The document provides an overview of algorithmic trading, including definitions, common components, and considerations for developing algorithmic trading strategies. It discusses the basic schema for algorithmic trading, including acquiring market data, analyzing the data, establishing conditions to trigger trades, and executing trades. It also covers related topics like risk management, portfolio management, data handling, and post-trade analysis. Additionally, it discusses different types of algorithmic trading strategies and considerations for backtesting strategies.

Algorithmic trading consistsof the automated buying and selling

of financial instruments (stocks, bonds and futures). Essentially It

requires a network connection to an electronic exchange, broker

or counterparty, and means of programmatically buying, selling

and performing other tasks related to trading, such as monitoring

price action and market exposure.

What is Algorithmic

Trading (or Algo)?

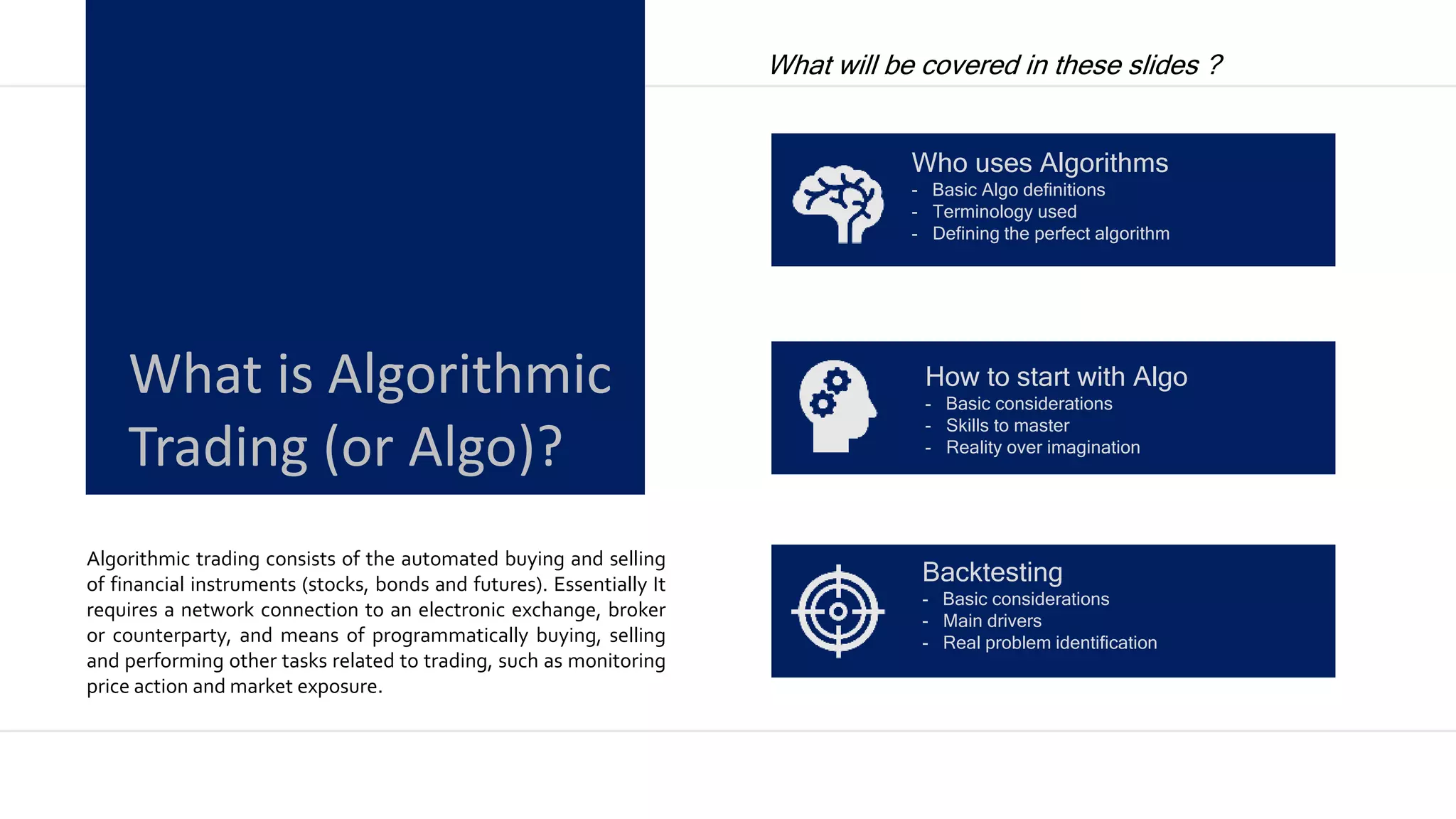

What will be covered in these slides ?

Who uses Algorithms

- Basic Algo definitions

- Terminology used

- Defining the perfect algorithm

How to start with Algo

- Basic considerations

- Skills to master

- Reality over imagination

Backtesting

- Basic considerations

- Main drivers

- Real problem identification

3.

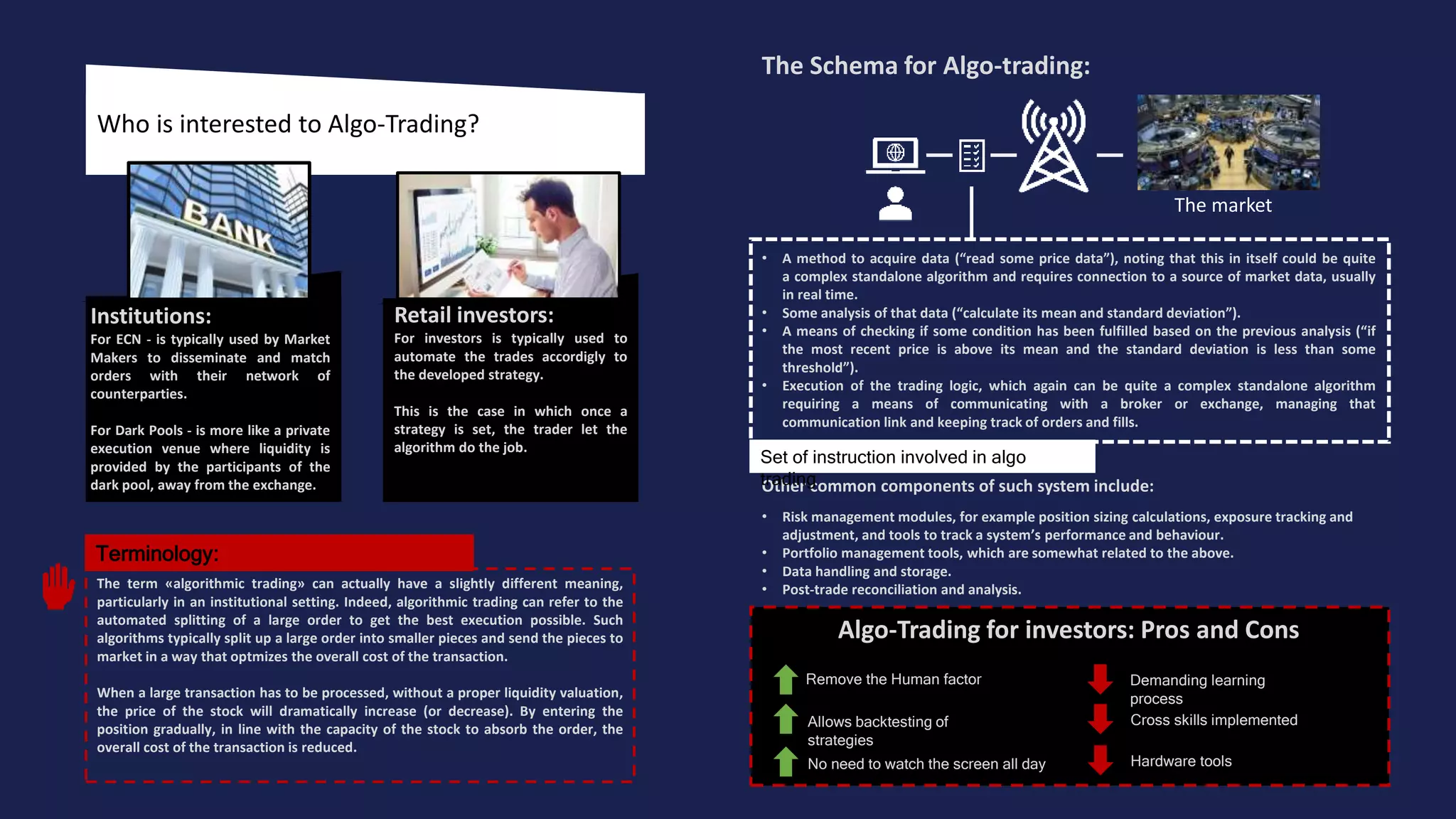

Who is interestedto Algo-Trading?

Algo-Trading for investors: Pros and Cons

The Schema for Algo-trading:

• A method to acquire data (“read some price data”), noting that this in itself could be quite

a complex standalone algorithm and requires connection to a source of market data, usually

in real time.

• Some analysis of that data (“calculate its mean and standard deviation”).

• A means of checking if some condition has been fulfilled based on the previous analysis (“if

the most recent price is above its mean and the standard deviation is less than some

threshold”).

• Execution of the trading logic, which again can be quite a complex standalone algorithm

requiring a means of communicating with a broker or exchange, managing that

communication link and keeping track of orders and fills.

Other common components of such system include:

• Risk management modules, for example position sizing calculations, exposure tracking and

adjustment, and tools to track a system’s performance and behaviour.

• Portfolio management tools, which are somewhat related to the above.

• Data handling and storage.

• Post-trade reconciliation and analysis.

Remove the Human factor

Allows backtesting of

strategies

Demanding learning

process

The term «algorithmic trading» can actually have a slightly different meaning,

particularly in an institutional setting. Indeed, algorithmic trading can refer to the

automated splitting of a large order to get the best execution possible. Such

algorithms typically split up a large order into smaller pieces and send the pieces to

market in a way that optmizes the overall cost of the transaction.

When a large transaction has to be processed, without a proper liquidity valuation,

the price of the stock will dramatically increase (or decrease). By entering the

position gradually, in line with the capacity of the stock to absorb the order, the

overall cost of the transaction is reduced.

The market

Set of instruction involved in algo

trading

No need to watch the screen all day

Cross skills implemented

Hardware tools

Retail investors:

For investors is typically used to

automate the trades accordigly to

the developed strategy.

This is the case in which once a

strategy is set, the trader let the

algorithm do the job.

Institutions:

For ECN - is typically used by Market

Makers to disseminate and match

orders with their network of

counterparties.

For Dark Pools - is more like a private

execution venue where liquidity is

provided by the participants of the

dark pool, away from the exchange.

Terminology:

4.

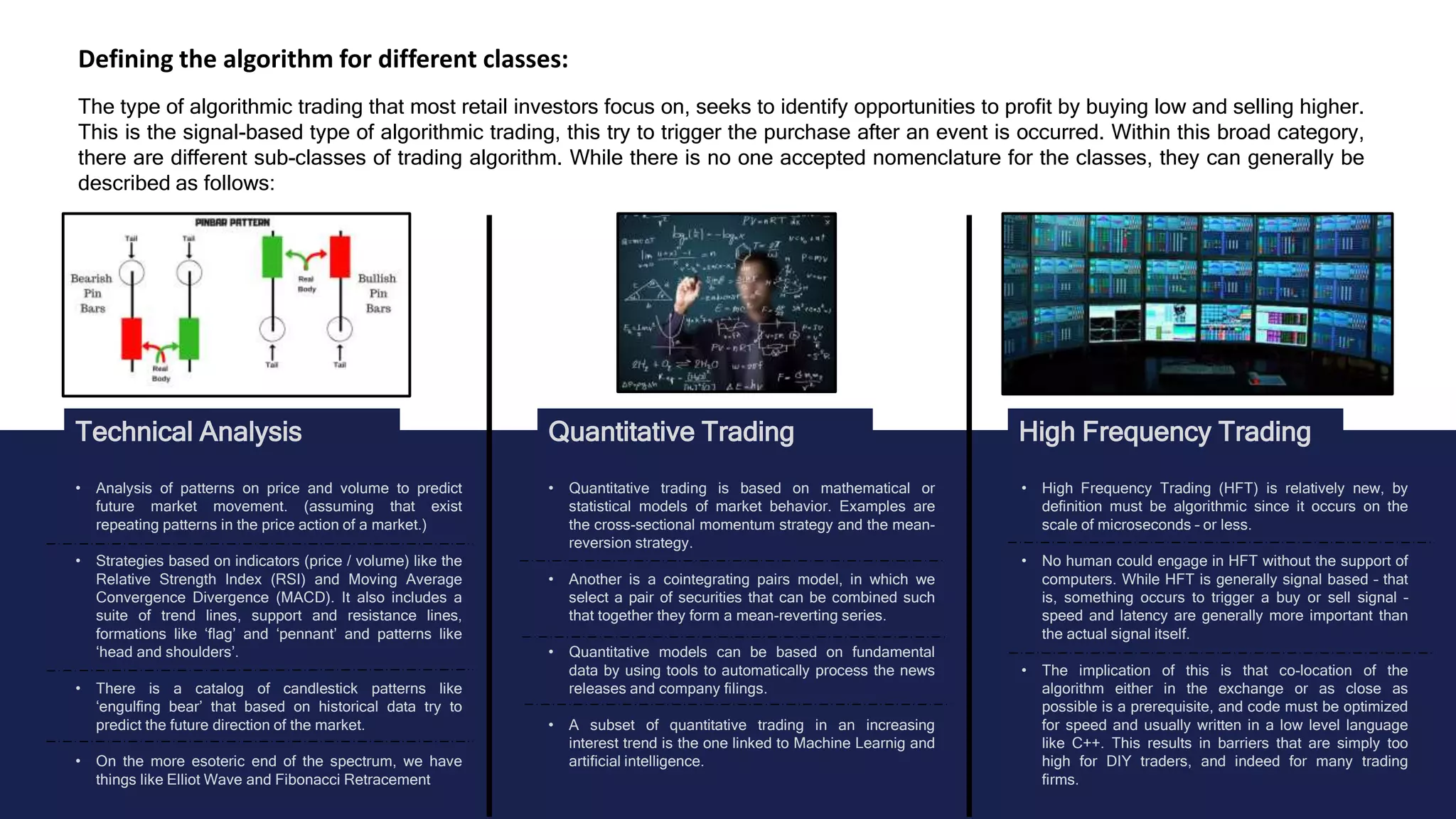

Technical Analysis QuantitativeTrading High Frequency Trading

Defining the algorithm for different classes:

The type of algorithmic trading that most retail investors focus on, seeks to identify opportunities to profit by buying low and selling higher.

This is the signal-based type of algorithmic trading, this try to trigger the purchase after an event is occurred. Within this broad category,

there are different sub-classes of trading algorithm. While there is no one accepted nomenclature for the classes, they can generally be

described as follows:

• Analysis of patterns on price and volume to predict

future market movement. (assuming that exist

repeating patterns in the price action of a market.)

• Strategies based on indicators (price / volume) like the

Relative Strength Index (RSI) and Moving Average

Convergence Divergence (MACD). It also includes a

suite of trend lines, support and resistance lines,

formations like ‘flag’ and ‘pennant’ and patterns like

‘head and shoulders’.

• There is a catalog of candlestick patterns like

‘engulfing bear’ that based on historical data try to

predict the future direction of the market.

• On the more esoteric end of the spectrum, we have

things like Elliot Wave and Fibonacci Retracement

• Quantitative trading is based on mathematical or

statistical models of market behavior. Examples are

the cross-sectional momentum strategy and the mean-

reversion strategy.

• Another is a cointegrating pairs model, in which we

select a pair of securities that can be combined such

that together they form a mean-reverting series.

• Quantitative models can be based on fundamental

data by using tools to automatically process the news

releases and company filings.

• A subset of quantitative trading in an increasing

interest trend is the one linked to Machine Learnig and

artificial intelligence.

• High Frequency Trading (HFT) is relatively new, by

definition must be algorithmic since it occurs on the

scale of microseconds – or less.

• No human could engage in HFT without the support of

computers. While HFT is generally signal based – that

is, something occurs to trigger a buy or sell signal –

speed and latency are generally more important than

the actual signal itself.

• The implication of this is that co-location of the

algorithm either in the exchange or as close as

possible is a prerequisite, and code must be optimized

for speed and usually written in a low level language

like C++. This results in barriers that are simply too

high for DIY traders, and indeed for many trading

firms.

5.

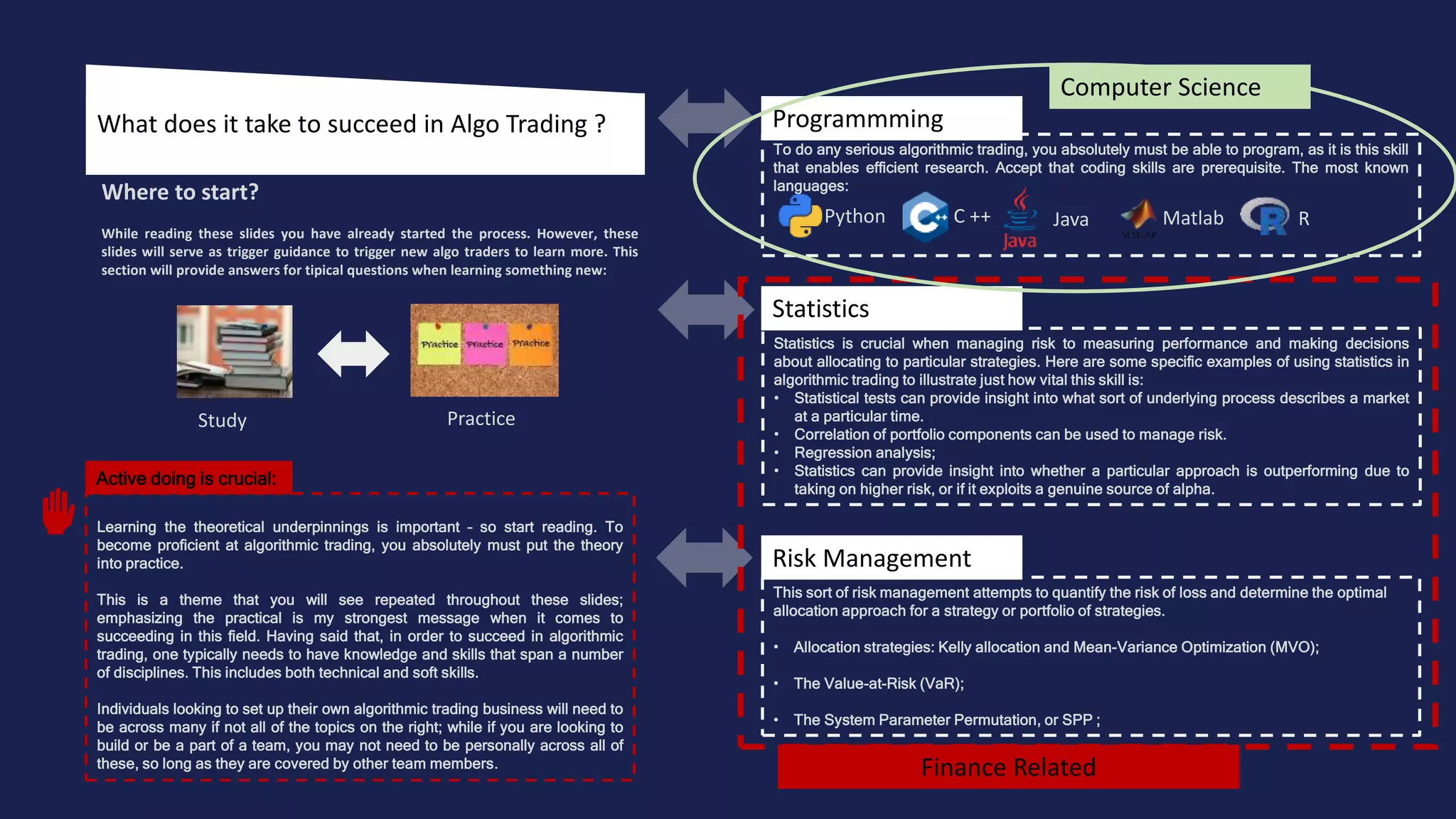

What does ittake to succeed in Algo Trading ?

Where to start?

While reading these slides you have already started the process. However, these

slides will serve as trigger guidance to trigger new algo traders to learn more. This

section will provide answers for tipical questions when learning something new:

Learning the theoretical underpinnings is important – so start reading. To

become proficient at algorithmic trading, you absolutely must put the theory

into practice.

This is a theme that you will see repeated throughout these slides;

emphasizing the practical is my strongest message when it comes to

succeeding in this field. Having said that, in order to succeed in algorithmic

trading, one typically needs to have knowledge and skills that span a number

of disciplines. This includes both technical and soft skills.

Individuals looking to set up their own algorithmic trading business will need to

be across many if not all of the topics on the right; while if you are looking to

build or be a part of a team, you may not need to be personally across all of

these, so long as they are covered by other team members.

Active doing is crucial:

Statistics is crucial when managing risk to measuring performance and making decisions

about allocating to particular strategies. Here are some specific examples of using statistics in

algorithmic trading to illustrate just how vital this skill is:

• Statistical tests can provide insight into what sort of underlying process describes a market

at a particular time.

• Correlation of portfolio components can be used to manage risk.

• Regression analysis;

• Statistics can provide insight into whether a particular approach is outperforming due to

taking on higher risk, or if it exploits a genuine source of alpha.

Statistics

To do any serious algorithmic trading, you absolutely must be able to program, as it is this skill

that enables efficient research. Accept that coding skills are prerequisite. The most known

languages:

Programmming

This sort of risk management attempts to quantify the risk of loss and determine the optimal

allocation approach for a strategy or portfolio of strategies.

• Allocation strategies: Kelly allocation and Mean-Variance Optimization (MVO);

• The Value-at-Risk (VaR);

• The System Parameter Permutation, or SPP ;

Risk Management

Finance Related

Computer Science

Python C ++ Java Matlab R

Study Practice

6.

Expectations Frequency ofTrading Infrastructure

Important Practical Matters:

Bear in mind that this is a very difficult path to deal with, due to the complexity of the arguments related to algo trading, in order to develop

strategies and really build up something you will need time and effort. First of all, you should master at least one of those skills previously

mentioned, then you can start to implement those skills in other context.

• This is not a way to become a millionare in just one

day – Hedge funds have 3-year compounded annual

return of just under 30%. You are not SMARTER !!!

• There may exist market phenomena that can generate

returns that are significant compared to the position

sizing of a retail account, but which are not capable of

carrying the trades of a larger fund.

• The amount of gains is tangled up with the amount of

risk you are willing to take. Thinking about reward in

terms of risk rather than in isolation will lead you to

much more sensible expectations.

• Swing Traders: are those who sets a lower frequency

of trading and hold a trade for weeks or months.

• Day Traders: holds positions for 2 days or less

• Intra-day Traders holds posistions within the day,

meaning that they open trades as soon as the market

open and close them before the closing day.

• High frequency trading generally refers to systems with

holding periods on the order of milliseconds to

seconds.

• Access to a strong (APIs) through a broker or through

a protocol, namely FIX, or Financial Information

Exchange.

• HFTs are not accessible by a retail investor who is

able to program due to restrictions on liquidity amount

and infrastructure complexity.

• For retail algo traders, a normal computer is enough to

process their algos, in order to perform algorithms 24h

a day, knowledge of warehouse servers is needed.

• Computer specifications and algorithms implemented

needs to be set out properly in order to be more

efficient.

7.

Backtesting – Measuringthe results

Traditional approach:

• Choose one strategy

• Implement the strategy for a

period of time.

• Take notes of the results and

grasp the pitfalls

Algo approach:

• Choose one or more strategies

• Set the timeseries in which you

want to perform the backtest

• Understand the variables that

affects the most the strategy and

rewrite the algorithm properly.

Slow Dynamic

• Slippage

• Commissions

• Swaps

Trading conditions

Simulation

vs

Reality

Backtesting requires that your trading algorithm’s performance be simulated using historical market

data, and the profit and loss of the resulting trades aggregated. Dealing with these two problems

requires that we consider:

Requirements for a good Backtest

• The Timeframe used for the analysis heavily influence

Granularity

• Sample of data discrepancies

Sample of data

Accuracy main drivers

Simulation accuracy Time frame employed

• Entry levels

• Exits

• Volume

• Market volatility

• Market liquidity

• Order type

• Execution Lathency

Influencing factors:

• Broker pricing

• Missing data

• On the traded product

• Data source

Where can be

found:

8.

Look-Ahead Bias orPeeking Bias Curve-Fitting Bias or over-Optimization Bias Data-Mining Bias or Selection Bias

Development methodology:

In addition to simulation accuracy, the experimental methodology itself can compromise the results of our simulations. Many of these biases are

subtle yet profound: they can and will very easily creep into a trading strategy research and development process and can have disastrous effects on

live performance. Accounting for these biases is critical and needs to be considered at every stage of the development process. For now, I will walk

through and explain the various biases that can creep in and their effect on a trading strategy.

• This form of bias is introduced by allowing future

knowledge to affect trade decisions. That is, trade

decisions are affected by knowledge that would not

have been available at the time the trade decision was

taken.

• A common example is executing an intra-day trade on

the basis of the day’s closing price, when that closing

price is not actually known until the end of the day.

• Another bias example is when we use a parameter

which has been estimated and then retrospectively

apply it to the beginning of the next run of the

simulation.

• Portfolio optimization parameters are particularly prone

to this bias.

• Data mining bias is another significant source of over-

estimated model performance.

• It is reconducible to the selection of a sample, once a

strategy has been tested, it is unlikely that the same

strategy works with other instruments or time frames

• It is impossible to solve the problem, a strategy must

work dependently with his framework.

• This is the bias that allows us to create magical backtests that

produce annual returns on the order of hundreds of percent.

Such backtests are of course completely useless for any

practical trading purpose.

• Regression models on more data will produce a cut of noise

and of course a curve-fitting shape.

• The more the sample embed the noise in the sample the more

the trading results will be of no value due to an always

increasing curve