Downloaded 41 times

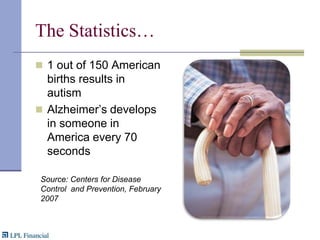

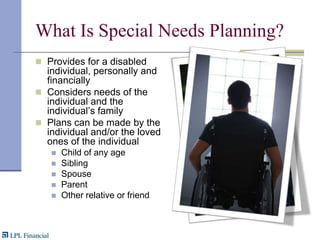

The document outlines the fundamentals of special needs planning, emphasizing the importance of addressing the care and financial security of individuals with disabilities. It provides statistics highlighting the prevalence of disabilities in the U.S. and details a step-by-step planning process that includes creating care plans, legal arrangements, and financial strategies. The document also explains various types of special needs trusts that can protect government benefits while providing for disabled individuals.