Downloaded 69 times

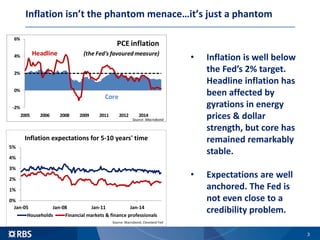

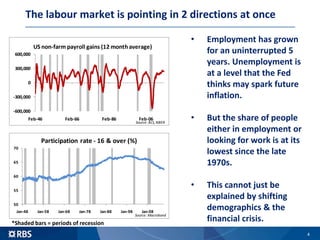

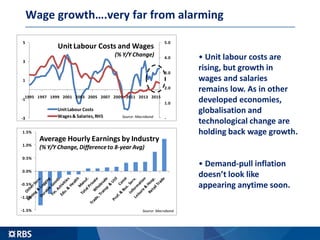

The document discusses the current state of inflation and economic growth in the U.S., indicating that inflation is well below the Federal Reserve's target and the labor market exhibits signs of duality, with stable unemployment but low participation rates. Wage growth remains subdued due to globalization and technological changes, while overall economic growth is modest compared to pre-crisis levels. The Fed is preparing for potential interest rate increases but must navigate emerging market vulnerabilities and the risks of exacerbating disinflationary trends.