Roubini's Crisis Hypothesis

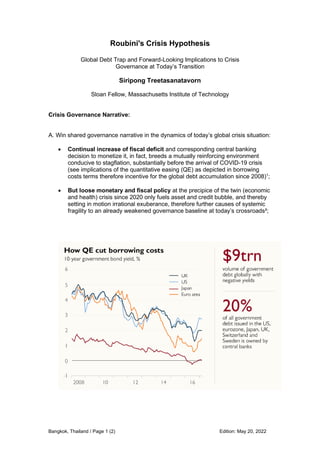

Roubini's Crisis Hypothesis: Global Debt Trap and Forward-Looking Implications to Crisis Governance at Today’s Transition Crisis Governance Narrative: • Continual increase of fiscal deficit and corresponding central banking decision to monetize it, in fact, breeds a mutually reinforcing environment conducive to stagflation, substantially before the arrival of COVID-19 crisis (see implications of the quantitative easing (QE) as depicted in borrowing costs terms therefore incentive for the global debt accumulation since 2008); • But loose monetary and fiscal policy at the precipice of the twin (economic and health) crisis since 2020 only fuels asset and credit bubble, and thereby setting in motion irrational exuberance, therefore further causes of systemic fragility to an already weakened governance baseline at today’s crossroads; • Confidence in the market and the policy is a key decisive determinant, essentially with structural capabilities to manage and overcome the ongoing supply-side challenge, considering in particular political resolve accompanied by collective rational decision, required to address the ongoing balkanization between sovereign nations in the web of global trade and financial systems; • Such is an important caveat at the crisis transition notably together with shared global priorities on the premise of broad-based capabilities to sustain the level of global/national debt without adding further cost to the supply side, while also maneuvering remaining resources and thereby re-establishing the equilibrium that best reflects the reality on the ground until the crisis subsides; • Structural transition over debt-trap challenges is, above all, an imperative required to reconstitute a good and constructive decision-making highground, with shared conscience of how and why the global economy shall serve the purpose only as long as we are all aware of its raison d'être, that is, better or worse, a function of collective reflection upon one's rational and moral choice.

Recommended

Recommended

More Related Content

Similar to Roubini's Crisis Hypothesis

Similar to Roubini's Crisis Hypothesis (20)

More from Siripong Treetasanatavorn

More from Siripong Treetasanatavorn (20)

Recently uploaded

Recently uploaded (13)

Roubini's Crisis Hypothesis

- 1. Bangkok, Thailand / Page 1 (2) Edition: May 20, 2022 Roubini's Crisis Hypothesis Global Debt Trap and Forward-Looking Implications to Crisis Governance at Today’s Transition Siripong Treetasanatavorn Sloan Fellow, Massachusetts Institute of Technology Crisis Governance Narrative: A. Win shared governance narrative in the dynamics of today’s global crisis situation: • Continual increase of fiscal deficit and corresponding central banking decision to monetize it, in fact, breeds a mutually reinforcing environment conducive to stagflation, substantially before the arrival of COVID-19 crisis (see implications of the quantitative easing (QE) as depicted in borrowing costs terms therefore incentive for the global debt accumulation since 2008)1 ; • But loose monetary and fiscal policy at the precipice of the twin (economic and health) crisis since 2020 only fuels asset and credit bubble, and thereby setting in motion irrational exuberance, therefore further causes of systemic fragility to an already weakened governance baseline at today’s crossroads²;

- 2. S. Treetasanatavorn. Roubini’s Crisis Hypothesis Edition: May 20, 2022 Bangkok, Thailand / Page 2 (2) B. Focus on key strategic priorities with mutually reinforcing impact on a global scale: • Confidence in the market and the policy is a key decisive determinant, essentially with structural capabilities to manage and overcome the ongoing supply-side challenge, considering in particular political resolve accompanied by collective rational decision, required to address the ongoing balkanization between sovereign nations in the web of global trade and financial systems3 ; • Such is an important caveat at the crisis transition notably together with shared global priorities on the premise of broad-based capabilities to sustain the level of global/national debt without adding further cost to the supply side, while also maneuvering remaining resources and thereby re-establishing the equilibrium that best reflects the reality on the ground until the crisis subsides; C. Lead the transition on reciprocal decision highgrounds with shared commonsense: • Structural transition over debt-trap challenges is, above all, an imperative required to reconstitute a good and constructive decision-making highground, with shared conscience of how and why the global economy shall serve the purpose only as long as we are all aware of its raison d'être, that is, better or worse, a function of collective reflection upon one's rational and moral choice. References (in appearance order): 1. See Nouriel Roubini's Op-ed via Project Syndicate and The Guardian (2021): https://www.theguardian.com/business/2021/jul/02/1970s-stagflation-2008-debt- crisis-global-economy; See also discussion of quantitative easing and implications to the borrowing costs from The Times (2017); Refer to the image source at: https://www.thetimes.co.uk/article/what-happens-when-the-tap-is-turned-off-lzt2pcq3n 2. See interview by Tom Keene at Bloomberg (2021): https://www.bloomberg.com/news/videos/2021-07-28/nouriel-roubini-says-a- stagflationary-debt-crisis-is-on-the-way-video 3. See discussion of the global economic development at the IMF's latest report on World Economic Outlook (2022): https://www.imf.org/en/Publications/WEO