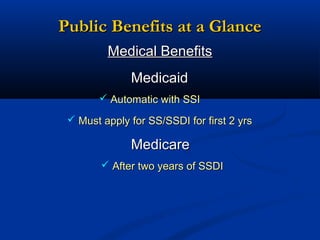

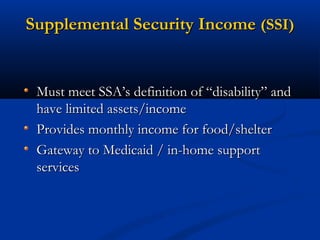

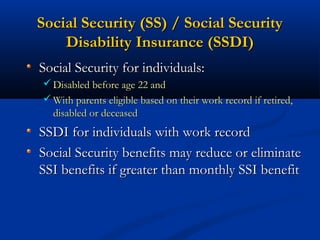

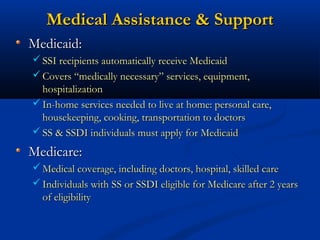

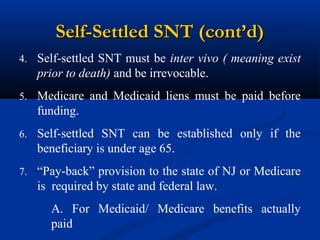

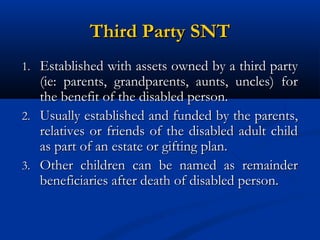

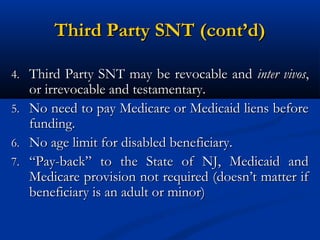

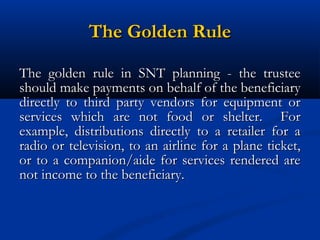

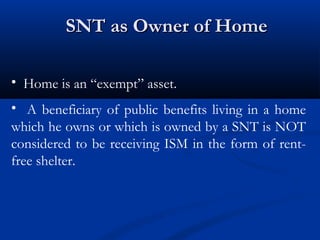

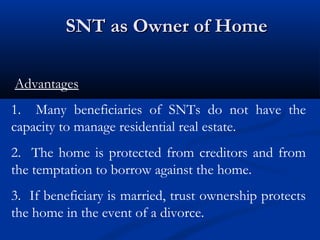

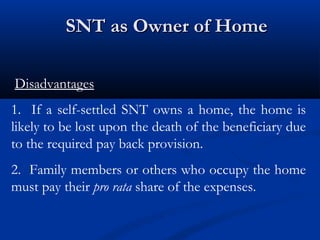

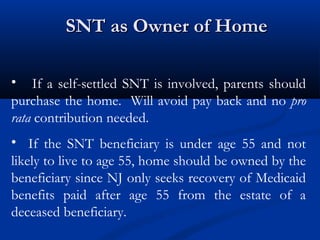

The document discusses essential planning for individuals with special needs, particularly focusing on estate planning for their parents. It outlines the significance of public benefits, the role of special needs trusts (SNTs), and strategic financial management to ensure long-term security and quality of life for individuals with disabilities. Moreover, it details various types of trusts, their implications for public benefits eligibility, and the importance of legal guidance in establishing effective financial plans.