remarkably, two previous periods of trade expansion (206 BCE – 220

CE and 1757-1860) bear similarities in how this trade developed.

Episode 1: Han and Roman Empires, 206

BCE – 220 CE

The earliest boom in international trade came with the dynamic economic

growth of both East and West. The Roman Empire had had its first experience

with modern democracy. China was ruled by the Han Dynasty, which had

absolute power. Romans had the highest income per capita in the world,

especially in the Italian peninsula. At the beginning of the first millennium, the

Roman Empire a population of around 44mn, 8mn of which lived in the

territory of modern Italy. According to the tax census from 2AD, China had a

population of around 57mn. The empires had economies which were roughly

the same size and which each represented a quarter of the world’s GDP.

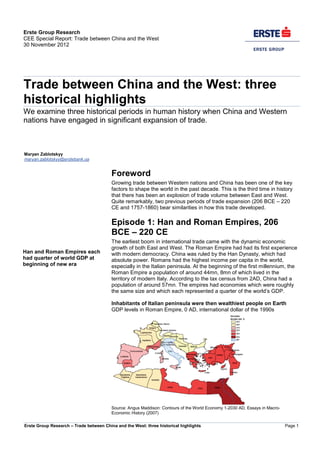

Inhabitants of Italian peninsula were then wealthiest people on Earth

GDP levels in Roman Empire, 0 AD, international dollar of the 1990s

Source: Angus Maddison: Contours of the World Economy 1-2030 AD, Essays in Macro-

Economic History (2007)

Han and Roman Empires each

had quarter of world GDP at

beginning of new era

2. Erste Group Research

CEE Special Report: Trade between China and the West

30 November 2012

Erste Group Research – Trade between China and the West: three historical highlights Page 2

Citizens of modern Italy were twice as rich as the Chinese, while many parts

of the Roman Empire also had higher income levels compared to those in

Asia. What also distinguished Romans was their overwhelming military power.

The infrastructure of the Romans was more focused on commerce (paved

roads, bridges). The Chinese, in turn, focused on building large-scale

fortifications and canals. The famous Great Wall of China was started during

the Han dynasty.

Roman citizens were richer that those of Asia

GDP per capita, international dollar of 1990s

450 450

550

600

810

China India Greece Egypt Italy

Source: Angus Maddison

Romans had overwhelming military power and

infrastructure

House prices to disposable income ratio, 2004=100

Around 0 AD Roman Empire Han Empire

Metal production

Iron 82 500 5 000

Copper 15 000 Negligable

Lead 80 000 Negligable

Silver 200 1

Inftrastructure

Road network, km 400 000 22 000

of which paved 50 000 Negligable

Brigdes 931 3

Source: wikiversity.org

The first international trade appeared between the Roman Empire and China

in the beginning of the 2

nd

century BCE. The main exchange: Roman gold for

Chinese silk. This gave the name to the famous trade route called the ‘Silk

Road’.

Many countries prospered because of Chinese-Roman trade, giving rise

to world’s first global foreign trade market

‘Silk route’, 206 BCE – 220 CE

Source: Wikipedia

Besides silk, China also traded teas and porcelain; while India traded spices,

ivory, textiles, precious stones, and pepper. The Roman Empire primarily

exported gold, silver, but also some goods, such as fine glassware, wine,

carpets, and jewels.

First global trade emerged from

Roman exchange of gold and

silver for China’s silk

3. Erste Group Research

CEE Special Report: Trade between China and the West

30 November 2012

Erste Group Research – Trade between China and the West: three historical highlights Page 3

Silk clothing was in great demand by Roman women, although it was

considered to be decadent and immoral.

“I can see clothes of silk, if materials that do not hide the body, nor even one's

decency, can be called clothes. ... Wretched flocks of maids labor so that the

adulteress may be visible through her thin dress, so that her husband has no

more acquaintance than any outsider or foreigner with his wife's body”

— Seneca the Younger, 4 BC – 65 AD

The Roman Senate issued, in vain, several edicts to prohibit the wearing of

silk, both on economic and moral grounds: the importation of silk caused a

huge outflow of gold.

"By the lowest reckoning, India, Seres and the Arabian peninsula take from

our Empire 100 millions of sesterces every year: that is how much our luxuries

and women cost us."

— Pliny the Elder, 23 AD – 79 AD

Romans had to pay in gold and silver as there was little demand for the goods

they produced. This was due to protectionist policies from China, which

emerged from its views on being a self-sufficient state. Historian Charles

Hucker, in his book on China’s imperial history, writes:

“In keeping with their domestic policies, the Chinese dynasties of the early

imperial age did not generally encourage foreign trade. It was not considered

either proper or safe for Chinese to have private intercourse with uncivilized

people, indeed unofficial travel beyond the frontiers was often deemed

treasonable”.

Still, high demand for Chinese products and the significant military power of its

neighbors made the Chinese government think that it was safer to allow

restricted forms of trade under government supervision. To maintain the self-

sufficiency of the state and still allow foreign trade, China officially traded only

with states it considered to be its vassals. Roman merchants claiming to be

diplomats from often nonexistent states visited Chinese government officials

in order to get permission to trade. Charles Hucker says:

“Tributary missions from vassal states were commonly allowed to include

traders, who thus gained opportunities to do business in the capital markets.

No doubt a large proportion of what the Chinese court chose to call tributary

missions were in fact shrewdly organized commercial ventures by foreign

merchants with no diplomatic status at all.”

What was supposed to be a protectionist policy against foreign goods turned

into a corruption scheme. Chinese government officials benefited from using

their control over foreign trade by allowing deals with western merchants

disguised as ‘diplomats’. As a result, China did experience a huge boom in

trade, but with most of the proceeds, in the form of gold and silver, going to

bureaucratic elite and little import of goods into the country. Since the elite

was afraid of losing their position and of criminal prosecution, they opted to

hoard gold and silver within their estates. There was so much inflow of

precious metal that it was used for making statues. Meanwhile, peasants were

banned from merchant activity. Additionally, peasants suffered pressure from

large landowners; in the following years, many peasants lost their land and

were forced into the service of the elite.

Demand for Chinese silk caused

huge outflows of gold and silver

from Roman Empire

Chinese governments tried to

control foreign trade

China’s state control on foreign

trade caused corruption among

officials and positive trade

balance with Western world

4. Erste Group Research

CEE Special Report: Trade between China and the West

30 November 2012

Erste Group Research – Trade between China and the West: three historical highlights Page 4

Gold and silver drained from the Roman Empire due to the negative trade

balance between the two empires. Soon Rome was finding it hard to pay its

soldiers. In addition to gold outflows, Romans were facing increasing pressure

from the tribes populating its northern borders. The debasement of currency

was one of the key ways that Rome found to pay its soldiers. As even that

was not enough, soon Rome began to rely more on barbarian mercenaries

and started giving out rights to collect taxes on its territory. That turned into a

cycle which eventually destroyed the state.

Romans debased currency to increase soldiers pay

Source: http://www.zerohedge.com/

Inflation soared due to currency debasement

Source: http://www.zerohedge.com/

The resulting fall of Rome was nothing less than a catastrophe. Both output

and population declined markedly. It was not until the 17

th

century that the

Mediterranean region saw levels of economic activity comparable to those

during the first two centuries of the first millennium. This statement is based

on levels of world lead production (a side product of silver mining) and the

number of shipwrecks found at the bottom of the Mediterranean.

After currency debasement, economy collapsed

Urban population, shipwrecks,

0

100

200

300

400

500

600

700

800

5

BCE

4

BCE

3

BCE

2

BCE

1

BCE

1

CE

2

CE

3

CE

4

CE

5

CE

shipwrecks,

city

size

0

2

4

6

8

10

12

14

total

urban

population

shipwrecks size of biggest city, tsd total urban population, mn

Source: http://www.historum.com/

World lead production recovered 1500 years later

World lead production

0

10

20

30

40

50

60

70

80

90

100

750

BCE

650

BCE

550

BCE

450

BCE

350

BCE

250

BCE

150

BCE

50

BCE

50

CE

150

CE

250

CE

350

CE

450

CE

550

CE

650

CE

750

CE

850

CE

950

CE

1050

CE

1150

CE

1250

CE

1350

CE

1450

CE

1550

CE

1650

CE

1750

CE

Source: http://www.historum.com/

Exactly at a time when the Roman Empire began the strong debasement of its

currency, China faced the start of the Yellow Turban Rebellion (184-205 CE).

This rebellion was caused by the corruption of government officials, peasants

losing their land, high taxes, and forced labor on grand state construction

projects. While the rebellion was eventually defeated, the military leaders and

local administrators gained self-governing powers in the process. This

hastened the collapse of the Han Dynasty in 220. In the aftermath of the revolt

and the fall of the ruling dynasty, China suffered economic collapse. The

population decreased from 50mn in the late 2

nd

century CE to 7.5mn in 280

CE.

5. Erste Group Research

CEE Special Report: Trade between China and the West

30 November 2012

Erste Group Research – Trade between China and the West: three historical highlights Page 5

It should be noted that there are at least four recognized theories about the

demise of Rome. The negative trade balance with China and resulting outflow

of precious metals from Rome was one of the contributing factors. The one

thing that is clear is that Romans could not keep up with rising military

expenses, while the Han Empire collapsed due to civil unrest. The next period

when trade between Western World and China resumed on large levels, was

not until the 18

th

century.

Episode 2: China, Europe and Opium Wars,

1757-1860

With the development of shipbuilding technologies, Western nations greatly

expanded trade across the globe. China again came into focus, especially for

Britain, which saw high demand for Chinese products. The first trade that

existed with China was for silks, porcelain ("fine china") and, most lucratively,

tea. China continued to restrict trade with Western Nations based on the age-

old view of China being prosperous and self-sufficient. The ruling Qing

Dynasty viewed foreign trade with suspicion.

“Our land is so wealthy and prosperous, that we possess all things. Therefore

there is no need to exchange the produce of foreign barbarians for our

own…China is the centre of the world and has everything we could ever need

and that all Chinese products were to be bought with Silver.”

Chinese Emperor Qianlong (1711-1799 CE)

China implemented the so-called Canton System in 1757. The Canton System

limited the ports in which European traders could do business with China. It

also forbade any direct trade between European merchants and Chinese

civilians. Instead, the Europeans, generally employees of major trading

companies (most importantly the British East India Company) had to trade

with an association of Chinese merchants known as the Cohong. The Cohong

was a Guild of thirteen merchants authorized by the Chinese Central

Government to handle trade, particularly rights to trade tea and silk, with the

West. They were the only group at the time authorized to do this, making them

the main controllers of all foreign trade in the nation.

The Canton System limited trade to only one port and exclusively with

the government appointed guild of merchants

The canton system ports, 1757-1842

Source: Wikipedia

China’s official policy was to

allow only payments with silver

and gold for exported products

Chine restricted trade to only

one ports of Macau and Hong

Kong

6. Erste Group Research

CEE Special Report: Trade between China and the West

30 November 2012

Erste Group Research – Trade between China and the West: three historical highlights Page 6

Britain had been on the gold standard since the 18

th

century, so it had to

purchase silver from continental Europe and Mexico to supply the Chinese

appetite for silver. The British East India Company faced a trade imbalance in

favor of China and invested heavily in opium production to redress the

balance. British and US merchants brought opium from the British East India

Company's factories in Patna and Benares, in the Bengal Presidency of

British India, to the coast of China, where they sold it to Chinese smugglers

who distributed the drug in defiance of Chinese laws. Aware both of the drain

of silver and the growing numbers of addicts, the Daoguang Emperor

demanded action. Officials who advocated legalization of the trade in order to

tax it were defeated by those who advocated suppression. In 1838, the

Emperor officials came to Guangzhou where they arrested Chinese opium

dealers and summarily demanded that foreign firms turn over their stocks.

When they refused, China stopped trade altogether and placed the foreign

residents under virtual siege, eventually forcing the merchants to surrender

their opium to be destroyed. In response, the British government sent

expeditionary forces from India, which ravaged the Chinese coast and

dictated the terms of settlement.

Britain had huge trade balance deficit with China

British East India Trade company balance

0

1

2

3

4

5

6

1761

1766

1771

1776

1781

1786

1791

1796

1801

1806

1811

1816

1821

1826

1831

Exports Imports

mn. pounds

Source: Wikipedia

British and American merchants sold opium to

compensate for the outflow of gold and silver

Opium Exports per capita from India to China

(in number of chests)

Source: http://www.nber.org/

The Chinese emperor failed to see the wisdom of his ancestors back in the

times of Han Empire, who allowed trade with West because they feared its

military power. Because they had prohibited imports and were thus deprived

of modern military technologies developed in the West, China lost the war to

Britain. The Treaty of Nanking, which ended the war, opened the way for

further opium trade, but ceded territory, including Hong Kong. The treaty

abolished the monopoly of the Thirteen Factories on foreign trade and instead

five ports were opened for trade, where Britons were allowed to trade with

anyone they wished. However, Chinese officials continued to obstruct foreign

trade, which led to the Second Opium War (1856-1860). The final Treaty of

Tientsin was signed with the following key points:

•Eleven more Chinese ports would be opened for foreign trade

•Right of foreign vessels, including warships, to navigate freely on Yangtze

River

•Right of foreigners to enter internal regions of China for purpose of travel,

trade or missionary activities.

Due to ban on legal imports,

Western merchants started

selling opium to compensate

for outflow of gold

China banned all trade, which

led to war with Britain in 1839

Lacking modern military

technology, China lost two

consecutive wars to Britain

China gave up Hong Kong and

allowed trade with West

7. Erste Group Research

CEE Special Report: Trade between China and the West

30 November 2012

Erste Group Research – Trade between China and the West: three historical highlights Page 7

The loss of two consecutive wars, the widening technological gap with

Western nations and increasing number of drug addicts came to be known as

The Century of Humiliation. The Century of Humiliation was one of the main

themes in the propaganda of the nationalist and communist movements which

later toppled the Qing dynasty in the 1920s. China regained Hong Kong from

Britain in 1997 and Macau from Portugal in 1999. These are now the only two

Special Administrative Regions of China. With the return of key trading ports,

China immediately experienced a new trade boom with the West. Thus began

the third period of trade expansion of the Western World with China, a period

through which we are currently living.

Episode 3: China, EU and United States,

2000-now

Immediately after Hong Kong joined China, trade between Western nations

and China exploded. Chinese exports rose 2.5 fold from the 1990s to 2000s

(adjusted for US inflation). During the next decade, the exports growth rate

doubled compared to that of the ’90s.

Since 2000, China’s exports growth accelerated

China’s exports

0

100

200

300

400

500

600

700

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

Source: IMF

Western nations ran into large trade deficits, Asian

economies went into big surpluses

Current account balance

-600

-500

-400

-300

-200

-100

0

100

200

300

400

500

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

Advanced economies Developing Asia

USD bn, adjusted for US CPI

Source: IMF

Export growth has been largely stimulated by government intervention. The

Chinese government has implemented artificial obstacles for rural areas: bans

on loans to municipalities and small enterprises, social care only made

available for those living in cities. This gave great advantages to companies in

large cities, who could use cheap workforce to actively compete on foreign

markets. Additionally, the Chinese government has kept its currency

exchange rate artificially low to make sure that its exports are price

competitive, while few imports come into country and large savings are made.

With the surge in savings, China has been making vast investments in

infrastructure. These investments often include large-scale projects such as

dams, roads, bridges and vast amounts of social housing. The investment

share of the Chinese economy has rapidly expanded, while household income

growth has been lagging behind GDP. The model of favoring cheap exports

and trade balance surpluses has been copied by other Asian economies, but

typically not to such an extreme extent.

China regained Hong Kong

from Britain in 1997, new trade

boom with the West started

Chinese government artificially

stimulated exports while

limiting imports

8. Erste Group Research

CEE Special Report: Trade between China and the West

30 November 2012

Erste Group Research – Trade between China and the West: three historical highlights Page 8

Investments took greater share of GDP in China

Investments, % of GDP, China

25%

27%

29%

31%

33%

35%

37%

39%

41%

43%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Source: IMF

China became world leader in savings

China’s FX reserves

0

500

1000

1500

2000

2500

3000

3500

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

USD bn

Source: IMF

Money no longer means gold, as the USD has taken over this role. For the

third time in history, China has become the leader in global savings of the

main means of exchange. The country currently possesses the largest stock

of foreign exchange reserves, worth USD 3.2trn. Quite symbolically, in 2012,

China is likely to become a leader in global gold consumption for the first time

since the 19

th

century. The huge bulk of Chinese FX reserves are by their

nature either deposits in commercial banks or loans to governments in other

countries. Chinese savings made it much easier for banks and governments

to get cheap funding. Chinese savings may well have contributed to the

deteriorating asset quality and lower standards of credit in Western countries.

In addition, competition with cheaper imports from Asia made life difficult for

many businesses in the developed world. Chinese demand for investments,

particularly in the construction sector, has pushed up commodity prices and

further widened the trade deficit in more advanced economies. China’s rising

savings and their likely contribution to the banking crisis of 2008/09 were

definitely not the sole reasons for the Great Recession. The economic crisis of

the recent years is a broad and complicated phenomenon. But the rising trade

deficit between West and East was one of the imbalances that likely facilitated

the economic downturn.

Lucrative lending soared in US since negative trade

balance with China expanded

US subprime mortgages, USD bn

Source: http://emlab.berkeley.edu/

Energy prices skyrocketed on growing demand

from China

Energy price index

0

50

100

150

200

250

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

Source: IMF

China is again global leader in

savings

Rising trade deficit between

West and East was an

imbalance that likely facilitated

economic downturn

9. Erste Group Research

CEE Special Report: Trade between China and the West

30 November 2012

Erste Group Research – Trade between China and the West: three historical highlights Page 9

Summary

There are three known historical periods during which trade between Western

and Eastern worlds has gone though explosive growth (206 BCE-220, 1757-

1860, 2000-now). Each time the West has seen widening trade balance

deficits and China ran trade surpluses. During three historical periods of

expanding trade, China become the global leader in savings of the main

global medium of exchange (be it gold, silver or the reserve currency). China

sustained its positive trade balance via government intervention, which came

at a cost to people’s income. In each of the three episodes, China has used

its proceeds from foreign trade surplus for large-scale construction projects

inside the country. The Great Wall of China and the vast difference between

the prosperity of Hong Kong and Mainland China are remnants of two

previous failures of the West to create sustainable and balanced economic

relations with East. In previous history, no country received greater damage

from China’s restrictions on trade than China itself. The Chinese people were

dissatisfied with their incomes and the whole country lagged in technology

compared to the West. In the past, this has led to revolts in China. Since

2010, the Chinese government declared a change in its policy, promising to

change the economic structure more in favor of domestic consumption.

Should this actually be done, the negative trade balance may diminish and the

West will find much more demand for its products. The EU, United States and

developing Asia may find themselves on the path of great prosperity should

trade become free and thus break the two-thousand-year-old unsustainable

economic model.

During three historical periods

of expanding trade, China

became global leader in

savings of main global medium

of exchange (gold, silver or

reserve currency)

Both EU, United States and

developing Asia may put

themselves on path of great

prosperity should the trade

become free and thus break the

two thousand year old

unsustainable economic model

10. Erste Group Research

CEE Special Report: Trade between China and the West

30 November 2012

Erste Group Research – Trade between China and the West: three historical highlights Page 10

Contacts

Group Research

Head of Group Research

Friedrich Mostböck, CEFA +43 (0)5 0100 11902

Major Markets & Credit Research

Head: Gudrun Egger, CEFA +43 (0)5 0100 11909

Adrian Beck (Fixed income AT, SW) +43 (0)5 0100 11957

Benedikt Blum (Quant, Euro) +43 (0)5 0100 11961

Hans Engel (Equity US) +43 (0)5 0100 19835

Christian Enger, CFA (Covered Bonds) +43 (0)5 0100 84052

Mildred Hager-Germain (Fixed income Euro, US) +43 (0)5 0100 17331

Alihan Karadagoglu (Corporates) +43 (0)5 0100 19633

Peter Kaufmann (Corporates) +43 (0)5 0100 11183

Stephan Lingnau (Equity Europe) +43 (0)5 0100 16574

Elena Statelov, CIIA (Corporates) +43 (0)5 0100 19641

Ronald Stöferle (Equity Asia, Commodities) +43 (0)5 0100 11723

Thomas Unger; CFA (Agencies) +43 (0)5 0100 17344

Macro/Fixed Income Research CEE

Head CEE: Juraj Kotian (Macro/FI) +43 (0)5 0100 17357

Chief Analyst: Birgit Niessner (CEE Macro/FI) +43 (0)5 0100 18781

CEE Equity Research

Head: Henning Eßkuchen +43 (0)5 0100 19634

Chief Analyst: Günther Artner, CFA (CEE Equities) +43 (0)5 0100 11523

Günter Hohberger (Banks) +43 (0)5 0100 17354

Franz Hörl, CFA (Steel, Construction) +43 (0)5 0100 18506

Daniel Lion, CIIA (IT) +43 (0)5 0100 17420

Christoph Schultes, CIIA (Insurance, Utility) +43 (0)5 0100 16314

Vera Sutedja, CFA (Telecom) +43 (0)5 0100 11905

Vladimira Urbankova, MBA (Pharma) +43 (0)5 0100 17343

Martina Valenta, MBA (Real Estate) +43 (0)5 0100 11913

Gerald Walek, CFA (Machinery) +43 (0)5 0100 16360

Editor Research CEE

Brett Aarons +420 956 711 014

Research, Croatia/Serbia

Head: Mladen Dodig (Equity) +381 11 22 09 178

Head: Alen Kovac (Fixed income) +385 62 37 1383

Anto Augustinovic (Equity) +385 62 37 2833

Ivana Rogic (Fixed income) +385 62 37 2419

Davor Spoljar, CFA (Equity) +385 62 37 2825

Research, Czech Republic

Head: David Navratil (Fixed income) +420 224 995 439

Petr Bittner (Fixed income) +420 224 995 172

Head: Petr Bartek (Equity) +420 224 995 227

Vaclav Kminek (Media) +420 224 995 289

Katarzyna Rzentarzewska (Fixed income) +420 224 995 232

Martin Krajhanzl (Equity) +420 224 995 434

Martin Lobotka (Fixed income) +420 224 995 192

Lubos Mokras (Fixed income) +420 224 995 456

Josef Novotný (Equity) +420 224 995 213

Research, Hungary

Head: József Miró (Equity) +361 235 5131

András Nagy (Equity) +361 235-5132

Orsolya Nyeste (Fixed income) +361 373 2026

Zoltan Arokszallasi (Fixed income) +361 373 2830

Research, Poland

Michal Hulboj (Equity) +48 22 330 6253

Marek Czachor (Equity) +48 22 330 6254

Adam Rzepecki (Equity) +48 22 330 6252

Michal Zasadzki (Equity) +48 22 330 6251

Research, Romania

Head: Lucian Claudiu Anghel +40 37226 1021

Head Equity: Mihai Caruntu (Equity) +40 21 311 2754

Dorina Cobiscan (Fixed Income) +40 37226 1028

Dumitru Dulgheru (Fixed income) +40 37226 1029

Eugen Sinca (Fixed income) +40 37226 1026

Raluca Ungureanu (Equity) +40 21311 2754

Marina Alexandra Spataru (Equity) +40 21311 2754

Research Turkey

Head: Can Yurtcan +90 212 371 2540

Evrim Dairecioglu (Equity) +90 212 371 2535

Goker Mustafa Gorkem (Equity) +90 212 371 2534

Sezai Saklaroglu (Equity) +90 212 371 2533

Sevda Sarp (Equity) +90 212 371 2537

Nilufer Sezgin (Fixed income) +90 212 371 2536

Mehmet Emin Zumrut (Equity) +90 212 371 2539

Research, Slovakia

Head: Maria Valachyova, (Fixed income) +421 2 4862 4185

Martin Balaz (Fixed income) +421 2 4862 4762

Research, Ukraine

Head: Maryan Zablotskyy (Fixed income) +38 044 593 9188

Igor Zholonkivskyi (Equity) +38 044 593 1784

Treasury - Erste Bank Vienna

Saving Banks & Sales Retail

Head: Thomas Schaufler +43 (0)5 0100 84225

Equity Retail Sales

Head: Kurt Gerhold +43 (0)5 0100 84232

Fixed Income & Certificate Sales

Head: Uwe Kolar +43 (0)5 0100 83214

Treasury Domestic Sales

Head: Markus Kaller +43 (0)5 0100 84239

Corporate Sales AT

Head: Christian Skopek +43 (0)5 0100 84146

Fixed Income & Credit Institutional Sales

Institutional Sales

Head: Manfred Neuwirth +43 (0)5 0100 84250

Bank and Institutional Sales

Head: Jürgen Niemeier +43 (0)5 0100 85503

Institutional Sales AT, GER, LUX, CH

Head: Thomas Almen +43 (0)5 0100 84323

Margit Hraschek +43 (0)5 0100 84117

Rene Klasen +43 (0)5 0100 85521

Marc Pichler +43 (0)5 0100 84118

Sabine Vogler +43 (0)5 0100 85543

Bank and Savingsbanks Sales

Head: Marc Friebertshäuser +43 (0)5 0100 85540

Bernd Thaler +43 (0)5 0100 85583

Carsten Demmler +43 (0)5 0100 85580

Mathias Gindele +43 (0)5 0100 85562

Andreas Goll +43 (0)5 0100 85561

Ulrich Inhofner +43 (0)50100 85544

Sven Kienzle +43 (0)50100 85541

Manfred Meyer +43 (0)5 0100 83213

Jörg Moritzen +43 (0)5 0100 85581

Michael Schmotz +43 (0)5 0100 85542

Klaus Vosseler +43 (0)5 0100 85560

Institutional Sales CEE

Head: Jaromir Malak +43 (0)50100 84254

Central Bank and International Sales

Head: Christoph Kampitsch +43 (0)50100 84979

Abdalla Bachu +44 207623 4159

Antony Brown +44 207623 4159

Sales CEE

Tomasz Karsznia +48 22 538 6281

Pawel Kielek +48 22 538 6223

Piotr Zagan +43 (0)50100 84256

Institutional Sales Slovakia

Head: Peter Kniz +421 2 4862 5624

Sarlota Sipulova +421 2 4862 5629

Institutional Sales Czech Republic

Head: Ondrej Cech +420 2 2499 5577

Milan Bartos +420 2 2499 5562

Radek Chupik +420 2 2499 5565

Pavel Zdichynec +420 2 2499 5590

Institutional Sales Croatia

Antun Buric +385 (0)6237 2439

Institutional Sales Hungary

Norbert Siklosi +36 1 235 584

Institutional Sales Romania

Head: Ciprian Mitu +40 213121199 6200

Ruxandra Carlan +40 21 310-4449 612

Institutional Solutions and PM

Head: Zachary Carvell +43 (0)50100 83308

Brigitte Mayr +43 (0)50100 84781

Mikhail Roshal +43 (0)50100 84787

11. Erste Group Research

CEE Special Report: Trade between China and the West

30 November 2012

Erste Group Research – Trade between China and the West: three historical highlights Page 11

Published by Erste Group Bank AG, Neutorgasse 17, 1010 Vienna, Austria.

Phone +43 (0)5 0100 - ext.

Erste Group Homepage: www.erstegroup.com On Bloomberg please type: EBS AV and then F8 GO

This publication has been prepared by EG Research. This report is for information purposes only.

Publications in the United Kingdom are available only to investment professionals, not private customers, as defined by the rules of the

Financial Services Authority. Individuals who do not have professional experience in matters relating to investments should not rely on it.

The information contained herein has been obtained from public sources believed by EGB to be reliable, but which may not have been

independently justified. No guarantees, representations or warranties are made as to its accuracy, completeness or suitability for any purpose.

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument or any other action and will not form

the basis or a part of any contract.

Neither EGB nor any of its affiliates, its respective directors, officers or employers accepts any liability whatsoever (in negligence or otherwise)

for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection therewith. Any opinion, estimate

or projection expressed in this publication reflects the current judgement of the author(s) on the date of this report. They do not necessarily

reflect the opinions of EGB and are subject to change without notice. EGB has no obligation to update, modify or amend this report or to

otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein,

changes or subsequently becomes inaccurate.

The past performance of financial instruments is not indicative of future results. No assurance can be given that any financial instrument or

issuer described herein would yield favourable investment results.

EGB, its affiliates, principals or employees may have a long or short position or may transact in the financial instrument(s) referred to herein or

may trade in such financial instruments with other customers on a principal basis. EGB may act as a market maker in the financial instruments

or companies discussed herein and may also perform or seek to perform investment banking services for those companies. EGB AG may act

upon or use the information or conclusion contained in this report before it is distributed to other persons.

This report is subject to the copyright of EGB. No part of this publication may be copied or redistributed to persons or firms other than the

authorised recipient without the prior written consent of EGB.

By accepting this report, a recipient hereof agrees to be bound by the foregoing limitations.

Copyright: 2012 EGB AG. All rights reserved.

Please refer to www.erstegroup.com for the current list of specific disclosures and the breakdown of Erste Group’s investment recommendations.