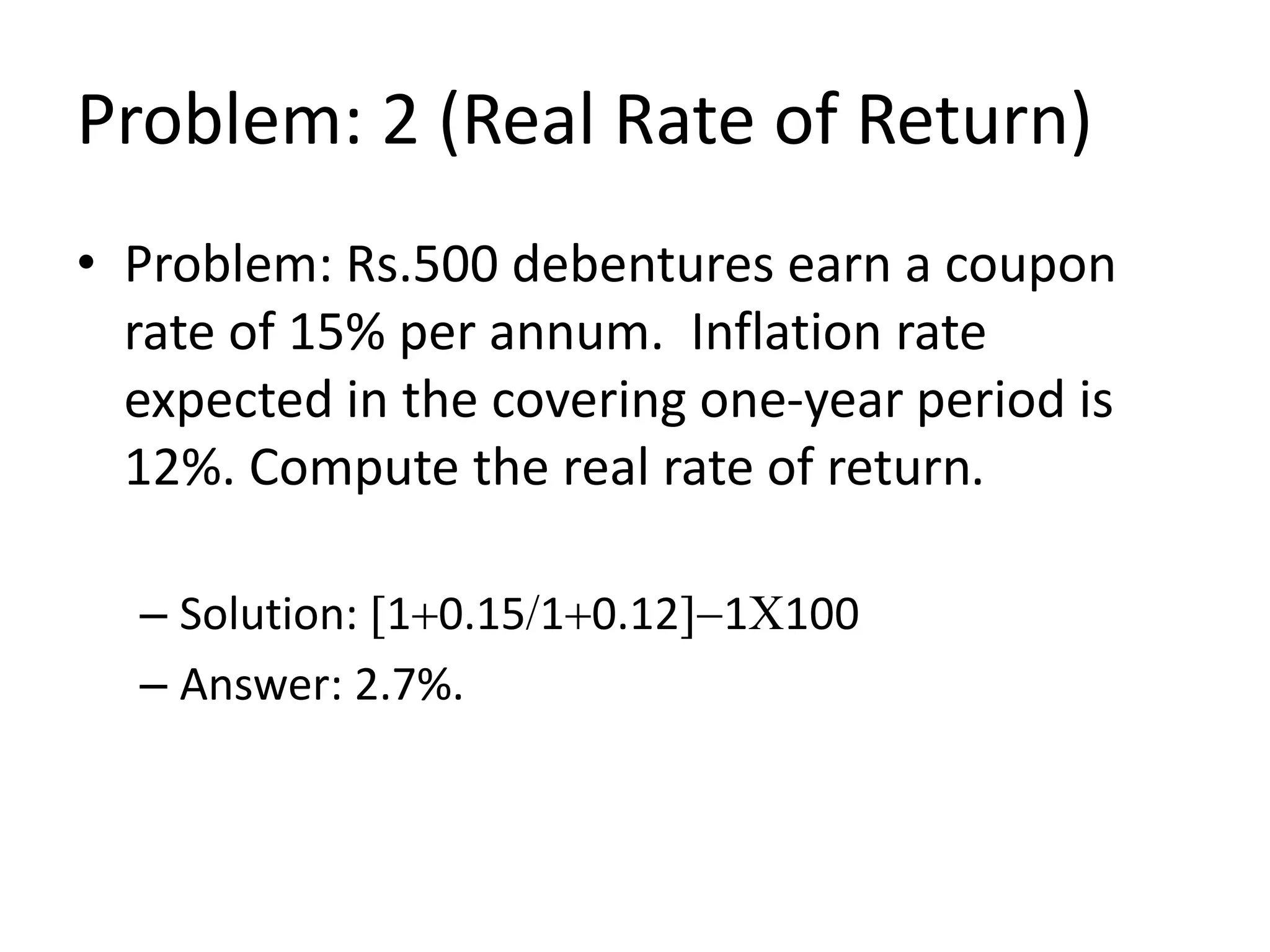

The document discusses risk and return in investments. It defines risk as the possibility of loss or variability in returns. It notes that risk and return are positively correlated, so higher risk investments like stocks generally offer higher returns than lower risk ones like bonds. It identifies two main components of risk: systematic risk that affects the overall market and unsystematic risk that is specific to a particular company. Common types of systematic risk include market risk, interest rate risk and inflation risk, while business and financial risk are examples of unsystematic risk. The document also provides examples of how to calculate expected returns, standard deviation of returns as a risk measure, and real rates of return adjusted for inflation.