The document outlines a coding guide for implementing various options trading strategies using QuantConnect's platform. It details the structure of the trading strategies, including classes for different options strategies (defined and undefined risk), methods for executing trades, backtesting parameters, and configurations for order handling. Additionally, it addresses some limitations of the platform and suggests custom solutions for improved functionality.

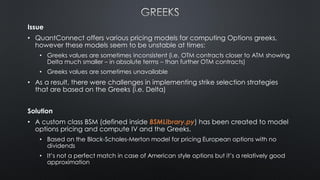

![• Each Strategy is defined as a class inheriting from the OptionStrategy class

• Additional strategies can be defined, by implementing the interface method getOrder()

• The input parameter chain is a list of option contracts for a given Expiration (controlled by the DTE parameter)

• The getOrder() method selects a number of contracts to buy/sell based on certain criteria (Call/Put, Delta, Strike,

Price)

• For strategies that require multiple expiration cycles (i.e. calendars), the run() method from the OptionStrategy class

must be overridden/implemented by the custom strategy class. See the implementation of class

TEBombShelterStrategy for details

class ButterflyStrategy(OptionStrategy):

def getOrder(self, chain):

return self.getButterflyOrder(chain

, netDelta = self.parameters["netDelta"]

, type = self.parameters["butteflyType"]

, leftWingSize = self.parameters["butterflyLeftWingSize"]

, rightWingSize = self.parameters["butterflyRightWingSize"]

, sell = self.parameters["creditStrategy"]

)

See the pre-built methods get<XYX>Order() inside

OptionStrategy.py for examples of how to

implement the getOrder() method](https://image.slidesharecdn.com/qcbacktesting-2021-220202003545/85/QuantConnect-Options-Backtesting-15-320.jpg)

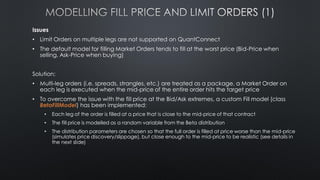

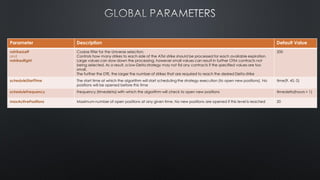

![Parameter Description Default Value

dte Days to Expiration. Used in conjunction with parameter dteWindow.

Contracts expiring in the range [dte-dteWindow, dte] are included in the selection process.

Once this filtering has been applied, the contracts with the expiration closest to the dte parameter are used

45

dteWindow See above 7

dteThreshold This parameter ignored if set to None or if dte < dteThreshold.

Once an open position reaches the dteThreshold, the following behavior is implemented:

• If forceDteThreshold = True close the position immediately, regardless of whether it is profitable or not

• If forceDteThreshold = False close the position as soon as it is profitable

21

allowMultipleEntriesPerExpiry Controls whether to allow a Strategy to open multiple positions on the same Expiration date False

forceDteThreshold Controls what happens when an open position reaches/crosses the dteThreshold. See above

useLimitOrders Controls whether to use Limit orders for Opening/Closing a position. True

limitOrderRelativePriceAdjustment Adjustment factor applied to the Mid-Price to set the Limit Order:

• Credit Strategy:

limitOrderRelativePriceAdjustment = 0.3 sets the Limit Order price 30% higher than the current Mid-Price

• Debit Strategy:

limitOrderRelativePriceAdjustment = -0.2 sets the Limit Order price 20% lower than the current Mid-Price

0.0

limitOrderAbsolutePrice Alternative method to set the absolute price (per contract) of the Limit Order. Only used if a value is specified

Unless you know that your price target can get a fill, it is advisable to use a relative adjustment or you may

never get your order filled

• Credit Strategy:

limitOrderAbsolutePrice = 1.5 sets the Limit Order price at exactly 1.5$

Debit Strategy:

limitOrderAbsolutePrice = -2.3 sets the Limit Order price at exactly -2.3$

None

limitOrderExpiration Controls how long Limit order is valid for. timedelta(hours = 8)](https://image.slidesharecdn.com/qcbacktesting-2021-220202003545/85/QuantConnect-Options-Backtesting-27-320.jpg)

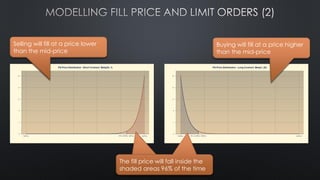

![Strategy Details

# Backtesting period

self.SetStartDate(2021, 1, 1)

self.SetEndDate(2021, 11, 30)

# Initial account value ($100K)

self.initialAccountValue = 100000

# Use SPY

self.ticker = "SPY"

# Open at 45 DTE

self.dte = 45

# Close at 21 DTE (no matter what)

self.dteThreshold = 21

self.forceDteThreshold = True

# Limit order 20% higher than the current mid-price

self.limitOrderRelativePriceAdjustment = 0.2

# Set expiration for Limit orders if they are not filled

self.limitOrderExpiration = timedelta(hours = 4)

# Sell enough contracts to reach $1000 premium (Fixed credit target)

self.targetPremium = 1000

# Sell no more than 6 contracts.

self.maxOrderQuantity = 6

# 60% Profit Target

self.profitTarget = 0.6

# 2X Stop Loss

self.stopLossMultiplier = 2 * self.profitTarget

# Holds all the strategies to be executed

self.strategies = []

# Sell a 10-Delta Put

self.strategies.append(PutStrategy(self, delta = 10, creditStrategy = True))](https://image.slidesharecdn.com/qcbacktesting-2021-220202003545/85/QuantConnect-Options-Backtesting-33-320.jpg)

![Strategy Details

# Backtesting period

self.SetStartDate(2021, 1, 1)

self.SetEndDate(2021, 11, 30)

# Initial account value ($100K)

self.initialAccountValue = 100000

# Use SPY

self.ticker = "SPY"

# Open at 45 DTE

self.dte = 45

# Close at 21 DTE (no matter what)

self.dteThreshold = 21

self.forceDteThreshold = True

# Limit order 20% higher than the current mid-price

self.limitOrderRelativePriceAdjustment = 0.2

# Set expiration for Limit orders if they are not filled

self.limitOrderExpiration = timedelta(hours = 4)

# Sell enough contracts to reach 1% of the Net Liq (Dynamic credit target)

self.targetPremiumPct = 0.01

# Sell no more than 10 contracts.

self.maxOrderQuantity = 10

# 60% Profit Target

self.profitTarget = 0.6

# 2X Stop Loss

self.stopLossMultiplier = 2 * self.profitTarget

# Holds all the strategies to be executed

self.strategies = []

# Sell a 10-Delta Put

self.strategies.append(PutStrategy(self, delta = 10, creditStrategy = True))](https://image.slidesharecdn.com/qcbacktesting-2021-220202003545/85/QuantConnect-Options-Backtesting-35-320.jpg)

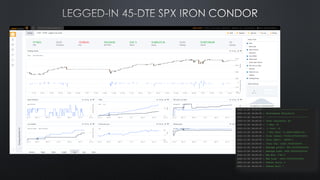

![# Backtesting period

self.SetStartDate(2021, 1, 1)

self.SetEndDate(2021, 11, 25)

# Initial account value ($1M)

self.initialAccountValue = 1000000

# Use SPX

self.ticker = "SPX"

# Open at 45 DTE

self.dte = 45

# No DTE threshold

self.dteThreshold = None

# Set expiration for Limit orders if they are not filled

self.limitOrderExpiration = timedelta(hours = 4)

# Sell enough contracts to reach $1000 premium

self.targetPremium = 1000

# Sell no more than 20 contracts.

self.maxOrderQuantity = 20

# 60% Profit Target

self.profitTarget = 0.6

# 2X Stop Loss

self.stopLossMultiplier = 2 * self.profitTarget

# Holds all the strategies to be executed

self.strategies = []

# Sell a 10-Delta, 25-wide Put Spread with a Limit price of $1

self.strategies.append(PutSpreadStrategy(self, delta = 10, wingSize = 25, limitOrderAbsolutePrice = 1 creditStrategy = True))

# Pair it with a 7-Delta, 25-wide Call Spread with a Limit price of $1.5

self.strategies.append(PutSpreadStrategy(self, delta = 7, wingSize = 25, limitOrderAbsolutePrice = 1.5 creditStrategy = True))](https://image.slidesharecdn.com/qcbacktesting-2021-220202003545/85/QuantConnect-Options-Backtesting-37-320.jpg)

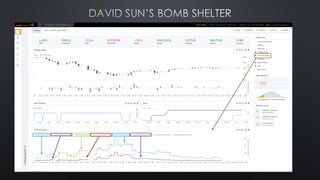

![Strategy Details

# Backtesting period

self.SetStartDate(2020, 2, 20)

self.SetEndDate(2020, 4, 30)

# Initial account value ($1M)

self.initialAccountValue = 1000000

# Use SPX

self.ticker = "SPX"

# Open at 45 DTE

self.dte = 120

# Search for contracts expiring between 80 DTE and 120 DTE

self.dteWindow = 40

# Process up to 400 strikes (=> 2000 points) to the left of ATM,

# zero strikes to the right

self.nStrikesLeft = 400

self.nStrikesRight = 0

# Close at 60 DTE (as soon as it is profitable)

self.dteThreshold = 60

# The dteThreshold is not enforced

self.forceDteThreshold = False

# Limit order 20% higher than the current mid-price

self.limitOrderRelativePriceAdjustment = 0.2

# Set expiration for Limit orders if they are not filled

self.limitOrderExpiration = timedelta(hours = 4)

# Dynamic Credit target: 1% of the Net Liq

self.targetPremiumPct = 0.01

# Sell no more than 3 contracts.

self.maxOrderQuantity = 3

# 60% Profit Target

self.profitTarget = 0.6

# Run only one position at the time

self.maxActivePositions = 1

# 2X Stop Loss

self.stopLossMultiplier = 2

# Disable some of the charts, there is a max limit of 10 time series

self.setupCharts(PnL = False, Performance = False

, WinLossStats = False, LossDetails = False

)

# Holds all the strategies to be executed

self.strategies = []

# Sell 120-DTE 15-Delta Put, use 10% of the credit to buy 2 90-DTE Puts.

# Plot the value of the Short and the Long contracts every 30 minutes

self.strategies.append(TEBombShelterStrategy(self

, delta = 15

, frontDte = self.dte – 30

, hedgeAllocation = 0.1

, plotLegDetails = True

, chartUpdateFrequency = 30)

)](https://image.slidesharecdn.com/qcbacktesting-2021-220202003545/85/QuantConnect-Options-Backtesting-39-320.jpg)

![Ifm derivatives 01[1].03.07](https://cdn.slidesharecdn.com/ss_thumbnails/ifm-derivatives011-03-07-130409134945-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)