Download to read offline

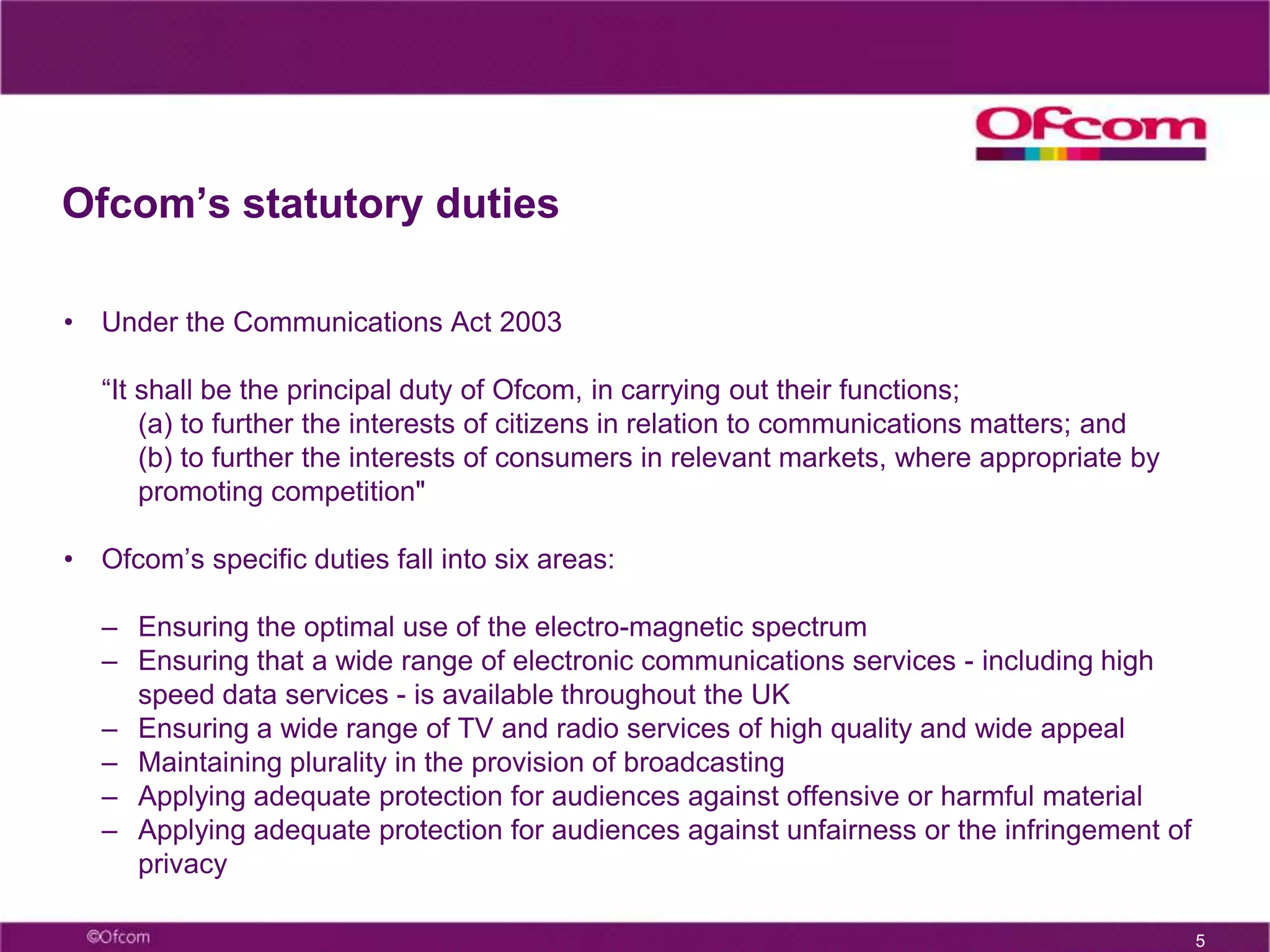

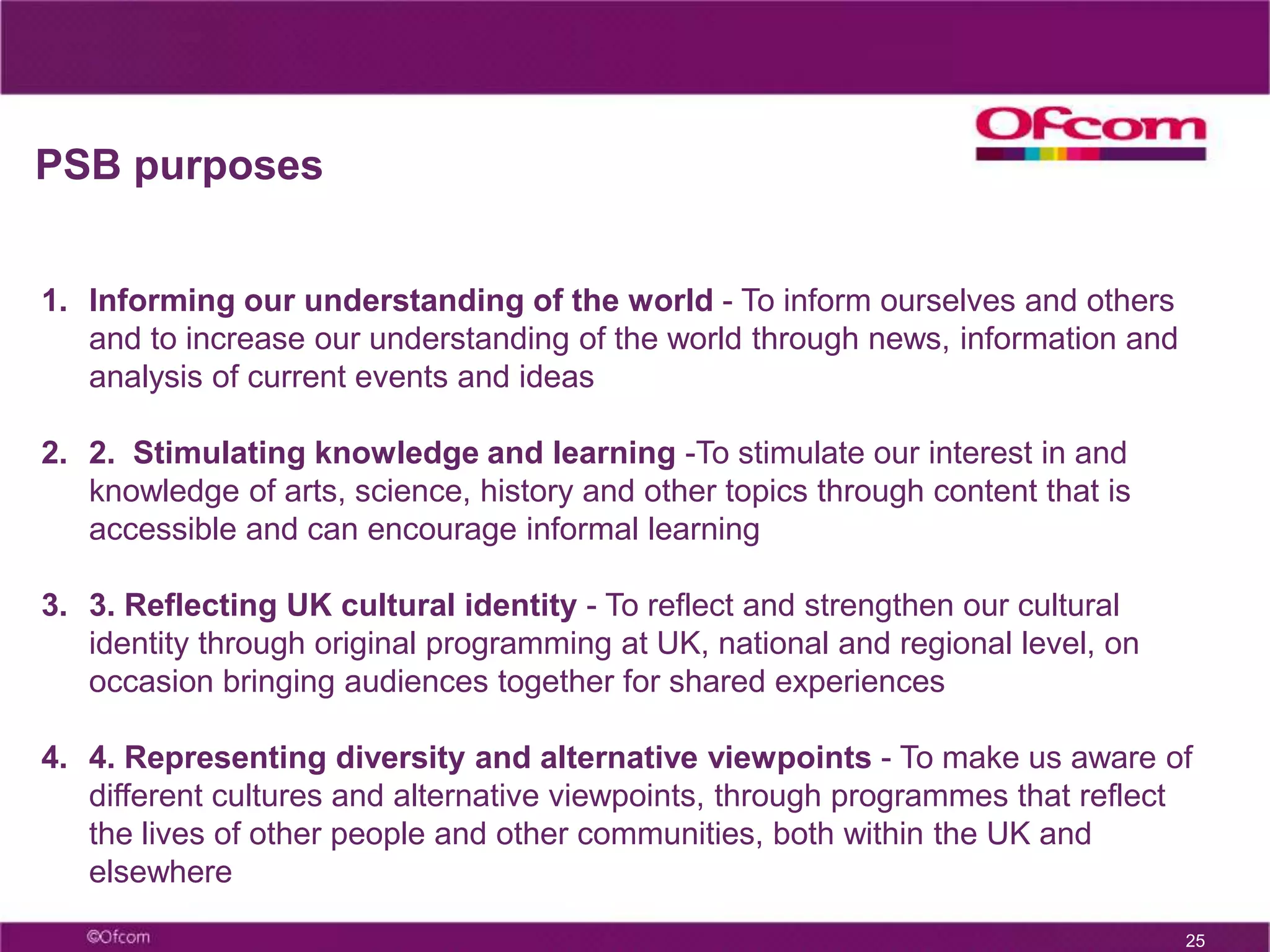

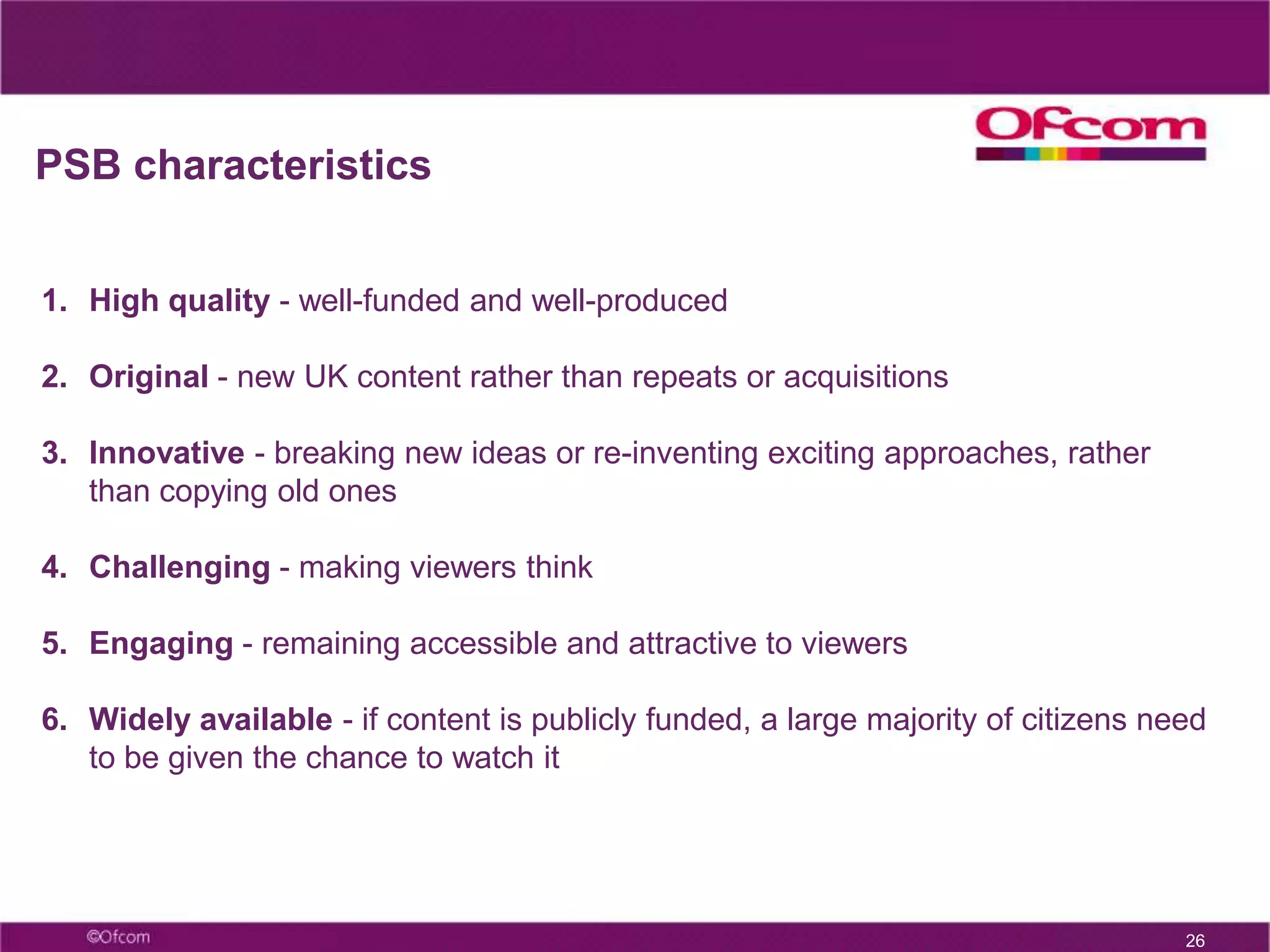

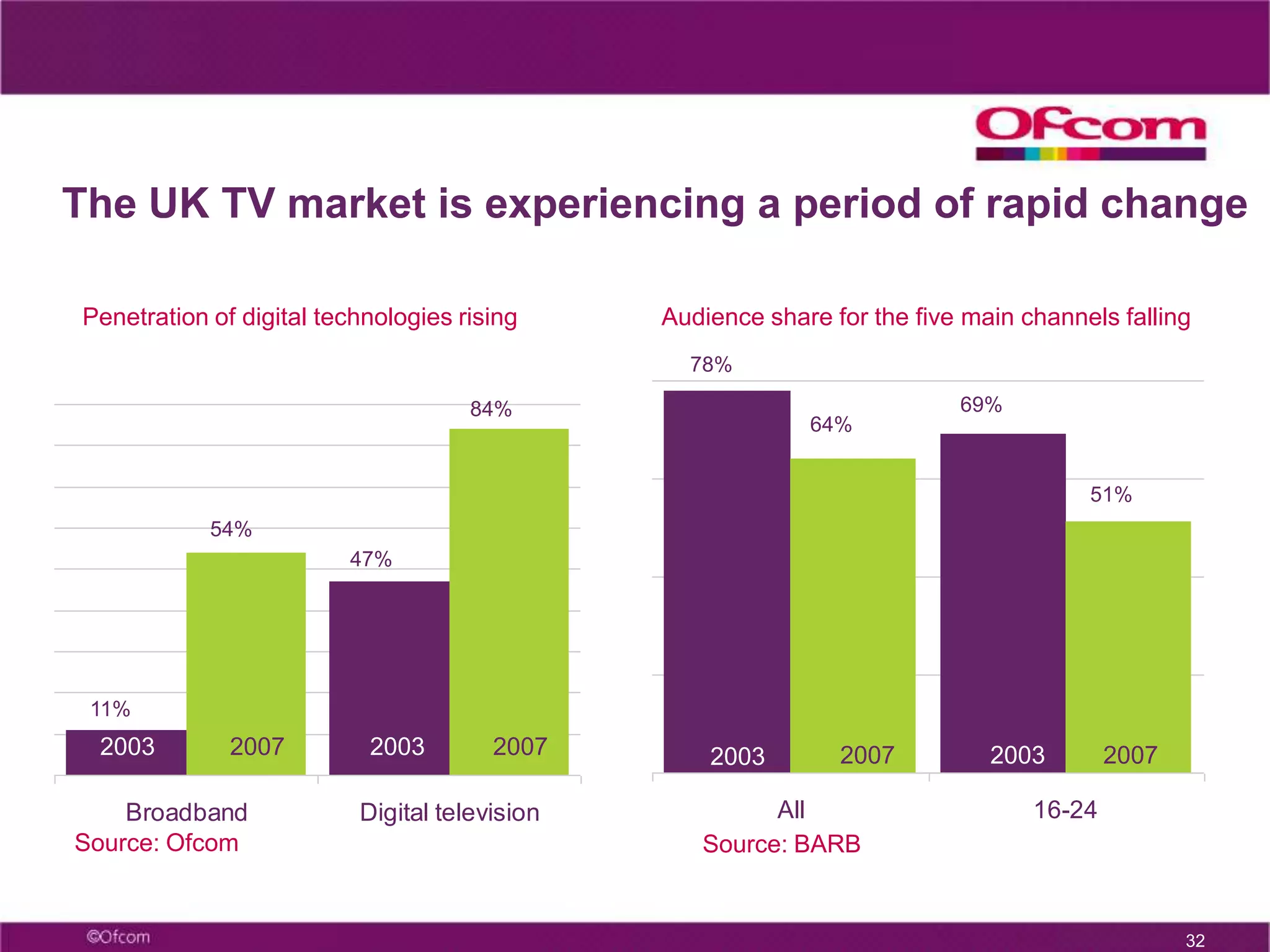

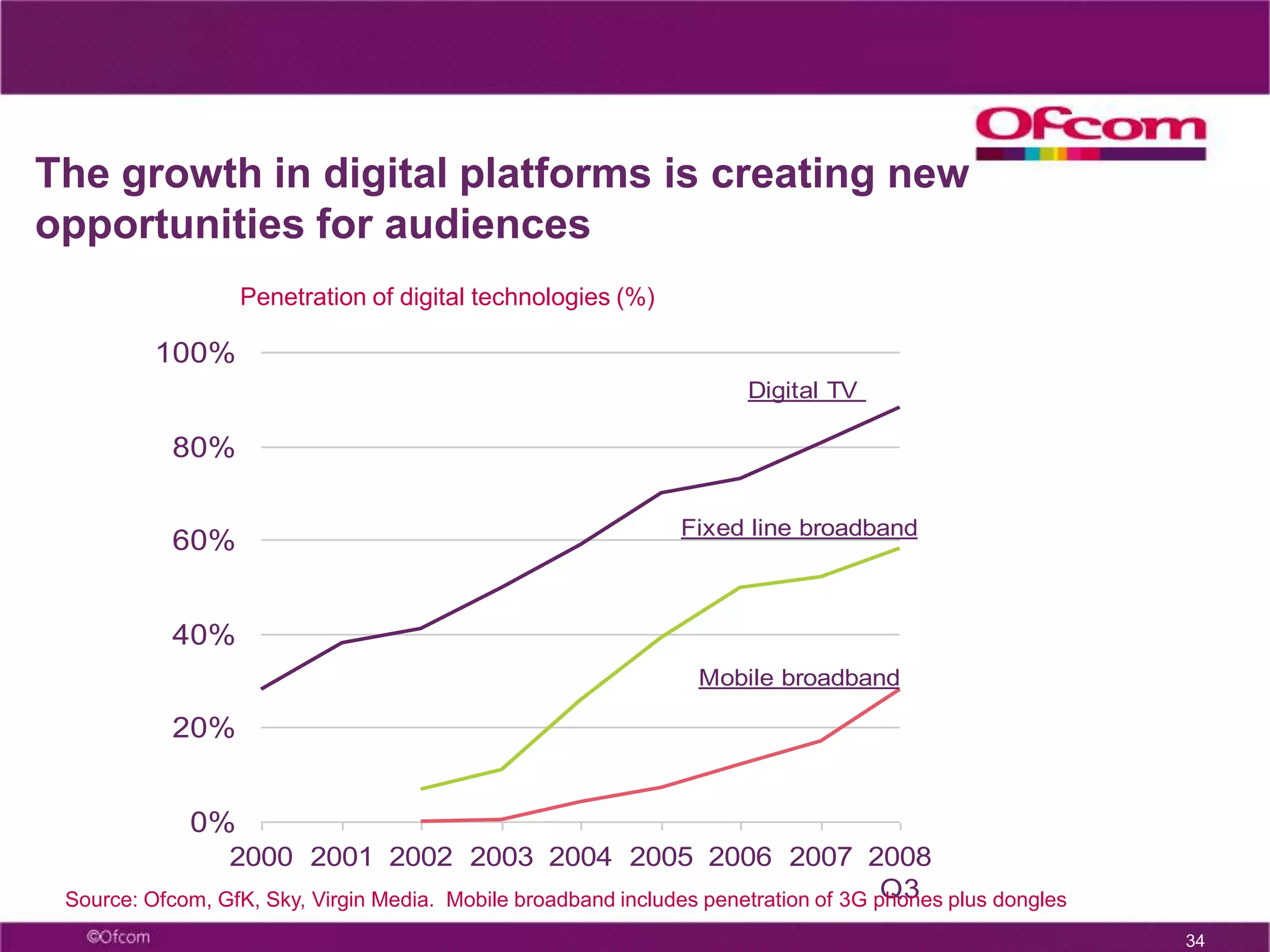

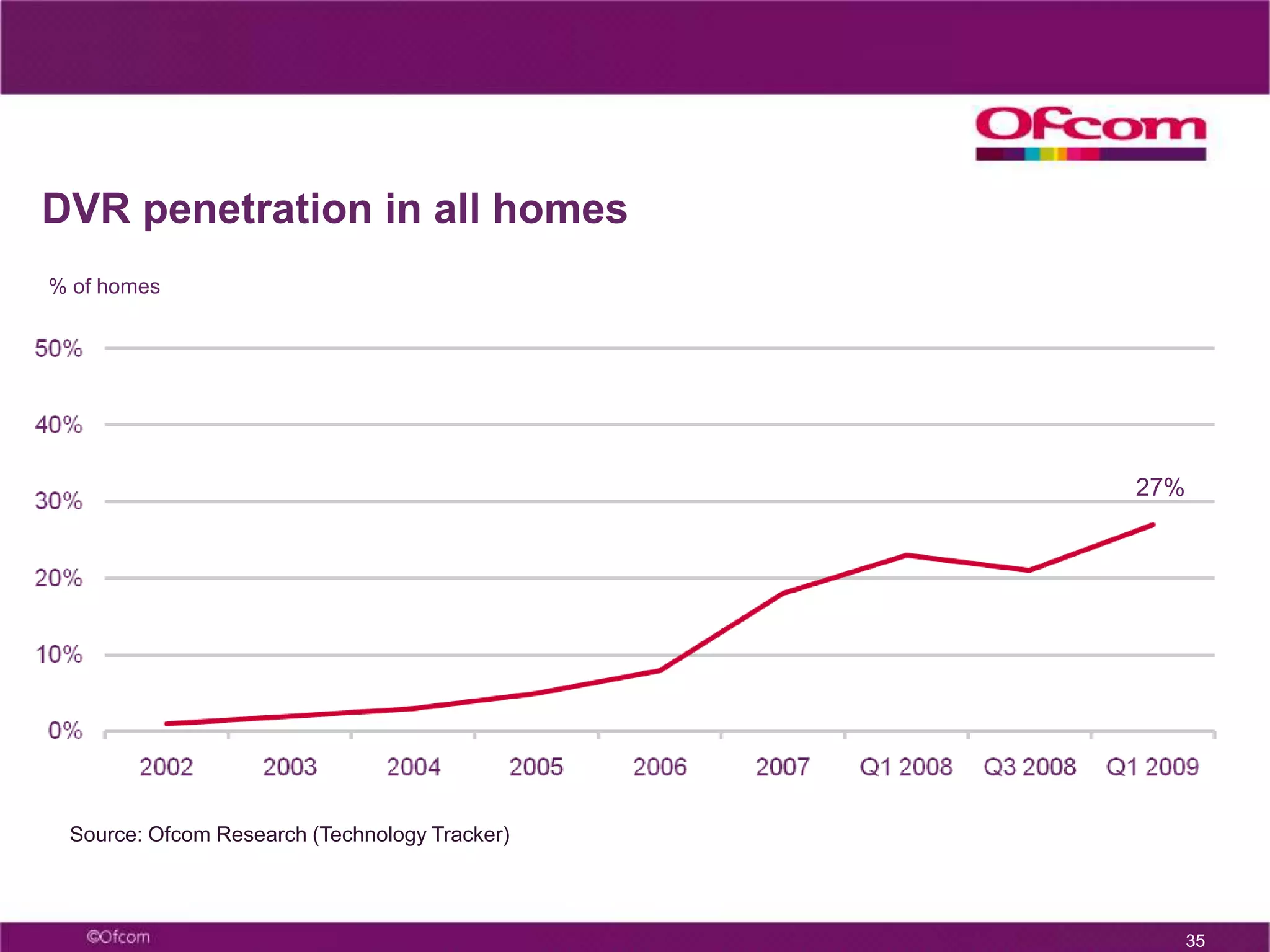

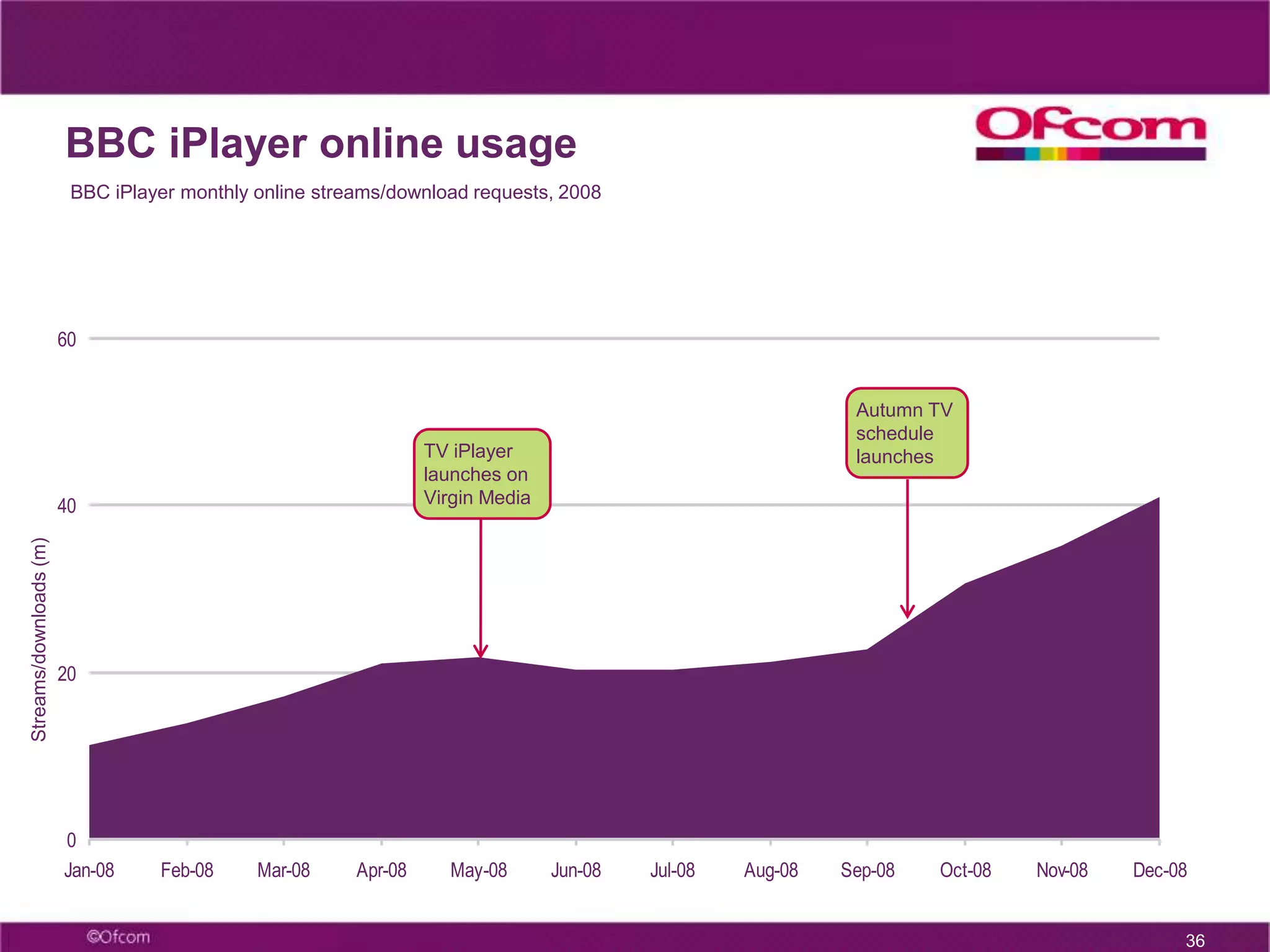

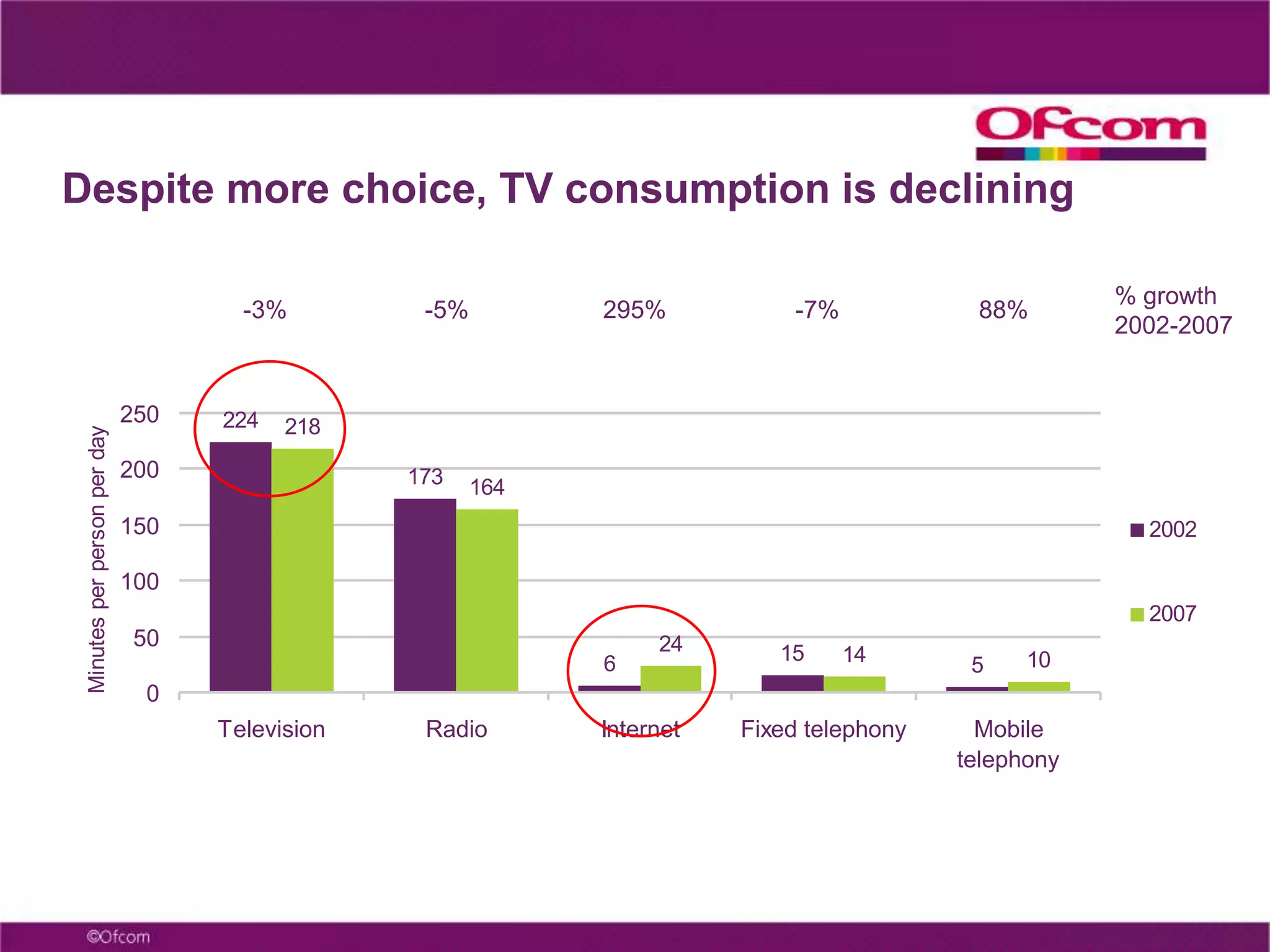

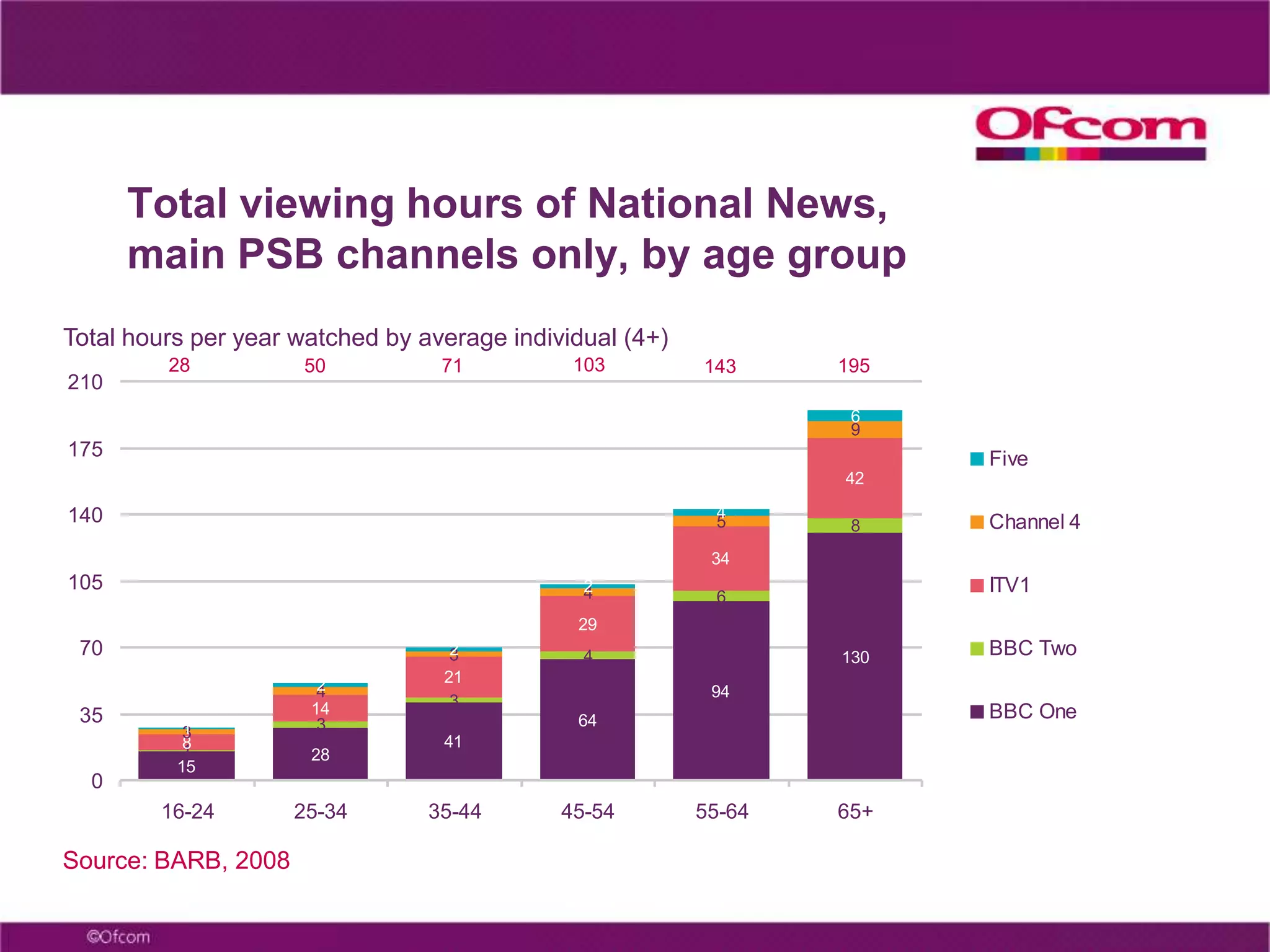

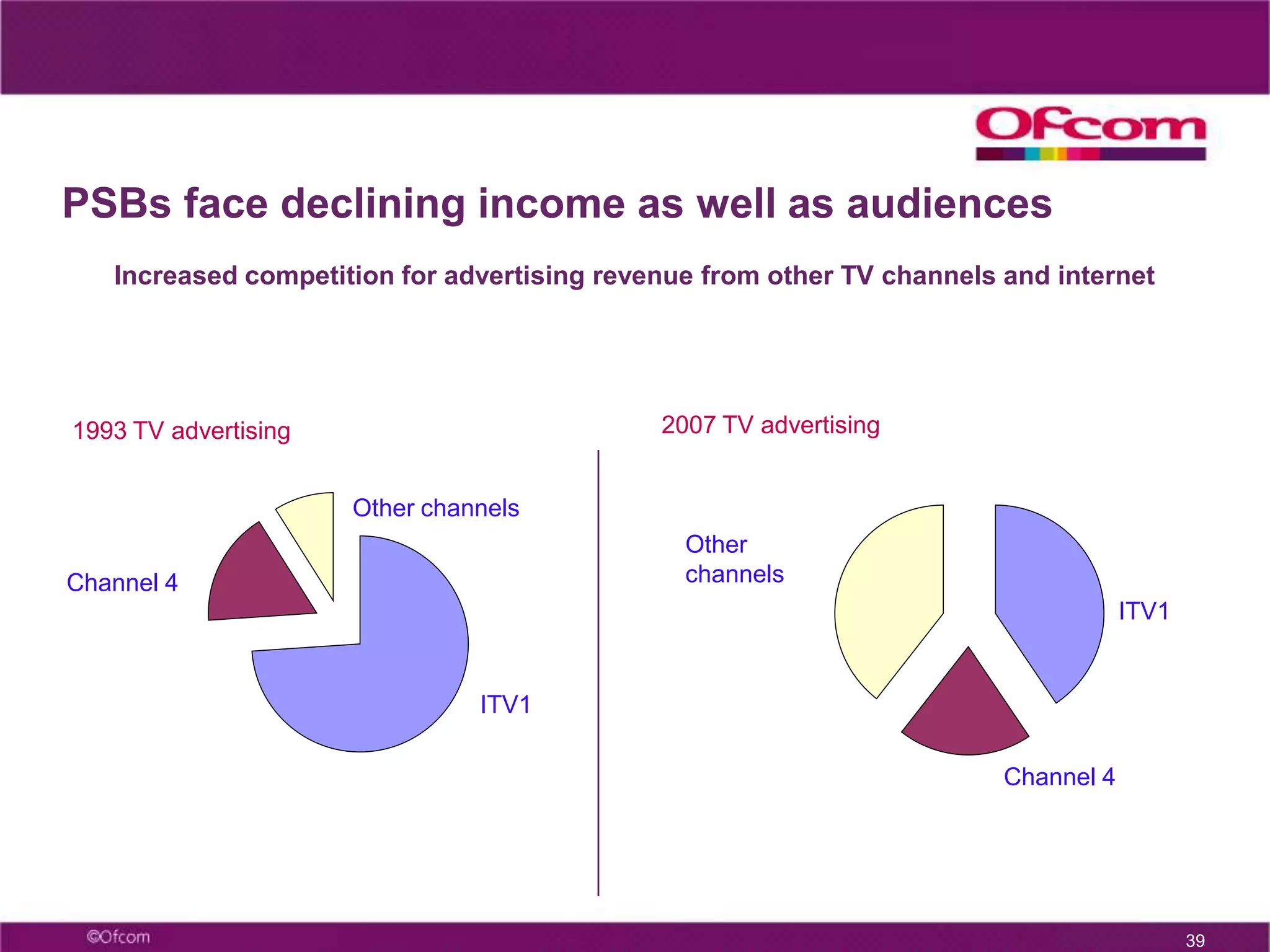

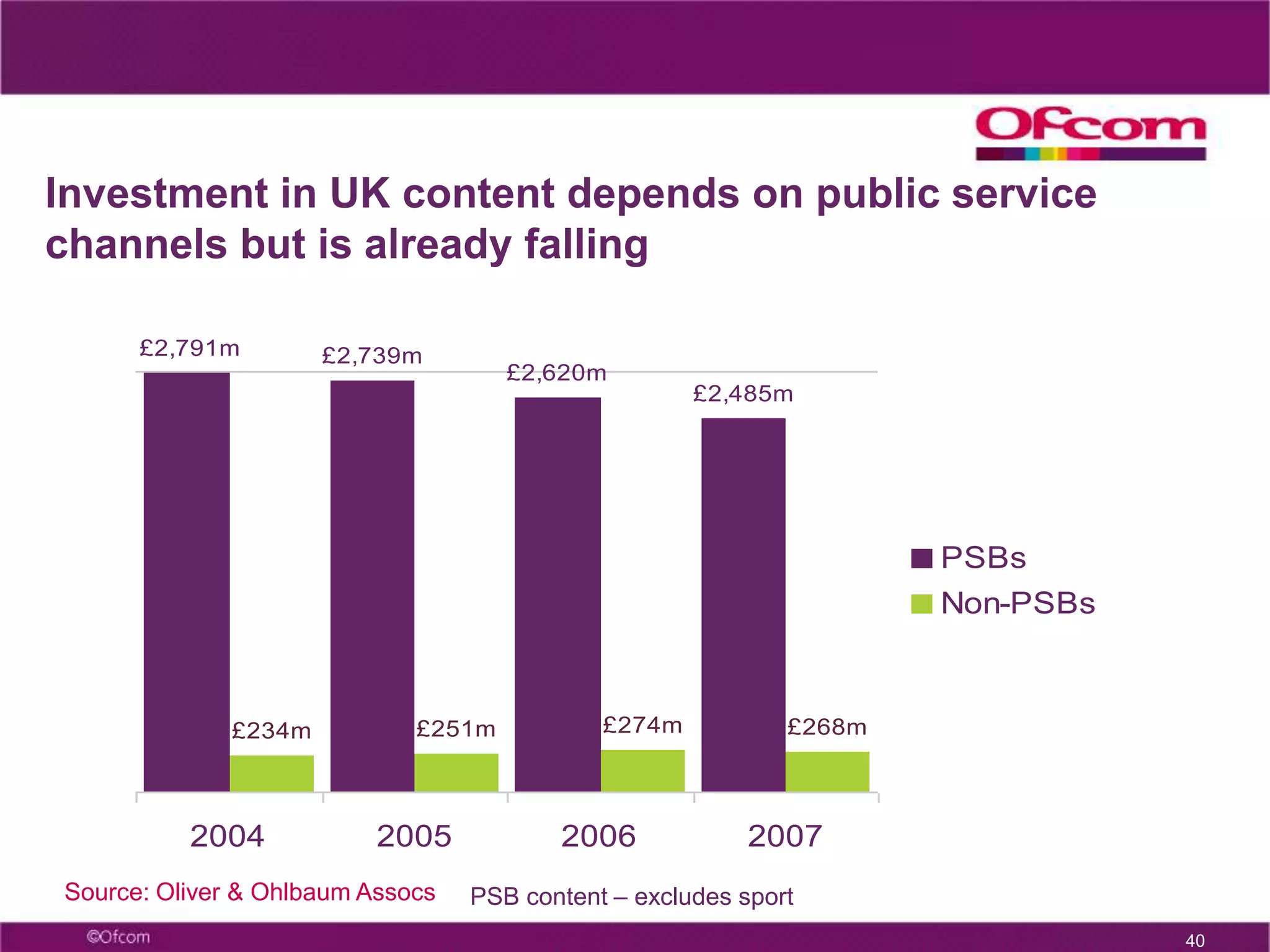

The document summarizes key points from a presentation given by Damian Radcliffe at Birmingham City University on November 26, 2009. The presentation covered Ofcom's role as the UK communications regulator, the state of the communications market, issues around public service broadcasting, local media, and the Digital Economy Bill. It provided an overview of Ofcom's duties and focus areas, trends in digital technologies, challenges facing public service broadcasters, and the goals and main elements of the Digital Economy Bill.

![Coded Agents – with UiPath SDK + LangGraph [Virtual Hands-on Workshop]](https://cdn.slidesharecdn.com/ss_thumbnails/codedagentsdeck-251215155422-5497c599-thumbnail.jpg?width=640&height=640&fit=bounds)