Downloaded 57 times

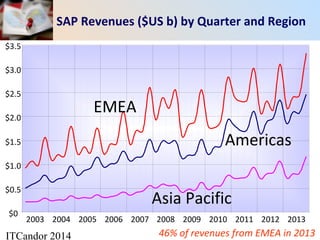

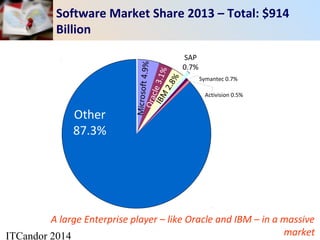

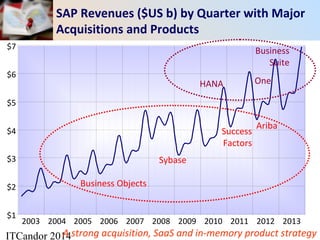

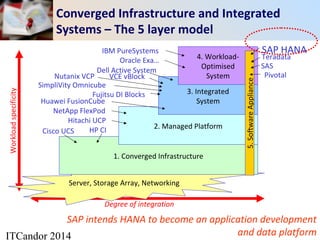

This document discusses SAP's strategy and market position. It notes that SAP has traditionally focused on European corporate workloads but is expanding into new areas like converged infrastructure, in-memory computing, and cloud services. The document analyzes SAP's financials, industry focus, major acquisitions, and growth areas like HANA and cloud. It argues that SAP's strategy of building HANA into an application and data platform while offering hybrid cloud services represents an idiosyncratic approach for the company to address the modern market.