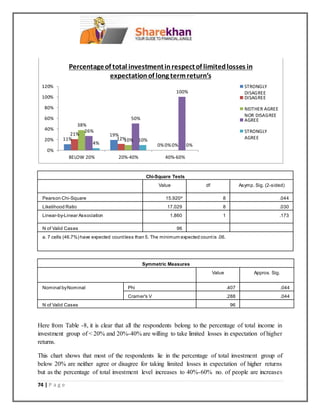

This document is a summer internship project report on analyzing investment patterns based on investors' risk profiles. It includes an introduction to the topic, definitions of key terms like risk, investment, and risk profiles. It also outlines the objectives, research methodology, data analysis and findings of the study conducted with Sharekhan Limited on how demographic and risk-related factors influence individuals' investment decisions and patterns.