Download to read offline

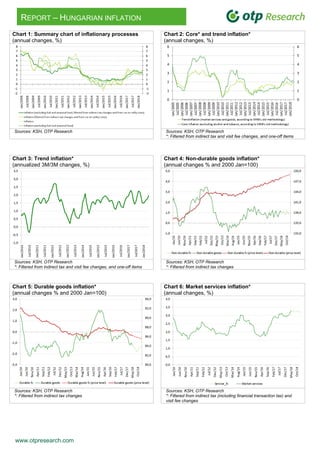

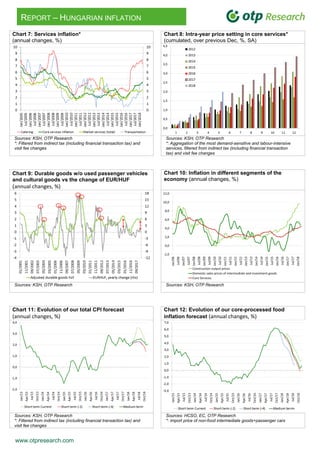

Hungarian inflation rose to 2.8% year-on-year in May 2018, driven mainly by higher fuel prices and increased services inflation. The report anticipates inflation may exceed the central bank's 3% target temporarily in the summer but forecasts it to decline thereafter due to base effects and decreasing food inflation. Methodological changes in their analysis framework aim to offer a clearer picture of core inflation trends, underscoring the influence of domestic demand and external factors on consumer prices.