Download to read offline

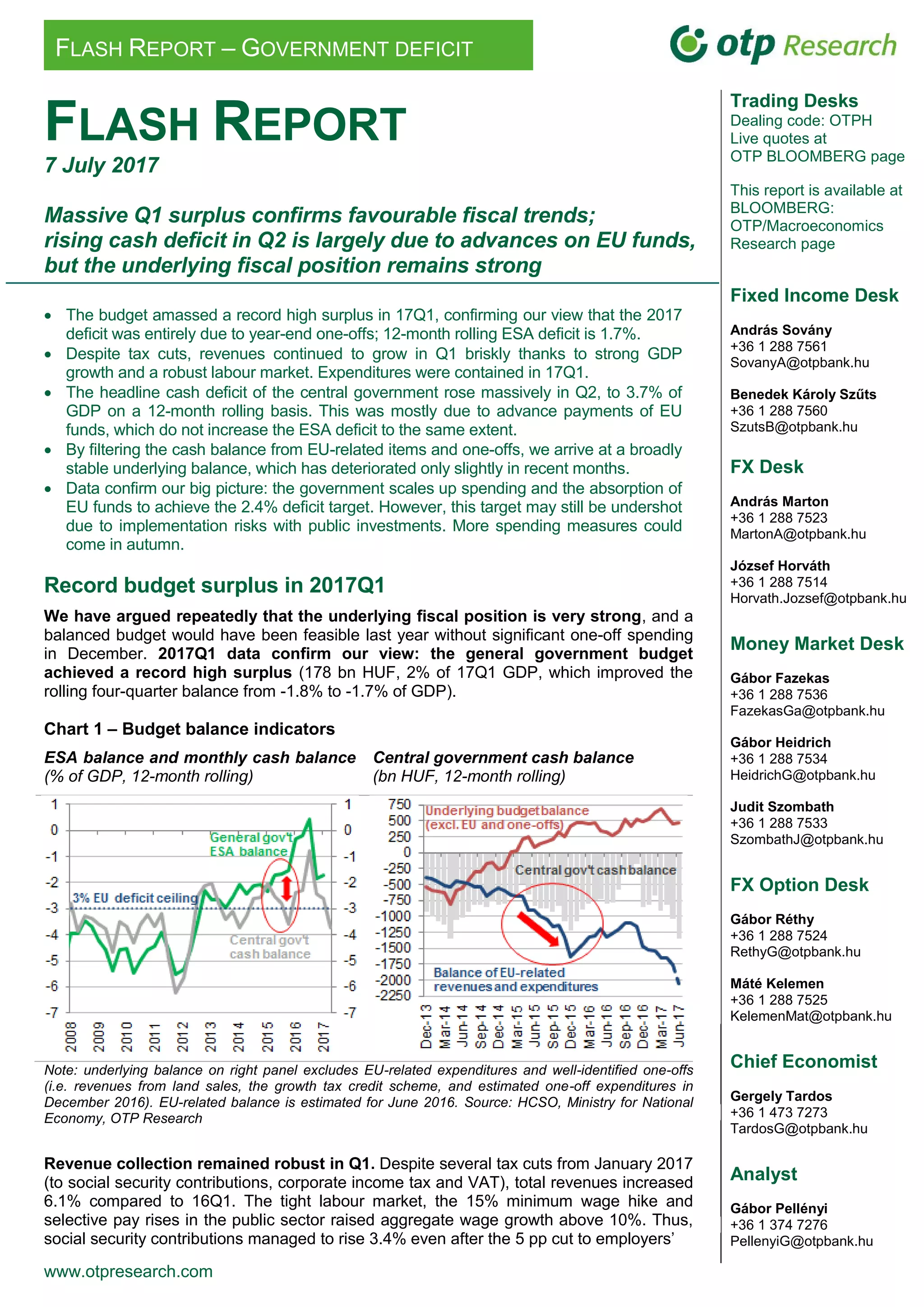

The document reports that Hungary achieved a record high budget surplus in Q1 2017, indicating a strong fiscal position despite a rising cash deficit in Q2 primarily caused by advances on EU funds. Revenue growth persisted due to robust GDP performance and tax collections, yet increased spending measures may be needed to meet the 2.4% deficit target ahead of the 2018 elections, amid various implementation risks. The analysis suggests that underlying fiscal stability remains, with potential additional spending measures expected in the autumn.